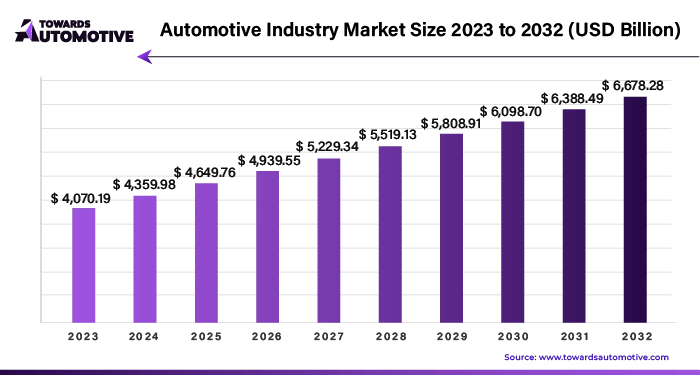

Ottawa, April 15, 2024 (GLOBE NEWSWIRE) -- The global automotive industry size was valued at USD 4,070.19 billion in 2023 and is predicted to hit around USD 6,388.49 billion by 2031, a study published by Towards Automotive a sister firm of Precedence Research.

In today's rapidly evolving business landscape, marked by the proliferation of emerging markets, the rapid advancement of new technologies, stringent security regulations, and shifting customer preferences, the automotive industry finds itself at the nexus of transformative change. Digitalization and innovative business models are reshaping traditional paradigms, ushering in a new era of disruption in the automotive sector.

Four critical technological disruptions—mobility, autonomous driving, electric vehicles, and connected technologies—are poised to revolutionize the automotive landscape. While these disruptions are often viewed as independent phenomena, there's a growing consensus among business leaders and industry experts that they are intricately interconnected, complementing, and reinforcing each other. The industry, overall, is perceived as primed and ready for substantial transformation.

Download a short version of this report @ https://www.towardsautomotive.com/insight-sample/1207

However, despite the widespread acknowledgment of impending change, there still needs to be a cohesive, overarching vision delineating how these disruptions will manifest in the automotive domain over the next 10 to 15 years. This lack of a unified vision presents challenges and opportunities, underscoring the need for stakeholders to shape and navigate the impending shifts proactively.

With this announcement, we aim to underscore the inevitability of change and delve deeper into the nuances and implications of these impending transformations. We seek to catalyze proactive engagement and strategic planning within the automotive industry by providing granular insights and quantifying the magnitude of these impending changes. Through collaborative efforts and foresighted initiatives, we can harness the potential of these disruptions to drive sustainable growth, innovation, and competitiveness in the automotive sector.

You can place an order or ask any questions, please feel free to contact us at sales@towardsautomotive.com

- The 2030 Automotive Revolution perspective culminates in a comprehensive process involving various stakeholders, including employees, startups, established businesses, research institutions, and law firms. This transformative outlook is shaped by a multi-faceted approach encompassing executive interviews, in-depth discussions with over 30 industry experts across Asia, Europe, and the United States, and rigorous analysis of market trends and technological advancements.

- Employees within automotive companies play a pivotal role in providing frontline insights and perspectives on emerging trends and consumer preferences. Their experiences and observations serve as valuable inputs in shaping the narrative of the automotive revolution.

- Startups and entrepreneurial ventures contribute innovative ideas and disruptive technologies that challenge traditional paradigms and drive industry evolution. Through collaborations and partnerships with established players, startups inject fresh perspectives and accelerate the pace of innovation within the automotive ecosystem.

- Business research and investments conducted by market analysts, investment firms, and strategic consultants provide critical insights into market dynamics, competitive landscapes, and emerging opportunities. These research endeavors inform strategic decision-making processes and guide investment allocations toward promising ventures and technologies.

- Law firms specializing in automotive regulations and intellectual property rights play a crucial role in navigating the industry's legal complexities. Their expertise ensures compliance with regulatory frameworks, protects intellectual property assets, and mitigates legal risks associated with technological advancements and market disruptions.

- Executive interviews and in-depth discussions with industry experts are the cornerstone of the 2030 Automotive Revolution perspective. A holistic understanding of emerging trends, market dynamics, and technological disruptions is attained by engaging with thought leaders and visionaries across diverse geographies and disciplines. These insights inform the development of strategic roadmaps and business models that anticipate and capitalize on future trends, such as the rise of electric and autonomous vehicles and their integration into macroeconomic frameworks.

- Ultimately, the 2030 Automotive Revolution perspective recognizes the convergence of various factors, from employee insights to entrepreneurial innovation, business research to legal expertise, in shaping the trajectory of the automotive industry toward a transformative future characterized by electrification, autonomy, and evolving consumer behaviors.

Customize this study as per your requirement @ https://www.towardsautomotive.com/contact-us

The automotive industry is undergoing a profound transformation, with eight key perspectives shaping its trajectory towards 2033. These perspectives provide insights into the current shifts and their implications for various stakeholders, including OEMs and suppliers, new entrants, management, customers, and the domestic auto industry.

- New Business Model Driven by Integration and Innovation: The emergence of a new business model characterized by integration, service connectivity, and innovation is poised to revolutionize the automotive industry. This transformation could potentially boost auto revenue by nearly 30%, reaching a total of $1.5 trillion. This shift highlights the growing importance of leveraging technology and connectivity to enhance customer experiences and create new revenue streams.

- Moderated Growth in Car Sales: Despite the transition to integrated business models, car sales are expected to increase, albeit at a lower annual growth rate of approximately 2%. This reflects changing consumer preferences, evolving mobility needs, and the increasing emphasis on sustainability and alternative transportation solutions.

- Changing Mobility Habits and Shared Ownership: The changing mobility habits of consumers are paving the way for shared ownership models. By 2030, it is projected that one in every 10 cars sold will be shared, leading to a significant expansion of the market for shared mobility systems. This trend underscores the shift towards more sustainable and efficient transportation solutions, driven by technological advancements and evolving consumer behaviours.

- City Brand as a Determinant of Travel Behaviour: In the automotive revolution, the concept of the city brand is poised to supersede traditional country or regional segmentation dimensions in shaping travel behaviour. The characteristics and attributes of cities will play a pivotal role in influencing consumer preferences and driving the adoption of new mobility solutions. Understanding and adapting to the unique needs and dynamics of urban environments will be crucial for stakeholders seeking to capitalize on emerging opportunities in the automotive sector.

The automotive industry in 2033 will be defined by integrated business models, moderated growth in car sales, the proliferation of shared ownership models, and the increasing influence of city brands on travel behaviour. Embracing these key perspectives will be essential for stakeholders to navigate the evolving landscape and unlock opportunities for growth and innovation in the automotive ecosystem.

