MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

SELECTED FINANCIAL HIGHLIGHTS

For The Years Ended

December 31,

(Dollars in thousands, except per share data) 2008 2007

--------- ---------

(Unaudited) (Unaudited)

Selected Financial Condition Data (at end of

period):

Assets $ 451,431 $ 408,880

Loans 370,280 355,079

Investment securities 47,490 21,597

Deposits 371,097 320,827

Borrowings 36,210 45,949

Shareholders' equity 41,552 39,321

Selected Statements of Income Data:

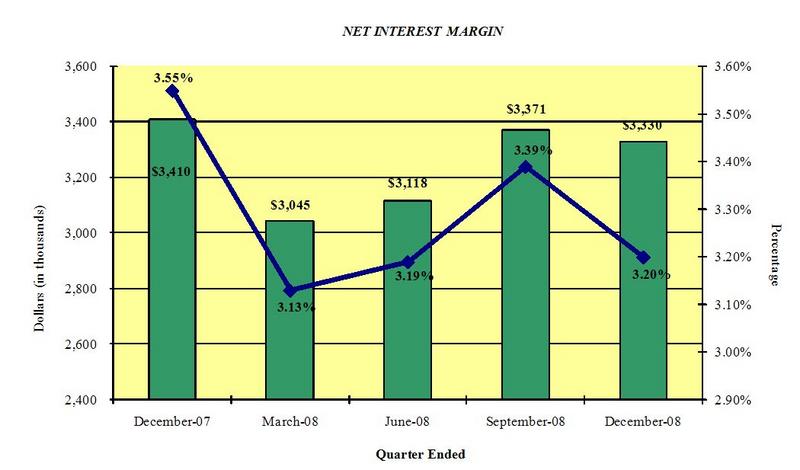

Net interest income $ 12,864 $ 13,417

Income before taxes 2,659 2,923

Net income 1,872 10,163

Income per common share - Basic .55 2.96

Income per common share - Diluted .55 2.96

Weighted average shares outstanding 3,422,012 3,428,695

Selected Financial Ratios and Other Data:

Performance Ratios:

Net interest margin 3.23% 3.60%

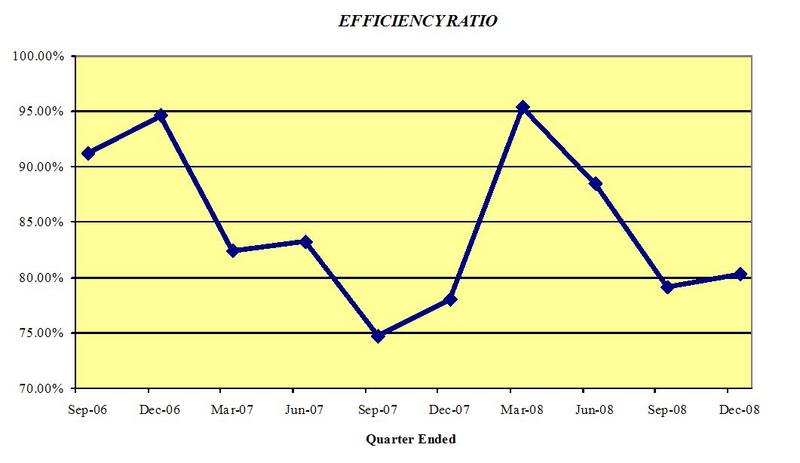

Efficiency ratio 85.51 79.46

Return on average assets .44 2.59

Return on average equity 4.61 31.05

Average total assets $ 425,343 $ 392,313

Average total shareholders' equity 40,630 32,731

Average loans to average deposits ratio 105.61% 104.94%

Common Share Data at end of period:

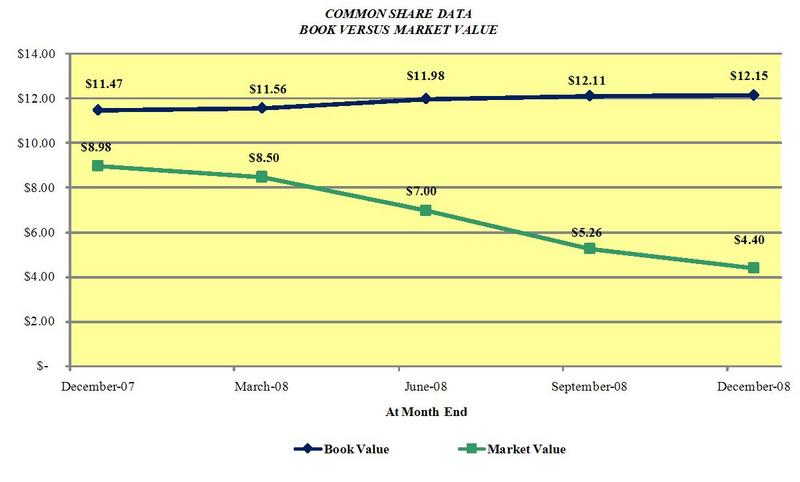

Market price per common share $ 4.40 $ 8.98

Book value per common share $ 12.15 $ 11.47

Common shares outstanding 3,419,736 3,428,695

Other Data at end of period:

Allowance for loan losses $ 4,277 $ 4,146

Non-performing assets $ 7,076 $ 5,234

Allowance for loan losses to total loans 1.16% 1.17%

Non-performing assets to total assets 1.57% 1.28%

Number of:

Branch locations 12 12

FTE Employees 100 100

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

December December

31, 31,

(Dollars in thousands) 2008 2007

--------- ---------

(unaudited) (audited)

ASSETS

Cash and due from banks $ 10,112 $ 6,196

Federal funds sold - 166

--------- ---------

Cash and cash equivalents 10,112 6,362

Interest-bearing deposits in other financial

institutions 582 1,810

Securities available for sale 47,490 21,597

Federal Home Loan Bank stock 3,794 3,794

Loans:

Commercial 296,088 288,839

Mortgage 70,447 62,703

Installment 3,745 3,537

--------- ---------

Total Loans 370,280 355,079

Allowance for loan losses (4,277) (4,146)

--------- ---------

Net loans 366,003 350,933

Premises and equipment 11,189 11,609

Other real estate held for sale 2,189 1,226

Other assets 10,072 11,549

--------- ---------

TOTAL ASSETS $ 451,431 $ 408,880

========= =========

LIABILITIES AND SHAREHOLDERS' EQUITY

Liabilities:

Non-interest-bearing deposits $ 30,099 $ 25,557

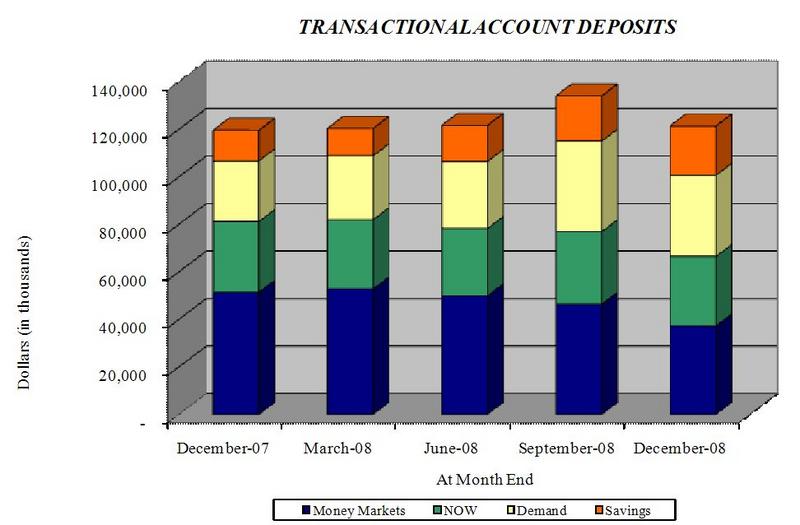

Interest-bearing deposits:

NOW, Money Market, Checking 70,584 81,160

Savings 20,730 12,485

CDs < $100,000 73,752 80,607

CDs > $100,000 25,044 22,355

Brokered 150,888 98,663

--------- ---------

Total deposits 371,097 320,827

Borrowings:

Federal funds purchased - 7,710

Short-term - 1,959

Long-term 36,210 36,280

--------- ---------

Total borrowings 36,210 45,949

Other liabilities 2,572 2,783

--------- ---------

Total liabilities 409,879 369,559

Shareholders' equity:

Preferred stock - No par value:

Authorized 500,000 shares, no shares outstanding

Common stock and additional paid in capital - No

par value

Authorized - 18,000,000 shares

Issued and outstanding - 3,419,736 and

3,428,695, respectively 42,815 42,843

Accumulated deficit (1,708) (3,582)

Accumulated other comprehensive income (loss) 445 60

--------- ---------

Total shareholders' equity 41,552 39,321

--------- ---------

TOTAL LIABILITIES AND SHAREHOLDERS' EQUITY $ 451,431 $ 408,880

========= =========

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS

(Dollars in thousands, except per share For The Years Ended December 31,

data) 2008 2007 2006

--------- -------- --------

INTEREST INCOME: (unaudited)(audited) (audited)

Interest and fees on loans:

Taxable $ 22,555 $ 26,340 $ 21,239

Tax-exempt 404 533 753

Interest on securities:

Taxable 1,293 1,100 1,186

Tax-exempt 5 - 87

Other interest income 305 722 787

--------- -------- --------

Total interest income 24,562 28,695 24,052

--------- -------- --------

INTEREST EXPENSE:

Deposits 10,115 13,224 10,575

Borrowings 1,583 2,054 1,884

--------- -------- --------

Total interest expense 11,698 15,278 12,459

--------- -------- --------

Net interest income 12,864 13,417 11,593

Provision for loan losses 2,300 400 (861)

--------- -------- --------

Net interest income after provision for loan

losses 10,564 13,017 12,454

--------- -------- --------

OTHER INCOME:

Service fees 838 688 547

Net security gains 64 - -

Net gains on sale of secondary market

loans 120 498 197

Proceeds from settlement of lawsuit 3,475 470 -

Other 156 350 239

--------- -------- --------

Total other income 4,653 2,006 983

--------- -------- --------

OTHER EXPENSES:

Salaries and employee benefits 6,886 6,757 6,132

Occupancy 1,374 1,272 1,264

Furniture and equipment 771 678 631

Data processing 844 785 691

Professional service fees 508 532 1,425

Loan and deposit 569 285 392

Telephone 170 228 210

Advertising 305 370 346

Other 1,131 1,193 1,130

--------- -------- --------

Total other expenses 12,558 12,100 12,221

--------- -------- --------

Income (loss) before provision for income

taxes 2,659 2,923 1,216

Provision for (benefit of) income taxes 787 (7,240) (500)

--------- -------- --------

NET INCOME (LOSS) $ 1,872 $ 10,163 $ 1,716

--------- -------- --------

INCOME (LOSS) PER COMMON SHARE

Basic $ .55 $ 2.96 $ .50

========= ======== ========

Diluted $ .55 $ 2.96 $ .50

========= ======== ========

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

LOAN PORTFOLIO AND CREDIT QUALITY

(Dollars in thousands)

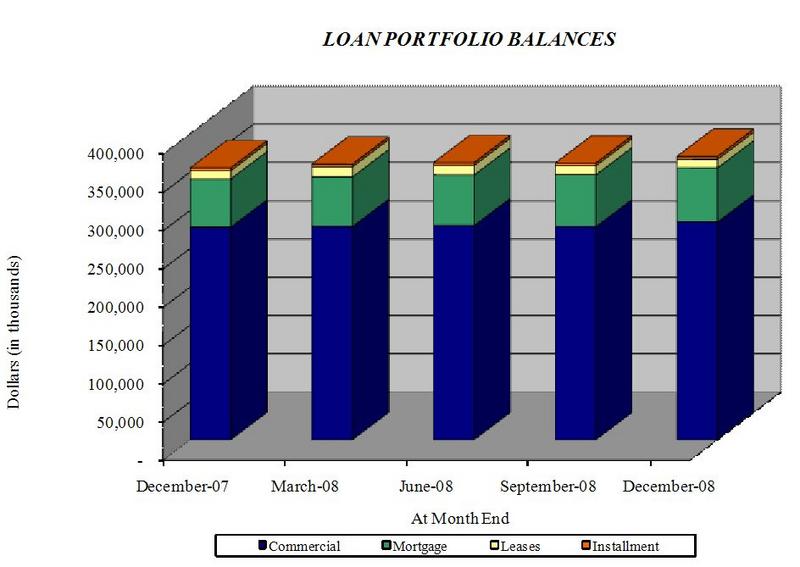

Loan Portfolio Balances (at end of period):

