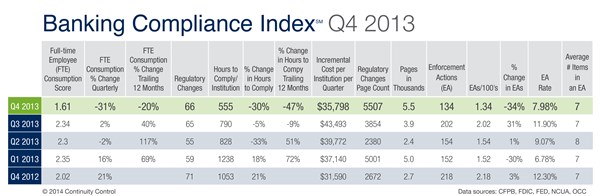

NEW HAVEN, Conn., Jan. 15, 2014 (GLOBE NEWSWIRE) -- Community financial institutions grappled with the toughest regulatory year on record in 2013. With more than 16,000 pages of new regulations added to the books, community banks were forced to expend more than 3,400 additional hours and $150,000 to keep pace with new rules according to the latest Banking Compliance IndexSM (BCI).

The data—compiled and analyzed by experts at Continuity Control™, a New Haven, Conn.-based provider of compliance management systems—shows that financial institutions dealt with 245 new regulatory items in 2013, an average of 61 new regulatory changes each quarter, up nearly 22 percent from 2012. Coping with the extra regulatory load required the average community bank to devote the equivalent of 2.15 full-time employees (FTEs).

Enforcement Actions (EA) escalated in 2013 as well. EAs totaled 642 for the year, or an average of 160 EAs per quarter, up more than 5 percent from 2012. If the current rate of enforcement holds, 8 percent of the industry's financial institutions will be placed under new enforcement actions within the next year. In the fourth quarter, the Federal Deposit Insurance Corp. (FDIC) also cited community banks for having inadequate compliance management systems, revealing a new area of focus for supervising agencies and one that the experts at Continuity Control expect will become more common in 2014.

"Many community financial institutions continue to rely on one or two individuals and antiquated processes to manage compliance," says Pam Perdue, Executive Vice President, Regulatory Insight, at Continuity Control and former Federal Examiner. "It's become untenable for an institution to keep up with all of these changes using current methods. For many banks, they are increasingly discovering that updating their technology can solve the problem better, faster and cheaper."

In terms of additional FTE consumption and hours needed to comply, increases to the regulatory load slowed slightly in the fourth quarter of 2013. However, with increases in regulatory changes and a record number of additional pages, the dip offered no relief to bankers, Perdue says.

"Just because the additional regulatory burden doesn't increase as quickly, doesn't mean the existing requirements disappear," Perdue says. "The BCI shows us the impact of what's being added to an already-enormous pile of regulations. This cumulative effect creates an insurmountable challenge for community banks with their limited resources."

Regulations are expected to increase throughout 2014, and the new rules will have a disproportionate impact on community financial institutions. The Independent Community Bankers of America (ICBA) recently sent a written statement about the issue to Congress, calling on representatives to fix the inequity.

"Crushing regulatory burdens collectively pose the greatest threat to the survival of the community banking industry," said Camden Fine, President and CEO of ICBA, in a recent blog post. "By sapping local institutions of resources they could be devoting to serving their customers and promoting growth, overly burdensome regulations make community banks less competitive, deter de novo charters, and drive industry consolidation."

About the BCI

The BCI is calculated each quarter using a multivariate analysis that can be weighted across different contexts and is calibrated to determine the regulatory impact on financial institutions of varying sizes, product mixes, and regulatory oversight. Using key indicators including volume, velocity and complexity of regulatory change; time expended to meet regulatory requirement(s); and supervision and the enforcement climate, the BCI's sophisticated metrics are unmatched in the industry.

The BCI tracks:

- Regulatory Changes: A total count of applicable financial regulatory changes throughout the quarter.

- Page Volume: The number of pages associated with each of the regulatory changes—indicative of the complexity and workload involved with reviewing and interpreting each change.

- Enforcement Action Information (EA): Analysis of the public enforcement actions that have been issued during a quarter.

The BCI employs a data-driven approach to provide unique insights into the depth and breadth of regulatory compliance workload impact measured in terms of a Full-time Employee (FTE) Consumption Score.

Over 650 financial institution professionals attended the Continuity Control RegAdvisor Quarterly Briefing webcast Thursday, January 9th. During this session regulatory experts reviewed the Q4 2013 BCI metrics and provided in-depth information on the quarter's regulatory changes, a workload assessment of these changes and the required actions to avoid penalties. A recording of this session is available at http://info.continuity.net/q4-2013-regadvisor-briefing

About Continuity Control

Continuity Control is an award-winning regulatory compliance platform that combines advanced software with personalized service to help community financial institutions reduce their regulatory burden. Founded in 2008 by distinguished technology, banking, and compliance specialists, Continuity Control's platform effectively reduces the resources a bank or credit union must spend on compliance while ensuring that it passes regulatory muster. Built just for community banks and credit unions, Continuity Control is the most comprehensive compliance management platform for community financial institutions on the market today.