The promotion of advanced technology within the automotive industry is poised to catalyse significant shifts in the coming years. Our analysis has identified eight key assumptions that underscore the transformative impact of these advancements on incumbent players and new entrants alike.

- Autonomous Vehicles on the Horizon: With the resolution of technical and regulatory hurdles, it is projected that up to 15% of new cars sold by 2030 will be fully autonomous. This represents a paradigm shift in transportation and underscores the growing viability of self-driving technology.

- Regional Variances in Electric Vehicle Adoption: While electric vehicles (EVs) are becoming increasingly efficient and competitive, the pace of their adoption is expected to vary significantly from region to region. Factors such as infrastructure development, government incentives, and consumer preferences will shape the trajectory of EV adoption worldwide.

- Navigating Competition and Cooperation: In an increasingly diverse and dynamic business environment, incumbent players will face the dual challenge of competing on multiple fronts while also engaging in cooperative endeavours with competitors. This necessitates a nuanced approach to business strategy, balancing competitive pressures with collaboration opportunities to drive growth and innovation.

- Focus and Expansion for New Entrants: New entrants into the automotive industry are expected to initially focus on specific, attractive business segments before gradually expanding into adjacent areas. This strategic approach allows for targeted investment and resource allocation, maximizing opportunities for success in the competitive landscape.

Leveraging strategic partnerships, adapting organizational structures, and reinventing value propositions are imperative strategies to navigate the evolving automotive landscape and seize opportunities for growth and innovation.

In essence, by embracing these principles and leveraging their inherent strengths, incumbent players can position themselves at the forefront of the automotive revolution, driving sustainable success in a rapidly evolving market.

The global automobile industry is undergoing significant shifts, presenting both challenges and opportunities for growth.

Driving Growth

- Investment in Public Transport: There is a growing demand for large vehicles, such as large cars and long-distance buses, driven by increased investment in public transport. Local governments are under pressure to revamp existing transportation systems to meet the evolving needs of users and alleviate road congestion caused by private vehicles. Companies like UBS Univers Busservice GmbH and MarinoBus are introducing longer buses equipped with driver assistance and LED lighting to cater to long-distance travel needs.

- Demand in Emerging Markets: Automotive companies are capitalizing on the rising demand for affordable private cars in developing countries like India, China, and Africa. With the middle-income group expanding in these regions, companies are introducing affordable new cars and motorcycles. For instance, Maruti Suzuki introduced the Fronx SUV in the South African market, targeting affordability and regional preferences.

Constraints

- Environmental Impact: The automobile industry faces constraints related to environmental concerns associated with vehicle production and operation. Car manufacturing processes require significant resources, contributing to issues such as deforestation and ecosystem damage. Additionally, emissions from internal combustion engines and reliance on fossil fuels pose challenges to future growth.

Opportunities

- Growing Electric Vehicle Market: The increasing interest in electric vehicles (EVs) presents a significant growth opportunity for automotive industry players. Factors such as environmental awareness, rising fuel prices, and technological advancements have made electric cars more affordable and attractive. Companies like Nissan and Renault are shifting their focus towards electric vehicles, aiming to offer fully electric models in the near future. Investments in infrastructure for fast charging and research and development to enhance EV performance are expected to further drive growth in this segment.

The automotive market faces several challenges, including:

- Rise in Raw Material Prices: Global competition in the automotive industry is challenged by the increasing prices of essential raw materials such as steel, rubber, glass, and plastic. The fluctuating costs of these materials can impact production expenses and profitability for manufacturers.

- Economic Uncertainty: Economic instability and uncertainty can pose significant challenges for the automotive sector. Factors such as changes in consumer income, disposable income, and overall economic health can influence consumer spending patterns and purchasing decisions. Uncertainty in economic conditions can also affect investment decisions and long-term planning for automotive companies.

- Competitive Market Dynamics: The automotive industry operates in a highly competitive market environment, characterized by constant innovation and technological advancements. Today's cars are equipped with advanced features such as remote monitoring, driver assistance systems, and augmented reality displays. While these technologies enhance the driving experience and safety, they also contribute to increased production costs, putting pressure on manufacturers to balance cost-effectiveness with product innovation.

Addressing these challenges requires strategic planning, innovation, and adaptability on the part of automotive companies. Finding ways to mitigate the impact of rising raw material prices, navigating economic uncertainties, and staying competitive in the market landscape are key priorities for industry players. Collaboration, efficient supply chain management, and investment in research and development are crucial strategies for overcoming these challenges and sustaining growth in the automotive market.

Overall, while the automotive industry faces challenges related to environmental sustainability and resource utilization, opportunities abound in the form of growing demand for public transport solutions and the transition towards electric vehicles, signaling a transformative shift in the market landscape.

Shifting Markets and Revenue Pools

Changing markets and evolving profit landscapes within the automotive industry are prompting a re-evaluation of conventional wisdom. While some commentators suggest a decline in the auto market, we maintain that rapid growth driven by new revenue streams, such as integration and data connectivity services, along with emerging business opportunities, underscores the resilience of the global economy.

Help of new business models, car income may rise by around 30% to USD 1.5 trillion, driven by shared mobility, connection services, and feature upgrades.

- New Business Model Driving Revenue Growth: Anchored by integration, service connectivity, and innovation, the automotive industry is poised for significant revenue growth. Projections indicate that adopting this new business model could elevate car revenue by approximately 30%, reaching an estimated $1.5 trillion. This represents a substantial increase from the traditional auto and aftermarket sales revenue sources.

- Diversified Revenue Streams: The evolving landscape of automotive revenue will be characterized by a mix of traditional sources, service requests, and driver information. This diversified revenue stream has the potential to propel annual growth rates to 4.4%, surpassing the 3.6% growth observed between 2010 and 2015. Connectivity and self-driving technologies will transform automobiles into platforms for personalized experiences, driving further revenue opportunities through targeted advertising and services.

- Innovation Driving Consumer Engagement: Advancements in software-based systems and connectivity will necessitate continuous updates and upgrades, ensuring that vehicles remain at the forefront of technological innovation. Additionally, the proliferation of shared mobility solutions and advancements in repair technology will enhance consumer interest in private vehicle ownership.

As short-term shared mobility solutions gain traction, consumers will increasingly prioritize personalized experiences and advanced repair capabilities, further bolstering demand for private vehicle ownership. Adapting to these shifting dynamics, automotive companies must invest in innovative technologies, foster strategic partnerships, and prioritize consumer-centric approaches to capitalize on emerging opportunities and sustain growth in a rapidly evolving market landscape.

