Dublin, Nov. 13, 2025 (GLOBE NEWSWIRE) -- The "Reverse Logistics Market Outlook 2026-2034: Market Share, and Growth Analysis" report has been added to ResearchAndMarkets.com's offering.

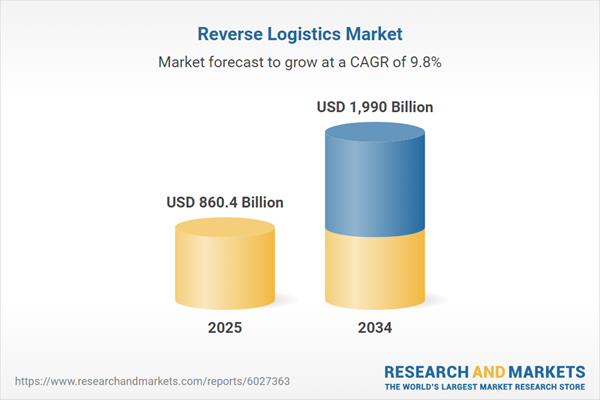

The Reverse Logistics Market is valued at USD 860.4 billion in 2025 and is projected to grow at a CAGR of 9.8% to reach USD 1.99 trillion by 2034

The market is being reshaped by the surge in online purchases and try-before-you-buy models, rising sustainability commitments, and extended producer responsibility frameworks that push closed-loop flows. Leading trends include AI-enabled disposition decisioning at first touch, return-less refunds for low-value items, dynamic routing to consolidation hubs, automated grading and triage using vision systems, and recommerce channels embedded into brand sites and marketplaces.

Driving factors include cost recovery of inventory, brand protection, ESG targets, scarce component recovery, and consumer demand for faster, frictionless returns. The competitive landscape blends parcel carriers, 3PLs, and specialist reverse platforms with OEM service networks and independent repair/refurb players; differentiation centers on speed to resale, recovery rate, fraud prevention, and data visibility.

Key pain points remain: cross-border paperwork and taxes, inconsistent item condition data, high transportation and handling costs, fraud/wardrobing, and complex handling of hazardous/regulated items (batteries, WEEE, pharmaceuticals). As networks redesign for circularity, leaders standardize packaging, digitize RMA and product identity, co-locate forward/reverse nodes, and deploy outcome-based SLAs tied to net recovery value, turnaround time, and landfill diversion - turning reverse logistics from a cost center into a strategic lever for margin, loyalty, and sustainability.

Reverse Logistics Market Reginal Analysis

North America

High e-commerce penetration and generous return policies create large, time-sensitive flows. Networks emphasize box-free drop-off, consolidated first-mile, and near-market refurbishment to speed resale. Electronics and apparel dominate volumes; automotive and home goods add bulky challenges. Providers compete on fraud analytics, recommerce partnerships, and carbon-aware routing. Retailers pilot dynamic return fees to align behavior with cost and sustainability.

Europe

Stringent waste and producer-responsibility rules push formalized take-back, repairability, and recycling, especially for electronics and batteries. Cross-border harmonization, VAT handling, and duty-drawback expertise are differentiators. Brands scale in-country grading hubs to minimize transport. Fashion and consumer tech lead recommerce adoption; refurbishment quality standards and extended warranties build consumer trust.

Asia-Pacific

Rapid growth in marketplace-driven commerce results in fragmented return flows across dense urban and remote geographies. Investments prioritize automated grading, localized repair clusters, and locker/parcel-shop ecosystems. Smartphone and small-electronics returns are high, with component harvesting a material value lever. Emerging policies on EPR and battery/WEEE accelerate formal reverse networks.

Middle East & Africa

E-commerce expansion and cross-border trade drive demand for simplified return paths, consolidation hubs, and bonded facilities. Fashion and electronics dominate early volumes. Infrastructure development focuses on parcel lockers and mall-based drop points; recommerce gains traction via regional platforms. Compliance for lithium batteries and temperature-sensitive goods is a growing capability gap providers aim to fill.

South & Central America

Macroeconomic volatility heightens the importance of value recovery and in-region refurbishment to avoid long international loops. Retailers favor in-store returns and local consolidation to reduce freight costs. Electronics and appliances are key categories; service providers with repair, parts harvesting, and localized resale channels outperform. Regulatory clarity on e-waste and duty management supports network maturation.

Reverse Logistics Market Key Insights

- First-touch disposition is decisive. AI/ML and rules engines use order, color/size sell-through, seasonality, and condition images to choose refund, reroute, repair, or recycle - maximizing net recovery and minimizing touchpoints.

- Recommerce becomes mainstream. Brand-owned resale and marketplace partnerships expand channels for "like-new" and Grade B/C inventory; serialized tracking and cosmetic grading stabilize pricing and trust.

- Automation lifts throughput. Vision grading, automated bagging, putwalls, and AMR-assisted induction cut dwell time and labor variability; facilities shift to U-shaped flows for triage/repair at the edge.

- Omnichannel return options matter. Box-free drop-off, curbside, locker, and mail-in returns reduce friction; dynamic policies (fee thresholds, extended windows) balance CX with cost and fraud risk.

- Sustainability is a selection metric. Landfill diversion, Scope 3 reporting, and recycled content targets influence provider choice; right-sized packaging and low-carbon transport lanes gain weight.

- Battery and hazmat complexity rises. EV and electronics returns require UN/DOT-compliant packaging, state-of-charge protocols, and chemistries-specific recycling - driving specialist partnerships.

- Healthcare and regulated flows. Device reprocessing, cold-chain, and recall execution demand chain-of-custody, sterilization validation, and lot/UDI traceability integrated with RMA systems.

- Fraud and abuse control. Computer vision, velocity checks, and identity scoring curb bracketing/wardrobing; policy engines tailor fees/exemptions by customer value and risk.

- Cross-border orchestration. Duty drawback, IOSS/HS code accuracy, and bonded returns centers reduce tax leakage and accelerate re-market authorization for international orders.

- Outcome-based SLAs. Contracts emphasize net recovery value, time-to-resale, first-pass yield in repair, and refund speed, aligning incentives across brands, platforms, and 3PLs.

Companies Featured

- DHL Supply Chain

- UPS Supply Chain Solutions

- FedEx Supply Chain

- GXO Logistics

- XPO

- Kuehne+Nagel

- DB Schenker

- DSV

- GEODIS

- CEVA Logistics

- Ryder System

- C.H. Robinson

- Inmar Intelligence

- Optoro

- Liquidity Services

Reverse Logistics Market Segmentation

By Return Type

- Recall Returns

- B2B Returns

- Repairable Returns

- End of Use Returns

- End of Life Returns

By Service

- Transportation

- Warehousing

- Reselling

- Replacement Management

- Refund Management

- Others

By End-User

- Retail & E-commerce

- Automotive

- Consumer Electronics

- Healthcare

- Others

For more information about this report visit https://www.researchandmarkets.com/r/4byi7n

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world's leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Attachment