TRUCKEE, Calif., March 3, 2014 (GLOBE NEWSWIRE) -- Clear Capital®, the premium provider of data and solutions for real estate asset valuation and collateral risk assessment, today released its Home Data Index™ (HDI) Market Report with data through February 2014. Using a broad array of public and proprietary data sources, the HDI Market Report publishes the most granular home data and analysis earlier than nearly any other index provider in the industry.

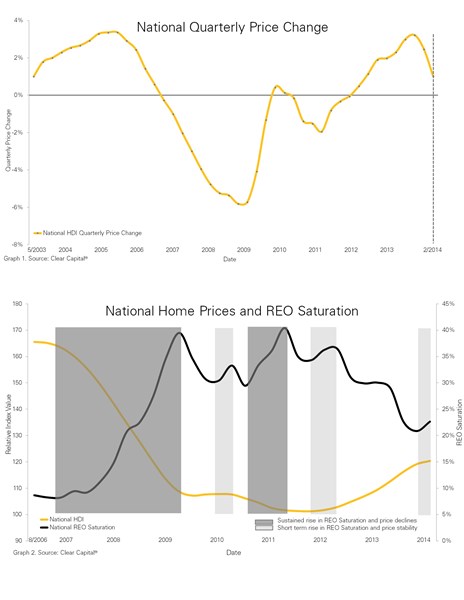

- February national home price gains were notably lower over the quarter, down to 1% from 2.5%. This is the largest drop since 2010, when gains were coming off the first time homebuyer tax credit. As markets adjust to the new normal, 1% is significant; 2014 is only expected to see 3%-5% growth. Graph 1 shows the recent, significant drop in quarterly trends.

- Additionally in February, national REO saturation ticked up 1.8 percentage points from 20.9% to 22.7%, the largest gain since January 2012. Declining quarterly gains coupled with rising REO saturation suggest home prices could see quarterly declines within the next few months. Graph 2 shows how price declines can directly correlate with rising REO saturation over sustained periods.

- With one month of winter to go, moderating prices in the bottom half of the lowest performing metro markets suggest near-term price declines are not out of the question. In February, three out of 15 reported slight declines over the quarter. The remaining 12 metros were mostly flat with not one market reaching 1% growth.

- Jacksonville's REO saturation rose by 3.2 percentage points over the quarter to 43.2%. This is the highest rate of distressed sale activity across the largest 50 metropolitan areas, and the largest quarterly increase for Jacksonville since early 2011. Under the pressure of rising distressed activity, price gains have cooled dramatically. Current quarterly gains of just 0.7% represent the lowest rate of growth for Jacksonville since mid-2011.

- Contact Alanna Harter for your February 2014 file of the Top 30 MSAs or access our data on the Bloomberg Professional service by typing CLCA <GO>.

"A few concerning indicators surfaced in February's home data," said Dr. Alex Villacorta, vice president of research and analytics at Clear Capital. "Our early data shows national quarterly price gains are falling at a rapid pace and suggest overall prices could dip into negative territory soon if current conditions continue. In light of expected waning investor demand, higher rates of distressed sale activity signal that the housing market still must withstand distressed sales, which account for nearly one in four transactions. Since the market fallout in 2006, home prices have dramatically declined during sustained periods of rising distressed sale activity. Over the last two years, however, rising distressed sales have been offset by investor demand, which is not guaranteed to be present in 2014.

Though it is not unusual to see rising distressed activity over the winter months, the current housing picture gives reason to be concerned. If we don't see a correction come spring, the housing market may be in for a long year.

Despite year-end forecasted gains between 3% and 5%, the market is still susceptible to declines. While the industry agrees that 2014 will be a year of moderation, we'll likely see more concern about declines over the next few months as other indices catch up to the Clear Capital HDI™. We'll keep a close eye on our early data and markets like Jacksonville, where rising REO saturation could snowball into declines over the short term."

Graph 1: National Quarterly Price Change and Graph 2: National Home Prices and REO Saturation: http://www.globenewswire.com/newsroom/prs/?pkgid=23874

National, Regional and 30 MSA Price Price Trends for February 2014: http://www.globenewswire.com/newsroom/prs/?pkgid=23875