Despite a move toward shared mobility, vehicle unit sales are predicted to expand going forward, albeit more slowly—roughly 2% annually

Global auto sales are anticipated to maintain an upward trajectory, albeit at a slower annual growth rate of 2% by 2030, compared to the 3.6% growth observed in the past five years. This deceleration can be attributed to macroeconomic factors and the burgeoning popularity of new mobility services such as car sharing and e-hailing.

An in-depth analysis reveals that regions characterized by dense populations and a robust automobile manufacturing base are prime candidates for the proliferation of these new mobility services. Many European and North American cities and locations fit this profile, making them conducive environments for the adoption of car sharing and e-hailing services. Consequently, the advent of these services may lead to a decline in private vehicle sales. However, this decline could be mitigated by increased sales of shared vehicles, which necessitate greater utilization and maintenance due to prolonged exposure to wear and tear.

Despite these shifts in consumption patterns, the primary driver of global sales growth remains positive macroeconomic developments, including the rising purchasing power of international consumers. The expansion of mature markets may be limited, necessitating a continued reliance on emerging markets, particularly China and India, to sustain overall growth momentum in the automotive industry.

In essence, while the rise of new mobility services may reshape consumer preferences and impact sales dynamics, the resilience of global auto sales hinges on a combination of macroeconomic factors and the continued expansion of emerging markets. Adapting to these evolving trends will be imperative for automotive companies to navigate the changing landscape and capitalize on emerging opportunities for growth and profitability.

Changes in Mobility Behaviour

Understanding customer preferences and behaviours is essential for evaluating the potential for business transformation, particularly in the context of disruptive technologies that can reshape the relationship between customers and cars.

- Changing Consumer Behaviour and Rise of Shared Ownership: A shift in consumer behaviour is evident, with projections indicating that 2030, one in ten cars sold will be shared vehicles. This shift is driving the emergence of a market for hardware tailored to customer preferences, efficient management, and technological integration. As consumers increasingly opt for various modes of transportation to fulfil their travel needs, the traditional car ownership model is being challenged, particularly in densely populated urban areas where private vehicles may need to be more practical.

Customers today view their cars as versatile vehicles suitable for various purposes, from solo commuting to family outings. However, future consumers will prioritize flexibility, seeking tailored solutions for specific purposes akin to selecting apps on their smartphones.

Evidence suggests a diminishing emphasis on private vehicle ownership and a rise in shared ownership models. For instance, in the United States, the percentage of young people (ages 16 to 24) with driver's licenses has declined from 76% in 2000 to 71% in 2013. Concurrently, Northern United States and Germany carpooling memberships have experienced annual growth rates exceeding 30% over the past five years.

The shift towards integration will enable customers to access optimal solutions for every purpose, paving the way for the emergence of purpose-built automobiles catering to specific needs. For example, car parks designed for electric ride-hailing services may offer features tailored for shopping, commuting, work, leisure, entertainment, and daily errands.

Understanding evolving consumer behaviours and preferences is imperative for automotive companies seeking to capitalize on emerging trends and shape their offerings to meet customers' changing needs in an increasingly interconnected and shared mobility landscape.

The shift towards integration in transportation is fostering the emergence of new businesses tailored to specific needs, such as fleets of vehicles designed specifically for e-hailing services. These vehicles prioritize high efficiency, robustness, extended mileage, and passenger comfort, with millions already in operation, signalling the nascent stage of this trend. As integration enables multi-modal solutions, projections indicate that by 2030, one in ten new cars sold could be for car-sharing purposes, leading to a reduction in private car sales. This shift towards shared mobility is expected to accelerate, with more than 30% of the mileage of new cars sold potentially being shared by 2030, and as much as one-third of new cars sold by 2050 could be for carpooling.

The concept of the "city brand" is poised to supersede traditional regional segmentation dimensions in shaping travel behaviour and driving the automotive revolution. Understanding the future of business necessitates a nuanced approach that recognizes the diverse characteristics of different cities based on factors such as population density, economic development, and prosperity. Low-income cities are experiencing significant population growth, while high-income cities remain relatively stable. Customer preferences, regulatory policies, and the availability and cost of new business models will vary across these segments. For instance, major cities like London or Shanghai face challenges such as congestion charges, parking shortages, and traffic congestion, making private vehicle ownership burdensome for many residents and creating a competitive advantage for car-sharing services. Conversely, rural areas with lower population density are likely to continue relying on private vehicle ownership as the primary mode of transportation due to limitations in scale for shared mobility services.

Businesses should tailor their strategies to align with the unique characteristics and challenges of different city types, leveraging opportunities presented by new business models in large urban centres while recognizing the continued importance of private vehicle ownership in rural areas.

Diffusion of Advanced Technology

Autonomous technology and electric power have sparked widespread interest, presenting significant long-term potential in the automotive industry. However, the pace of expansion over the next 15 years will hinge on overcoming various obstacles.

Once technical and regulatory challenges are addressed, projections suggest that up to 15% of new cars sold by 2030 could be fully autonomous. However, the widespread availability of autonomous vehicles (AVs) is unlikely before 2020. In the interim, advanced driver assistance systems (ADAS) will play a pivotal role in preparing drivers, customers, and businesses for the transition to autonomous driving. Commercialization of ADAS has been impeded by cost constraints, limited consumer understanding, and security concerns, particularly in achieving NHTSA Rule Level 3 and Level 4 automation.

Technology players and startups are expected to play a significant role in overcoming these challenges and enabling the widespread adoption of autonomous technology. Regulatory and consumer acceptance represent additional hurdles, but the benefits of driverless cars, such as increased productivity and convenience, have the potential to drive widespread adoption once these issues are addressed.

A significant shift is anticipated in the automotive landscape, with approximately 50% of passenger cars sold in 2030 projected to feature autonomous capabilities, and around 15% being fully autonomous. This transformative trend underscores the potential for autonomous technology to revolutionize the way people travel and interact with vehicles, paving the way for a future where driving becomes more efficient, convenient, and safe.

Electric vehicles (EVs) are gaining traction due to their increasing efficiency and competitiveness. However, the pace of their adoption will vary significantly at the local level, influenced by factors such as emissions regulations, battery costs, charging infrastructure, and consumer acceptance.

The tightening of emissions regulations, coupled with declining battery costs and the expansion of charging infrastructure, will provide a significant boost to the proliferation of EVs, including hybrids, plug-in hybrids, battery electric vehicles (BEVs), and fuel cell vehicles, in the coming years. The speed of adoption will be determined by the interplay between customer attractiveness, including the total cost of ownership, and governmental incentives and policies, which will vary regionally and locally.

