BURLINGTON, MA--(Marketwire - Mar 22, 2012) - Despite the progress of residential switch rates, there is still significant market potential for retailers to explore in residential power markets across the United States. In addition, service satisfaction with U.S. residential electricity consumers is significantly higher in open states than in closed states. This appears from the second annual Residential Power Choice Survey by DNV KEMA Energy & Sustainability, which asked U.S. residential electricity consumers to cite factors influencing their choice of electric power providers in their respective states.

DNV KEMA conducted telephone interviews with more than 2,500 residential customers that reside in open states -- states that allow retail competition and active implementation -- as well as in closed states with little to no retail competition. The survey data provides a definitive examination of residential consumer power choices, as well as geographic and segment-level analyses of bridges and barriers to electricity competition and choice, such as satisfaction with service providers.

Competitive retail energy markets primarily aim to reduce consumer costs, which vary widely from state to state. In states with higher electricity costs, such as Hawaii and Connecticut, customers have a strong motivation to explore alternative provider options. However, DNV KEMA's study shows sustained residential migration growth during the past two years as a result of favorable policies, including purchase of receivables (POR), which provides competitive retailers with financial payment protection, and marketer referral programs.

"Sixteen states and the District of Columbia currently have sustainable foundations established to allow competition in retail markets. Each has its own set of unique policies and regulations in regard to retail competition," said Young Kim, associate director of DNV KEMA's Retail Energy Practice. "By surveying residential customers' attitudes, awareness, preferences, and experiences related to energy choice and competition, we can draw conclusive business implications for retailers in open states across the United States."

Key findings of the 2012 Residential Power Choice Survey are as follows:

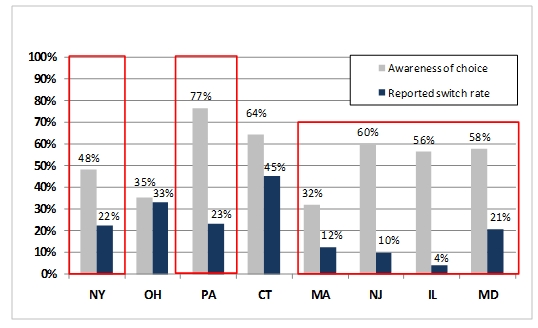

- Marketing potential in residential retail markets is significant in some open states, where the awareness of choice is high, which mainly include Eastern U.S. states, as shown in Figure 1.

- Service satisfaction in open states is significantly higher than in closed states. Sixty percent of residential customers in Texas are satisfied with their retail energy providers, while less than 40 percent of residential customers in closed states are satisfied with their utilities.

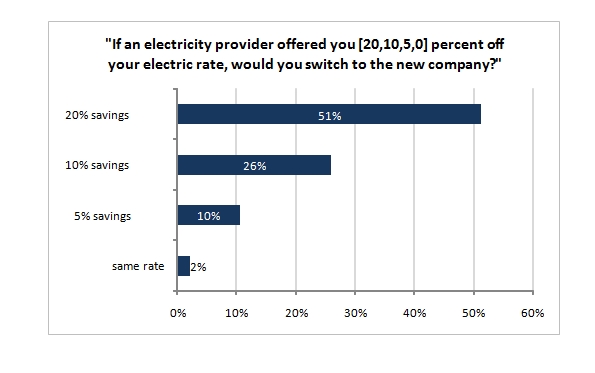

- Cost saving is the primary reason for switching. Approximately half of respondents would switch for a savings of 20 percent off their electric rates, while less than 30 percent would switch for 10 percent off, as shown in Figure 2. In addition, the willingness to switch is higher than average in some open states, most of which are Eastern U.S. states.

- Interest in smart energy offers currently remains low despite increasing deployment of advanced metering in open states. Smart thermostat plans are the most popular program, while the prepay plans are the least popular.

Download the Residential Power Choice Survey executive summary. Subscribers to DNV KEMA's Retail Energy Markets Advisory Service may access the full report, including detailed analyses and data, a variety of cross tabulation analyses and customer geographic and demographic characteristics.

DNV KEMA's 23rd Executive Forum on retail energy will convene in San Antonio, Texas, April 3-4, 2012. This year's event will focus on the unprecedented growth of competitive markets and strategies retailers must use to sustain their momentum.

About DNV KEMA Energy & Sustainability

DNV KEMA Energy & Sustainability, with more than 2,300 experts in over 30 countries around the world, is committed to driving the global transition toward a safe, reliable, efficient, and clean energy future. With a heritage of nearly 150 years, we specialize in providing world-class, innovative solutions in the fields of business & technical consultancy, testing, inspections & certification, risk management, and verification. As an objective and impartial knowledge-based company, we advise and support organizations along the energy value chain: producers, suppliers & end-users of energy; equipment manufacturers; as well as government bodies, corporations, and non-governmental organizations. DNV KEMA Energy & Sustainability is part of DNV, a global provider of services for managing risk with more than 10,000 employees in over 100 countries. For more information on DNV KEMA Energy & Sustainability, visit www.dnvkema.com.

Follow DNV KEMA: Utility of the Future blog; Twitter; LinkedIn