MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

SELECTED FINANCIAL HIGHLIGHTS

(Dollars in thousands except per share September December September

data) 30, 31, 30,

2006 2005 2005

--------- --------- ---------

(Unaudited) (Unaudited)

Selected Financial Condition Data (at end

of period):

Total assets $ 363,191 $ 298,722 $ 280,590

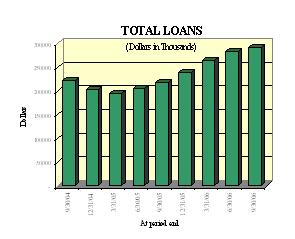

Total loans 292,614 239,771 218,462

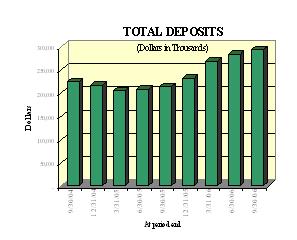

Total deposits 293,494 232,632 213,268

Borrowings 38,307 36,417 36,417

Total shareholders' equity 28,226 26,588 27,900

Selected Statements of Income Data (nine

months and year ended):

Net interest income $ 8,566 $ 9,780 $ 7,100

Income (loss) before taxes 853 (7,364) (6,336)

Net income (loss) 1,378 (7,364) (6,336)

Income (loss) per common share - Basic .40 (2.15) (1.85)

Income (loss) per common share - Diluted .40 (2.15) (1.85)

Three Months Ended

Net interest income $ 2,952 $ 2,680 $ 2,507

Income (loss) before taxes 190 (1,028) (518)

Net income (loss) 690 (1,028) (518)

Income (loss) per common share - Basic .20 (.30) (.15)

Income (loss) per common share - Diluted .20 (.30) (.15)

Selected Financial Ratios and Other Data

(nine months and year ended):

Performance Ratios:

Net interest margin 3.53% 3.64% 3.54%

Efficiency ratio 93.82 160.43 112.11

Return on average assets .54 (2.58) (.73)

Return on average equity 6.71 (25.63) (26.92)

Average total assets $ 341,646 $ 285,896 $ 280,506

Average total shareholders' equity $ 27,440 $ 28,732 $ 28,112

Average loans to average deposits ratio 98.86% 98.17% 99.33%

Common Share Data (at end of period):

Market price per common share $ 10.56 $ 9.10 $ 10.99

Book value per common share $ 8.23 $ 7.76 $ 8.14

Common shares outstanding 3,428,695 3,428,695 3,428,695

Other Data (at end of period):

Allowance for loan losses $ 5,316 $ 6,108 $ 6,589

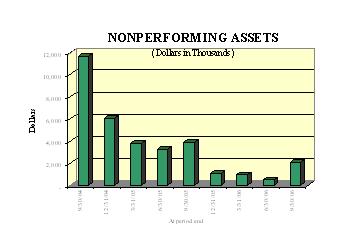

Non-performing assets $ 2,091 $ 1,059 $ 3,905

Allowance for loan losses to total loans 1.82% 2.55% 3.02%

Non-performing assets to total assets .58% .35% 1.39%

Number of:

Branch locations 13 12 12

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

(Dollars in thousands except per share September December September

data) 30, 31, 30,

2006 2005 2005

--------- --------- ---------

(Unaudited) (Unaudited)

ASSETS

Cash and due from banks $ 5,537 $ 4,833 $ 5,333

Federal funds sold 11,949 3,110 4,849

--------- --------- ---------

Cash and cash equivalents 17,486 7,943 10,182

Interest-bearing deposits in other

financial institutions 889 1,025 1,282

Securities available for sale 36,129 34,210 35,506

Federal Home Loan Bank stock 4,152 4,855 4,855

Total loans 292,614 239,771 218,462

Allowance for loan losses (5,316) (6,108) (6,589)

--------- --------- ---------

Net loans 287,298 233,663 211,873

Premises and equipment 12,643 11,987 11,268

Other real estate held for sale 26 945 1,948

Other assets 4,568 4,094 3,676

--------- --------- ---------

Total assets $ 363,191 $ 298,722 $ 280,590

========= ========= =========

LIABILITIES AND SHAREHOLDERS' EQUITY

Liabilities:

Non-interest-bearing deposits $ 22,826 $ 19,684 $ 19,690

Interest-bearing deposits 270,668 212,948 193,578

--------- --------- ---------

Total deposits 293,494 232,632 213,268

Borrowings 38,307 36,417 36,417

Other liabilities 3,164 3,085 3,005

--------- --------- ---------

Total liabilities 334,965 272,134 252,690

Shareholders' equity:

Preferred stock - No par value:

Authorized 500,000 shares, no shares

outstanding - - -

Common stock - No par value:

Authorized 18,000,000 shares

Issued and outstanding - 3,428,695

shares 42,646 42,412 42,412

Accumulated deficit (14,083) (15,461) (14,434)

Accumulated other comprehensive

income (337) (363) (78)

--------- --------- ---------

Total shareholders' equity 28,226 26,588 27,900

--------- --------- ---------

Total liabilities and shareholders'

equity $ 363,191 $ 298,722 $ 280,590

========= ========= =========

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS

(Dollars in thousands except per

share data) Three Months Ended Nine Months Ended

-------------------- --------------------

September September September September

30, 30, 30, 30,

2006 2005 2006 2005

--------- --------- --------- ---------

(Unaudited)(Unaudited)(Unaudited)(Unaudited)

Interest income:

Interest and fees on loans:

Taxable $ 5,635 $ 3,547 $ 15,316 $ 9,807

Tax-exempt 189 222 575 694

Interest on securities:

Taxable 306 282 852 1,178

Tax-exempt 5 42 87 126

Other interest income 268 177 631 470

--------- --------- --------- ---------

Total interest income 6,403 4,270 17,461 12,275

--------- --------- --------- ---------

Interest expense:

Deposits 2,951 1,338 7,540 3,666

Borrowings 500 425 1,355 1,509

--------- --------- --------- ---------

Total interest expense 3,451 1,763 8,895 5,175

--------- --------- --------- ---------

Net interest income 2,952 2,507 8,566 7,100

Provision for loan losses - - (600) -

--------- --------- --------- ---------

Net interest income after

provision for loan losses 2,952 2,507 9,166 7,100

--------- --------- --------- ---------

Other income:

Service fees 133 137 365 470

Loan and lease fees 23 5 59 11

Net security gains (1) (1) (1) 96

Net gains on sale of loans 66 17 149 37

Other 19 96 135 194

--------- --------- --------- ---------

Total other income 240 254 707 808

--------- --------- --------- ---------

Other expenses:

Salaries, commissions, and

related benefits 1,487 1,555 4,577 4,665

Occupancy 333 275 943 748

Furniture and equipment 159 133 470 430

Data processing 176 234 512 726

Accounting, legal, and

consulting fees 341 204 955 750

Loan and deposit expense 78 153 305 696

Telephone 55 66 155 203

Advertising expense 70 314 247 696

Penalty on prepayment of FHLB

borrowings - - - 4,320

Other 303 345 856 1,010

--------- --------- --------- ---------

Total other expenses 3,002 3,279 9,020 14,244

--------- --------- --------- ---------

Income (loss) before income

taxes 190 (518) 853 (6,336)

Provision for (benefit of)

income taxes (500) - (525) -

--------- --------- --------- ---------

Net income (loss) $ 690 $ (518) $ 1,378 $ (6,336)

========= ========= ========= =========

Income (loss) per common share:

Basic $ .20 $ (.15) $ .40 $ (1.85)

========= ========= ========= =========

Diluted $ .20 $ (.15) $ .40 $ (1.85)

========= ========= ========= =========

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

LOAN PORTFOLIO AND CREDIT QUALITY

(Dollars in thousands)

Loan Portfolio Balances (at end of period):