By 2030, the share of electric cars in new car sales is projected to range from 10% to 50%. Adoption rates are expected to be highest in developed, densely populated cities with stringent emissions regulations and consumer incentives such as tax breaks, private parking privileges, and reduced electricity costs. Conversely, sales penetration will be slower in small towns and rural areas where housing prices are lower and there is a greater reliance on personal vehicle ownership.

Continued advancements in battery technology and cost reduction are anticipated to mitigate these local disparities, making EVs increasingly affordable compared to traditional internal combustion engine vehicles. By the next decade, battery prices are forecasted to decline to $150 to $200 per kilowatt-hour, rendering electric cars cost-competitive and enhancing their market penetration. Furthermore, improvements in payment technology, multiple payment options, and heightened consumer awareness will further augment the value proposition of EVs.

It is noteworthy that despite the rise of EVs, the majority of electric cars are expected to be hybrids, indicating that internal combustion engines will continue to play a significant role even beyond 2030. This underscores the transitional nature of the automotive industry as it moves towards a more sustainable and electrified future.

Automotive Industry Key Market Players & Competitive Insights

The automotive industry is witnessing intense competition among major market players, driving significant investments in research and development to expand product ranges and enhance industry strength. Entrepreneurs are also taking strategic measures to expand their global influence, including new product development, contractual agreements, mergers and acquisitions, increased investments, and collaboration with other organizations. In such a competitive landscape, companies must offer valuable products to sustain growth and viability.

The global automotive market is characterized by the presence of numerous international and regional companies, all vying for market share. Competition is fierce, with manufacturers competing based on factors such as price, product quality, reliability, and after-sales service. Technological advancements present opportunities for OEM companies to differentiate themselves and gain market traction, particularly those offering advanced features like infotainment systems, advanced security features, and connectivity.

Key players such as Volkswagen AG, Mercedes-Benz Group Corporation, Ford Motor Company, Tesla Inc., Toyota Motor Corporation, and others lead the market with their diverse product offerings, reliability, economy, and advanced technology. While international players dominate, regional and local players also play significant roles.

Major players are expected to strengthen their positions through mergers and acquisitions, expanding their operations and solutions globally. Manufacturers must continuously innovate to adapt to evolving technologies, which ultimately impact the competitiveness of their products in the market.

The automotive manufacturing sector is dynamic and competitive, with a focus on innovation to improve vehicle performance, safety, and efficiency. Recent years have seen increased emphasis on electric and hybrid vehicles to reduce emissions and meet the demand for greener transportation options. Automakers design, manufacture, and assemble vehicles, often operating large factories to produce various parts and assemble them into finished products. As the industry evolves, companies will continue to innovate to meet changing consumer demands and regulatory requirements while maintaining competitiveness in the global market.

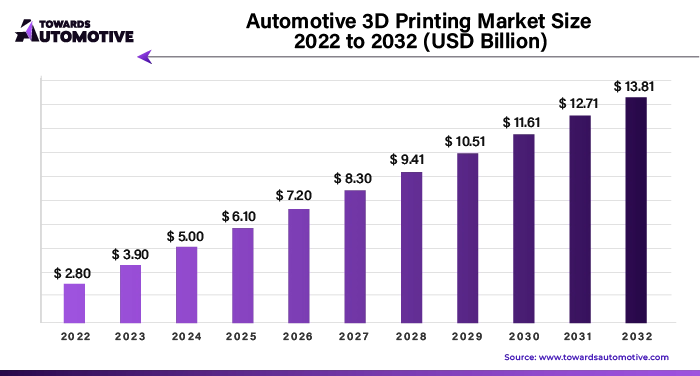

The automotive 3D printing market valued at USD 3.90 billion in 2023, is experiencing steady growth and is projected to exceed USD 13.81 billion by 2032, with a notable CAGR of over 19.40%.

3D printing technology has revolutionized the automotive industry, offering numerous advantages from rapid prototyping to intricate detailing, and even the potential for full vehicle production. Major companies like Mitsubishi Chemical and BASF recognize the immense potential of 3D printing in the automotive sector, viewing it as a lucrative business opportunity.

Automotive companies are increasingly embracing 3D printing technology to drive innovation and improve manufacturing processes. Designers and engineers are leveraging this technology to bring bold ideas to life, enhancing engineering outcomes and streamlining production.

- 3D Printing End-Use Parts: While 3D printing initially served as a tool for rapid prototyping in the automotive industry, it is now increasingly utilized for creating end-use automotive parts. Analysts predict that this segment of the 3D printing market could generate up to $9 billion in revenue by 2029. Leading automotive companies such as Volkswagen, BMW, and Ford are at the forefront of utilizing 3D printing technology to manufacture final car components.

- Effective Materials in Automotive Manufacturing: Fused Filament Fabrication (FFF) is among the most popular 3D printing technologies used in the automotive industry. This method offers versatility, allowing for the use of various materials with properties akin to plastic. By employing 3D printers, companies can produce necessary components in-house, ensuring continuous production and reducing dependency on external suppliers.

Examples of 3D Printing in Automotive

- Electronics Manufacturing: Companies like Bocar utilize 3D printers to create plastic component models, reducing production time significantly. Collaboration with 3DGence resulted in the creation of scaled models, eliminating the need for additional parts like elbows and pipes, ultimately reducing failure rates in hydraulic systems.

- Racing Car Production: Polish students have developed electric racing cars using 3D printed materials. The AGH Racing - RTE 2.0 - LEM electric racing car, introduced in 2019, featured components produced through 3D printing. Advanced solutions, including 3D printing, were utilized to create aerodynamic elements and molds for racing car parts.

- Dynamic Developments and Market Growth: The 3D printing industry is experiencing dynamic growth, with established companies shifting their focus to cater to aerospace and automotive industries' specific needs. The market is evolving rapidly, with a focus on delivering high-quality equipment at reasonable prices to drive innovation and maintain competitiveness.

3D printing technology continues to transform the automotive industry, offering innovative solutions for rapid prototyping, manufacturing, and customization. With ongoing advancements and market growth, leveraging 3D printing capabilities presents significant opportunities for automotive manufacturers to stay ahead in a competitive landscape.

