Reykjavik, 2015-08-24 18:42 CEST (GLOBE NEWSWIRE) -- Reykjavik Energy’s (RE-Orkuveita Reykjavikur) Plan had, at mid-year 2015, returned ISK 7 billion above its goal set in Plan-target in the spring of 2011. The bottom-line results in the company’s consolidated financial statements for H1 2015, approved by the Board of Directors today, were a profit of ISK 2.3 billion.

60% of Plan’s returns through internal improvements

At the end of H1 2015, the Plan had returned RE a better cash position amounting to ISK 52.3 billion. The Plan supposed results of ISK 45.1 billion at that time. Lasting rationalisation of operating cost continuously increases the Plan’s returns. On the other hand, in years 2015 and 2016 considerable investments in utility systems, which were postponed as a part of the Plan, are to be entered into.

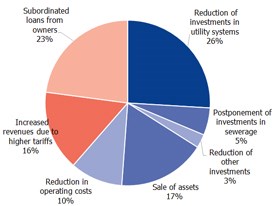

Composition of the Plan’s Yield

The attached graph depicts the share individual components of RE’s Plan have yielded since its initiation April 1st 2011 until mid-year 2015. External factors have contributed 39%, thereof owners’ loans 23% and increased tariffs 16%. Internal measures are responsible for some 60% og the ISK 52 billion improved cash position. Decreased and postponed investments account for 34% and sale of assets 17%. Most importantly, permanent reduction in operating cost have already returned ISK 5 billion, which amounts to 10% of the Plan’s total returns.

Increasing investments

This year has seen considerable investment in utility systems and existing power plants. Additionally, work on several projects that were postponed by RE following the financial crisis, has been resumed. The principal projects are the connection of the Hellisheidi Power Plant to the Hverahlid geothermal field and new sewerages in West-Iceland. Maintenance investments in RE’s utilities will increase and reach a balanced level by year-end 2016.

Fluctuations in electricity purchases

Reykjavik Energy’s general operating costs have been significantly reduced since the Plan’s initiation. Besides selling electricity generated in the Group’s own power plants, it also purchases electricity from Landsvirkjun (National Power Company of Iceland) for resale. The Group also pays for power transmission over the national grid. Because of various internal and external factors, significant fluctuations are in these purchases that appear in the Group’s total operating cost. The increase between H1 2014 and H1 2015 in these purchases were by 28%.

Bjarni Bjarnason, CEO

The operations of the companies within the Reykjavik Energy Group are stable and solid and improved risk management has further reduced fluctuations in results. All RE’s staff strives for rationality and prudence in operations. Thus, we fulfil RE’s role of providing our customers with reliable services at minimum cost.

Managers’ overview

| Operations for the first half of the year | 2011 | 2012 | 2013 | 2014 | 2015 |

| All amounts are in ISK ,000,000 at each year’s price level | |||||

| Revenues | 16,676 | 19,287 | 20,111 | 18,234 | 20,479 |

| Salaries and other expenses | (3,661) | (4,183) | (4,011) | (3,849) | (4,187) |

| Electricity purchases and transmission | (2,502) | (2,377) | (2,668) | (2, 530) | (3,256) |

| EBITDA | 10,512 | 12,727 | 13,432 | 11,855 | 13,036 |

| Depreciation | (4,136) | (4,585) | (4,496) | (4,331) | (4,799) |

| EBIT | 6,376 | 8,142 | 8,936 | 7,524 | 8,237 |

| Result of the period | (3,821) | (924) | 3,736 | 3,831 | 2,260 |

| Cash flow statement: | |||||

| Received interest income | 58 | 40 | 81 | 359 | 252 |

| Paid interest expense | (2,452) | (2,805) | (2,473) | (2,560) | (2,215) |

| Net cash from operating activities | 8,928 | 9,988 | 10,059 | 10,953 | 11,042 |

| Working capital from operation | 8,886 | 10,067 | 11,174 | 9,533 | 10,501 |

Contact:

Bjarni Bjarnason

CEO

+354 516 7707