September December September

30, 31, 30,

2006 2005 2005

--------- --------- ---------

Commercial Loans

Hospitality and tourism $ 37,287 $ 37,681 $ 40,424

Real estate - operators of nonresidential

buildings 35,965 28,217 24,837

Real estate agents and managers 19,744 10,588 7,837

New car dealers 10,049 9,995 5,005

Other 102,341 88,842 81,623

--------- --------- ---------

Total Commercial Loans 205,386 175,323 159,726

1-4 family residential real estate 51,341 44,660 42,490

Consumer 2,792 2,285 2,108

Construction 33,095 17,503 14,138

--------- --------- ---------

Total Loans $ 292,614 $ 239,771 $ 218,462

========= ========= =========

Credit Quality (at end of period):

September December September

30, 31, 30,

2006 2005 2005

--------- --------- ---------

Nonperforming Assets

Nonaccrual loans $ 2,065 $ 15 $ 1,957

Loans past due 90 days or more - 99 -

Restructured loans - - -

--------- --------- ---------

Total nonperforming loans 2,065 114 1,957

Other real estate owned 26 945 1,948

--------- --------- ---------

Total nonperforming assets $ 2,091 $ 1,059 $ 3,905

========= ========= =========

Nonperforming loans as a % of loans .71% 0.05% 0.90%

--------- --------- ---------

Nonperforming assets as a % of assets .58% 0.35% 1.39%

--------- --------- ---------

Reserve for Loan Losses:

At period end $ 5,316 $ 6,108 $ 6,589

--------- --------- ---------

As a % of loans 1.82% 2.55% 3.02%

--------- --------- ---------

As a % of nonperforming loans 257.43% 5,357.89% 336.69%

--------- --------- ---------

As a % of nonaccrual loans 257.43% N/M% 336.69%

========= ========= ---------

Charge-off Information:

Average loans $ 271,351 $ 207,928 $ 202,381

--------- --------- ---------

Net charge-offs $ 192 $ 858 $ 377

--------- --------- ---------

Charge-offs as a % of average loans .07% .41% .19%

--------- --------- ---------

MACKINAC FINANCIAL CORPORATION

QUARTERLY FINANCIAL SUMMARY

*(Dollars in thousands, except per share data)

Average

Average Average Average Shareholders'

Quarter Ended Assets Loans Deposits Equity

-------- -------- -------- ------------

September 30, 2006 $ 362,632 $ 289,210 $ 296,608 $ 28,041

June 30, 2006 342,820 273,686 274,591 27,213

March 31, 2006 319,007 250,735 254,720 27,055

December 31, 2005 288,619 224,386 219,967 27,288

September 30, 2005 280,506 209,785 211,197 28,112

June 30, 2005 277,754 197,545 206,875 28,879

March 31, 2005 296,856 199,703 209,035 30,692

December 31, 2004 327,543 218,962 211,685 8,455

September 30, 2004 346,078 226,951 236,418 6,096

Net Book

Return on Average Net Effi- Income Value

---------------- Interest ciency Per Per

Quarter Ended Assets Equity Margin Ratio Share Share

------- ------- ------- ------- ------- --------

September 30, 2006 .75% 9.76% 3.36% 91.17% $ 0.20 $ 7.93

June 30, 2006 .22 2.82 3.62 91.41 0.05 7.93

March 31, 2006 .63 7.47 3.62 99.37 0.15 7.93

December 31, 2005 (1.41) (14.95) 3.96 128.37 (0.30) 7.76

September 30, 2005 (0.73) (7.39) 3.79 112.11 (0.15) 8.14

June 30, 2005 (0.83) (8.01) 3.67 119.07 (0.17) 8.32

March 31, 2005 (7.16) (69.25) 3.21 300.96 (1.53) 8.42

December 31, 2004 2.95 114.17 2.48 71.83 8.25 10.13

September 30, 2004 (0.87) (49.53) 2.25 120.66 (2.17) 18.44

*Historical per share data has been adjusted for the 20:1 reverse stock

split distributed in December 2004.

Contact Information: Contact: Investor Relations (888) 343-8147 Website: www.bankmbank.com