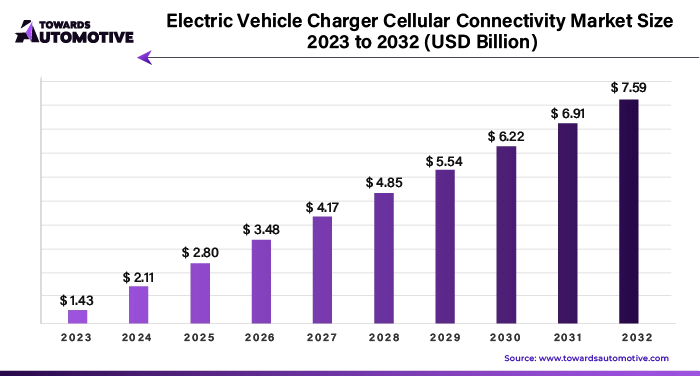

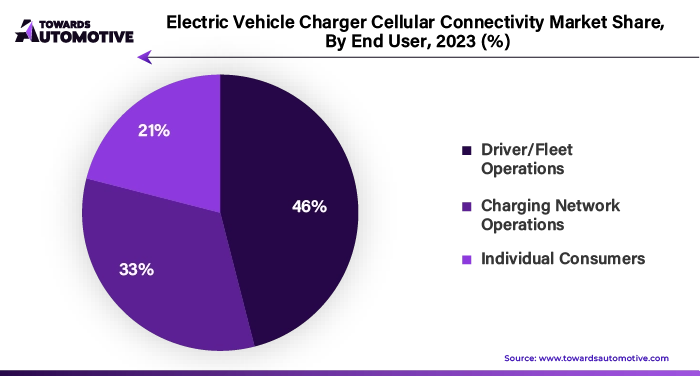

The electric vehicle charger cellular connectivity market valued at USD 1.43 billion in 2023, is experiencing steady growth and is projected to exceed USD 7.59 billion by 2032, with a notable CAGR of over 20.38%.

As the world shifts towards electric vehicles (EVs), developing EV charging infrastructure is paramount to support this transition. With the anticipated surge in EV adoption, the demand for electric car parks and charging stations continues to rise. Establishing a robust charging station network is essential to ensure convenient and efficient charging for EV owners. Regarding connecting these stations, two popular options are cellular and Wi-Fi connections, each with advantages and considerations.

Cellular vs. Wi-Fi Connection:

Cellular Connection:

- Data Security and Privacy: Chargers with 4G LTE-based SIM cards offer enhanced data security and privacy compared to Wi-Fi connections. Cellular networks operate on controlled, licensed bands, ensuring reliability and minimizing interference.

- Stability and Reliability: Cellular connections are stable and reliable, even in remote areas where Wi-Fi signals may be weak or non-existent. This is crucial as the demand for EV chargers grows and charger networks expand.

- Remote Access and Management: 4G cellular networks enable remote access to chargers, allowing for efficient monitoring, updates, and maintenance without on-site visits. Charger owners can remotely monitor performance, analyze data, and optimize operations, improving customer satisfaction and network efficiency.

Wi-Fi Connection

- Cost and Accessibility: Wi-Fi connections are commonly used for home charging stations due to their affordability and accessibility. However, Wi-Fi may require additional control and security measures for public EV chargers.

- Signal Strength and Dependence: Wi-Fi signal strength depends on the quality of the local network, which may vary and could result in limitations in certain areas. Charger hosts relying solely on Wi-Fi may need help in areas with poor connectivity.

- Security Risks: Chargers connected to Wi-Fi networks may expose the charger and the network to security risks. External threats could exploit vulnerabilities to access sensitive data or compromise the network's security.

While cellular and Wi-Fi connections have advantages, cellular connectivity offers greater security, stability, and remote access capabilities for commercial EV chargers. With the increasing demand for EV charging infrastructure, prioritizing the adoption of 4G cellular networks can enhance charging stations' efficiency, security, and performance, contributing to the widespread adoption of electric vehicles and sustainable transportation.

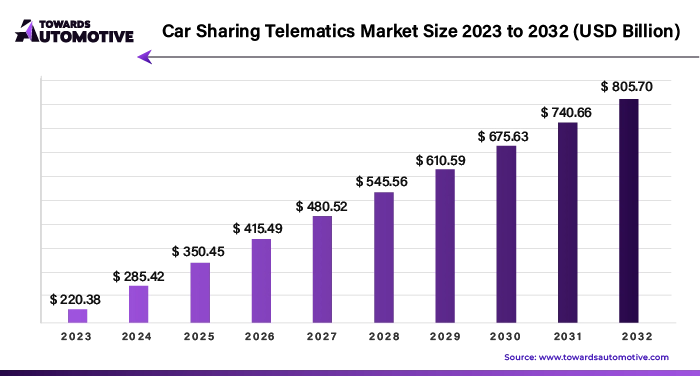

The car sharing telematics market valued at USD 220.38 million in 2023, is experiencing steady growth and is projected to exceed USD 805.70 million by 2032, with a notable CAGR of over 15.49%.

The remote data communication market for car sharing services is experiencing significant growth driven by several key factors. As more people opt for shared mobility solutions over car ownership, the demand for efficient and reliable car sharing services is increasing. This trend is fueled by urbanization, changing consumer preferences, and the availability of affordable and convenient transportation options. The integration of telematics with other emerging technologies such as GPS, IoT, and artificial intelligence further enhances the capabilities of shared vehicles, enabling better tracking, remote monitoring, and predictive maintenance.

The market analysis indicates a robust growth trajectory for the ridesharing remote information market, with a projected Compound Annual Growth Rate (CAGR) over the forecast period. This growth is attributed to advancements in IoV technology, which have improved the efficiency and functionality of shared vehicles. Additionally, the growing demand for flexible and cost-effective transportation solutions is driving the adoption of ride-sharing services, thereby increasing the need for efficient telematics solutions.

Several leading players dominate the car sharing remote data operation market, including companies like INVERS, Vulog, and Ridecell. These companies offer comprehensive solutions encompassing hardware, software, and consulting services to cater to the diverse needs of ridesharing operators. INVERS, in particular, stands out as a market leader with its long history and innovative solutions that have contributed significantly to the growth of the car sharing market.

As the market continues to expand, there are ample opportunities for ridesharing telematics companies to capitalize on the growing demand for shared services and the increasing need for efficient fleet management. The adoption of remote data communication can enhance business efficiency and reduce costs by providing tracking, monitoring, and communication capabilities to ridesharing companies. With factors such as rapid urbanization, smart city strategies, and advancements in IoT and AI technology driving market growth, the future prospects for ridesharing telematics companies are promising.

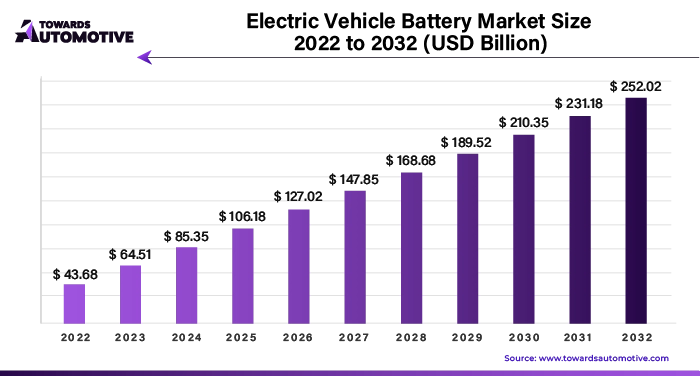

The electric vehicle battery market valued at USD 64.51 billion in 2023, is experiencing steady growth and is projected to exceed USD 252.02 billion by 2032, with a notable CAGR of over 21.50%.

Energy storage systems, typically in the form of batteries, play a crucial role in electric vehicles (EVs), plug-in hybrid electric vehicles (PHEVs), and hybrid electric vehicles (HEVs). These systems enable the storage and distribution of electrical energy, powering the vehicle's propulsion and auxiliary systems. Here are the main types of energy storage systems used in such vehicles:

- Lithium-Ion Batteries: Lithium-ion batteries are widely used in electric vehicles and plug-in hybrids due to their high energy density, good power-to-weight ratio, and long cycle life. They offer excellent energy efficiency, temperature performance, and low self-discharge rates. However, challenges such as cost, lifespan, cobalt consumption, and safety concerns in certain failure scenarios are areas of ongoing research and development.

- Nickel Metal Hydride (NiMH) Batteries: NiMH batteries are prevalent in hybrid vehicles for their durability, safety, and resistance to abuse. Although they have a longer lifespan compared to lead-acid batteries, they face challenges such as high cost and hydrogen loss control.

- Lead-Acid Batteries: Lead-acid batteries are known for their affordability, reliability, and recyclability. While they are commonly used in start-stop systems and some electric vehicles for service transportation, they suffer from limitations such as low power density, poor performance at high temperatures, and short lifespan.

- Supercapacitors: Supercapacitors store energy electrostatically and can provide high power output in short durations. They are often used in conjunction with batteries to supplement power during acceleration and regenerative braking. Supercapacitors offer advantages such as fast charging and discharging capabilities but have limited energy storage compared to batteries.

Recycling of batteries is essential for mitigating environmental impact and conserving valuable resources. As electric vehicles become more prevalent, the battery recycling market is expected to expand. Various recycling techniques are being developed to recover materials such as lithium, cobalt, and nickel from spent batteries. These techniques include smelting, direct recycling, and intermediate processes, each with its advantages and challenges in terms of efficiency, energy consumption, and material recovery.

Overall, advancements in battery technology and recycling processes are critical for ensuring the sustainability and environmental friendliness of electric vehicles. By addressing challenges and improving recycling methods, the industry can enhance the lifecycle sustainability of electric vehicle batteries and promote a cleaner transportation future.

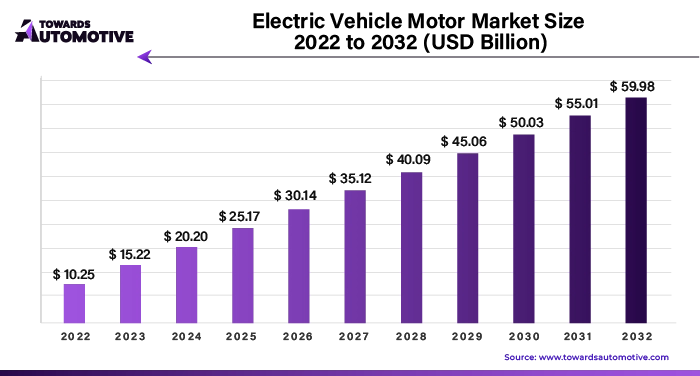

The electric vehicle motor market valued at USD 15.22 billion in 2023, is experiencing steady growth and is projected to exceed USD 59.98 billion by 2032, with a notable CAGR of over 21.69%.

Hybrid electric vehicles (HEVs) have revolutionized vehicle technology by integrating the benefits of both internal combustion engines and electric motors. Here are the main components and functions of hybrid electric cars:

- Battery (Auxiliary): The auxiliary battery in hybrid cars provides the initial power needed to start the vehicle before the main traction battery is activated. It also powers various accessories within the car.

- DC/DC Converter: This device converts the high-voltage direct current (DC) electricity from the traction battery into the lower-voltage DC power required for operating the vehicle's systems and charging the auxiliary battery.

- Generator: Also known as an electric generator, the generator harnesses the kinetic energy generated during braking and converts it into electricity. This energy is then transferred back to the traction battery for storage and later use.

- Electric Traction Motor: The electric traction motor utilizes electricity from the traction battery to drive the wheels of the vehicle. In some hybrid cars, the same motor serves both propulsion and regenerative braking functions.

- Exhaust System: The exhaust system removes exhaust gases produced by the internal combustion engine and expels them from the vehicle. Catalytic converters within the exhaust system help minimize harmful emissions.

- Fuel Fill Port: The fuel fill port is the opening through which gasoline is added to the vehicle's fuel tank.

- Gasoline Tank (Gasoline): The gasoline tank stores the fuel required to power the internal combustion engine.

- Internal Combustion Engine (Spark Ignition): The internal combustion engine burns gasoline to generate mechanical energy, which can directly propel the vehicle or generate electricity for the electric traction motor.

- Power Electronic Controller: This unit manages the flow of power between the traction battery, electric traction motor, and generator. It controls the vehicle's speed and power output to optimize efficiency.

- Thermal System: The thermal management system regulates the temperature of various components within the vehicle, including the engine, electric motor, electrical circuits, and battery pack. Maintaining optimal temperatures ensures efficient operation and reliability.

- Traction Battery Pack: The traction battery pack stores the energy required by the electric traction motor for propulsion. Typically, these battery packs consist of lithium-ion cells designed for longevity and high power output.

By effectively combining these components, hybrid electric vehicles can achieve significant improvements in fuel economy and emissions reduction compared to traditional combustion engine vehicles. Furthermore, the implementation of regenerative braking technology allows for the capture and storage of energy that would otherwise be lost during braking, further enhancing the vehicle's efficiency and performance.

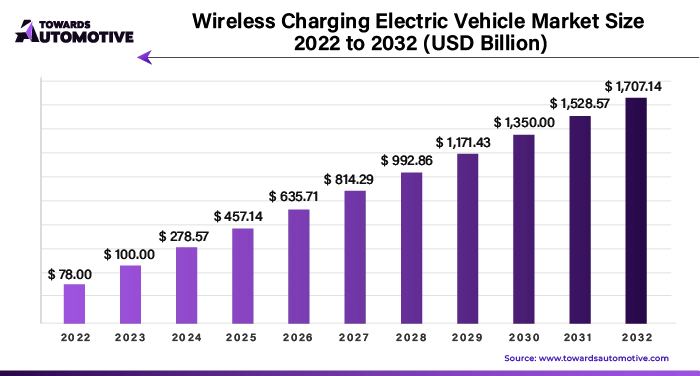

The wireless charging electric vehicle market valued at USD 100 million in 2023, is experiencing steady growth and is projected to exceed USD 1707.14 million by 2032, with a notable CAGR of over 37.06%.

Wireless charging for electric vehicles is a cutting-edge technology that works on the principle of magnetic resonance, where magnetic coils in the charger transfer electricity to corresponding coils installed beneath the vehicle. This method offers efficiency and speed comparable to traditional plug-in charging methods, with wireless chargers boasting an efficiency of 90-93%. While wireless charging currently supports up to 20kW charging power, equivalent to mainstream Level 2 charging speeds, advancements for supercharger-level speeds are anticipated in the future.

Although wireless charging technology has been around for some time, it has gained significant traction in recent years, particularly in the American market. While it has yet to establish a strong foothold in Europe and Asia, American businesses and entrepreneurs are optimistic about its potential, especially given the increasing popularity of electric vehicles.

Currently, only a few electric vehicles, such as the BMW 530e Hybrid Sedan, offer wireless charging as a factory option in the United States. However, there is growing interest in integrating wireless charging capabilities into electric vehicles, with a survey showing that 81% of current and potential electric vehicle owners in the United States are interested in wireless charging capability.

Wireless EV charging comes in two main forms: static charging, where the vehicle remains stationary over wireless charging coils, and dynamic charging, which involves embedding inductive charging technology into roads and highways. Dynamic charging, in particular, has the potential to revolutionize long-distance travel for electric vehicles by enabling continuous charging while driving at speeds of up to 65 mph.

While wireless charging offers numerous advantages, such as eliminating the need for cables, reducing the risk of accidents, and providing greater convenience and time savings, it also presents challenges, particularly in terms of infrastructure cost. Plugless Power, a leader in wireless charging solutions, currently offers third-party wireless chargers priced at around $3,500, excluding installation costs.

Continental AG is a key player in the electric vehicle wireless charging industry, offering a range of safe, efficient, and smart charging solutions for electric cars and trucks worldwide. With innovations in areas such as autonomous driving, connectivity, safety technology, and electric vehicles, Continental is at the forefront of advancing wireless charging technology for the automotive industry.

The company mentioned in the provided information operates multiple subsidiaries with a robust distribution network spanning across North America, Europe, and Asia. Each subsidiary specializes in different aspects of wireless technology and contributes to the advancement of various industries, particularly in transportation and energy management.

Daihen Corporation, headquartered in Japan, is a prominent electronics company with a global presence. It manufactures a wide range of products and systems, including transformers, solar inverters, welding machines, industrial robots, and wireless transmission systems. With 10 sales offices and 8 factories worldwide, Daihen is a key player in providing innovative solutions for diverse industries.

Delachaux Group, based in France, boasts a rich history dating back to 1902. It serves international clients, including major players in the railway, port, and aviation sectors. The group encompasses several brands, such as Frauscher for railway signals, Pandrol for railway infrastructure, and Conductix Wampfler for energy and information management. Delachaux Group's expertise extends across Europe, the Middle East, Africa, the Americas, and the Asia Pacific region.

Electreon, Inc., headquartered in Israel, focuses on developing smart wireless technology for transportation. Specializing in electric vehicles (EVs) and driverless vehicles, Electreon is at the forefront of dynamic wireless charging systems. With ongoing pilot projects in Israel, Italy, and Germany, Electreon is paving the way for efficient and sustainable public transportation solutions.

ELIX Wireless, a Canadian company established in 2013, is dedicated to advancing wireless transmission systems. Using magnetic couplings, ELIX Wireless develops solutions for electric vehicles, warehouse automation, robotics, and automated guided vehicles (AGVs). Their products cater to a wide range of applications, including buses, trucks, coaches, mining equipment, defense systems, and medical devices.

HEVO, Inc., headquartered in Brooklyn, New York, specializes in wireless charging solutions for electric vehicles. Their comprehensive offerings include app and cloud synchronization, power stations, and wireless receivers. With additional offices in Silicon Valley, California, and Amsterdam, Netherlands, HEVO is committed to enhancing the convenience and accessibility of electric vehicle charging infrastructure.

InductEV (formerly Momentum Wireless Power), based in Pennsylvania, USA, focuses on high-power wireless charging solutions. Their magnetic induction systems are designed to charge electric vehicle batteries efficiently, catering to various applications such as city buses, commercial vehicles, boats, and trucks.

Mojo Mobility, Inc. offers a range of solutions in mobile payment, automotive technology, EV charging, and consumer electronics. With a focus on innovation, Mojo Mobility develops cutting-edge wireless charging technology for diverse applications.

WAVE, Inc. (Wireless Advanced Vehicle Electrification) designs and manufactures wireless charging systems for electric buses, with capacities up to 250kW. Their solutions, including the WAVE Salt Lake City Charging Station, enable automated charging for multiple vehicles simultaneously, revolutionizing electric vehicle infrastructure.

Overall, these subsidiaries represent a diverse portfolio of expertise in wireless technology, driving innovation and progress in transportation, energy management, and consumer electronics industries globally. Through their collaborative efforts, they are shaping the future of sustainable and efficient technologies for a better tomorrow.

North America Expected to Have the Highest Growth in the Market

The North American automotive industry holds a significant position globally, with the United States being the largest market in the region. However, the Canadian automotive industry is also experiencing steady growth and is expected to continue expanding. This growth is attributed to various factors, including the continuous development of safety technology in both light commercial vehicles and heavy commercial vehicles, aimed at ensuring drivers' safety. Additionally, government initiatives aimed at enhancing vehicle safety standards further contribute to the demand for vehicles, particularly in the Asia-Pacific region.

In the Asia-Pacific region, China leads as the largest automotive market, while India's automotive sector is witnessing significant growth driven by factors such as the rising middle-income class and a large young population. Japan's automotive industry remains a major player in the region, supported by established companies like Toyota, Honda, and Nissan, which have significantly contributed to the country's economy.

As the automotive industry continues to evolve, major market players are investing heavily in research and development to enhance product offerings. These players are also expanding their international footprint through various strategies such as new product development, mergers and acquisitions, partnerships, and increased investments. Competition in the automotive sector is intense, with companies competing on factors like price, product quality, reliability, and after-sales service.

Key players in the global automotive market include Volkswagen AG, Mercedes-Benz Group Corporation, Ford Motor Company, Tesla Inc., Toyota Motor Corporation, Hyundai Motor Co., Ltd., Nissan Motor Co., Ltd., General Motors Co., and others. These companies strive to offer high-performance vehicles equipped with advanced technology, safety features, and connectivity options to meet consumer demands and gain a competitive edge in the market.

Automakers are increasingly investing in electric and hybrid vehicles to reduce emissions and meet growing demand for sustainable transportation solutions. The automotive manufacturing process is complex and highly competitive, with automakers continuously innovating to improve vehicle performance, safety, and efficiency. These companies typically operate large factories where various components of vehicles are produced and assembled into finished products.

The automotive industry remains a dynamic and evolving sector, with major players constantly striving to stay ahead of the competition by delivering innovative products that meet consumer needs while adhering to stringent safety and environmental standards.

Browse More Insights of Towards Healthcare:

- The market value of automotive Tire Pressure Monitoring Systems (TPMS) to rise from USD 8.38 billion in 2022 and anticipated to reach USD 23.52 billion by 2032, with a CAGR of 10.10% during the forecast period.

- The automotive exhaust analyzer market size was valued at USD 792.47 million in the year 2022 and is projected to grow to USD 1543.35 million in the year 2032, with an expanding CAGR of 7.69% in terms of revenue during the forecasted period.

- The automotive seat market was valued at USD 82.46 billion in the year 2022, and it is expected to reach 143.10 billion by the year 2032 growing at a CAGR of 5.48% during the forecast period.

- The global industry for automotive air suspension systems market size was at USD 19.15 Billion in 2022 estimated to grow at a CAGR of 4.88% from 2023 to 2032 and reach USD 29.41 billion by the end of 2032.

- The global automotive composites market size is projected to grow significantly, reaching USD 21.03 billion by 2032. The market is expected to achieve a double digit CAGR of 10.76% during the forecast period, starting from USD 8.39 billion in 2022.

- The automotive anti-lock braking system market size was valued at USD 59.58 billion in 2022 and is expected to reach USD 131.58 billion by 2032, growing at a CAGR above 9% during the forecast period (2023 - 2032).

- The automotive electronic stability control system market size was valued at USD 40.65 billion in 2022 and is expected to expand to USD 106.91 billion by 2032, with an increase in CAGR of more than 11.34%.

- The automotive interior components market size is anticipated to witness substantial growth, projecting an increase from USD 58.26 Billion in 2023 to USD 84.27 Billion by 2032.The CAGR for the forecast period (2023-2032) is estimated at 4.19%.

- The automotive pneumatic actuator market size was valued at USD 20.04 billion in 2022, is developing strongly. With a predicted value of USD 32.30 billion at the end of the projection period in 2032, it has a CAGR of more than 5.44% from 2023 to 2032.

- The automotive smart key market size is expected to increase from USD 18.25 billion in 2023 to an estimated USD 27.67 billion by 2032, with a compound yearly growth rate (CAGR) of 5.42% over the forecast period (2023-2032).

Automobile Industry Segmentation

Automobile Industry Vehicle Type Outlook

- Passenger Car

- Hatchback

- Sedan

- SUV

- MUV

- Commercial Vehicle

- LCVs

- Heavy Trucks

- Buses & Coaches

Automobile Industry Propulsion Type

- ICE Vehicle

- Electric Vehicle

Automobile Industry Regional Outlook

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Australia

- Rest of Asia-Pacific

- Latin America

- Brazil

- Rest of Latin America

- Middle East and Africa

- South Africa

- Rest of Middle East and Africa

Automotive Industry Recent Developments

- April 2023: Nissan Motor Co. and IBM have initiated a joint research program aimed at leveraging quantum computing to accelerate the development of advanced materials for electric vehicle batteries. The collaboration seeks to enhance battery performance, longevity, and cost-effectiveness, with the ultimate goal of driving the adoption of electric vehicles worldwide.

- August 2023: Volkswagen Group announced its ambitious plans to invest heavily in electric vehicle production, aiming to become the global leader in electric mobility by 2030. The company plans to launch dozens of new electric models across its various brands, leveraging its modular electric vehicle platforms and advanced battery technology to accelerate the transition to sustainable transportation solutions worldwide.

- August 2023: Fiat Chrysler Automobiles (FCA) has deepened its partnership with Verizon Communications to explore the potential of 5G technology in enhancing vehicle connectivity and enabling advanced driver assistance systems (ADAS). The collaboration aims to leverage Verizon's expertise in telecommunications to develop innovative solutions that enhance the safety, efficiency, and convenience of FCA vehicles.

- November 2023: BMW Group and NVIDIA Corporation have announced a strategic collaboration to integrate NVIDIA's AI computing platforms into BMW's vehicles, enabling advanced autonomous driving capabilities and intelligent cockpit features. The partnership aims to leverage NVIDIA's leadership in AI technology to deliver a new level of driving experience and personalized services to BMW customers worldwide.

- January 2024: Audi AG has unveiled plans to establish a dedicated research and development center in Silicon Valley, California, focused on advancing electric vehicle technology and software development. The facility will serve as Audi's hub for collaboration with leading tech companies and startups, with a focus on developing innovative solutions for electric propulsion, autonomous driving, and digital services.

- March 2024: Ford Motor Company and Amazon Web Services (AWS) have announced a strategic partnership to develop a cloud-based platform for Ford's next-generation connected vehicles. The collaboration aims to leverage AWS's expertise in cloud computing and data analytics to enable new features and services, such as over-the-air software updates, predictive maintenance, and personalized driver experiences, while also enhancing vehicle security and privacy.

Acquire our comprehensive analysis today @ https://www.towardsautomotive.com/price/1207

You can place an order or ask any questions, please feel free to contact us at sales@towardsautomotive.com

About Us

Towards Automotive is a premier research firm specializing in the automotive industry. Our experienced team provides comprehensive reports on market trends, technology, and consumer behaviour. We offer tailored research services for global corporations and start-ups, helping them navigate the complex automotive landscape. With a focus on accuracy and integrity, we empower clients with data-driven insights to make informed decisions and stay competitive. Join us on this revolutionary journey as we work together as a strategic partner to reinvent your success in this ever-changing packaging world.

Browse our Brand-New Journal@ https://www.towardspackaging.com

Browse our Brand-New Journal@ https://www.towardshealthcare.com

Browse our Consulting Website@ https://www.precedenceresearch.com

For Latest Update Follow Us: https://www.linkedin.com/company/towards-automotive