December 31, December 31,

2008 2007

------------ ------------

(unaudited) (audited)

Commercial Loans:

Real estate - operators of nonresidential

buildings $ 41,299 $ 41,597

Hospitality and tourism 35,086 37,604

Real estate agents and managers 29,292 29,571

Operators of nonresidential buildings 13,467 10,569

Other 145,831 130,546

------------ ------------

Total Commercial Loans 264,975 249,887

1-4 family residential real estate 65,595 57,613

Consumer 3,745 3,537

Construction

Commercial 31,113 38,952

Consumer 4,852 5,090

------------ ------------

Total Loans $ 370,280 $ 355,079

============ ============

Credit Quality (at end of period):

December 31, December 31,

2008 2007

----------- -----------

(unaudited) (audited)

Nonperforming Assets :

Nonaccrual loans $ 4,887 $ 3,298

Loans past due 90 days or more - 710

----------- -----------

Total nonperforming loans 4,887 4,008

Other real estate owned 2,189 1,226

----------- -----------

Total nonperforming assets $ 7,076 $ 5,234

=========== ===========

Nonperforming loans as a % of loans 1.32% 1.13%

----------- -----------

Nonperforming assets as a % of assets 1.57% 1.28%

----------- -----------

Reserve for Loan Losses:

At period end $ 4,277 $ 4,146

----------- -----------

As a % of average loans 1.18% 1.24%

----------- -----------

As a % of nonperforming loans 87.52% 103.44%

----------- -----------

As a % of nonaccrual loans 87.52% 125.71%

=========== ===========

Charge-off Information (year to date):

Average loans 361,324 333,415

----------- -----------

Net charge-offs 2,168 1,260

----------- -----------

Charge-offs as a % of average loans .60% .38%

----------- -----------

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

QUARTERLY FINANCIAL HIGHLIGHTS

QUARTER ENDED

(Unaudited)

December September December

31, 30, June 30, March 31, 31,

2008 2008 2008 2008 2007

--------- ---------- ---------- ---------- ----------

BALANCE SHEET

(Dollars in

thousands)

Total loans $ 370,280 $ 361,521 $ 362,122 $ 360,056 $ 355,079

Allowance for

loan losses (4,277) (3,385) (3,585) (3,924) (4,146)

--------- ---------- ---------- ---------- ----------

Total loans,

net 366,003 358,136 358,537 356,132 350,933

Intangible

assets 46 65 85 104 124

Total assets 451,431 440,953 437,327 417,175 408,880

Core deposits 195,165 208,940 200,293 203,445 199,809

Noncore

deposits (1) 175,932 151,754 156,683 122,602 121,018

--------- ---------- ---------- ---------- ----------

Total

deposits 371,097 360,694 356,976 326,047 320,827

Total

borrowings 36,210 36,210 36,280 48,849 45,949

Total

shareholders'

equity 41,552 41,427 40,975 39,633 39,321

Total shares

outstanding 3,419,736 3,419,736 3,419,736 3,428,695 3,428,695

AVERAGE BALANCES

(Dollars in

thousands)

Assets $ 441,583 $ 423,702 $ 418,246 $ 417,682 $ 406,308

Loans 366,077 358,844 362,574 357,778 350,050

Deposits 358,213 341,377 332,725 336,016 324,194

Equity 41,516 41,097 40,399 39,491 38,973

INCOME STATEMENT

(Dollars in

thousands)

Net interest

income $ 3,330 $ 3,371 $ 3,118 $ 3,045 $ 3,410

Provision for

loan losses 1,100 450 750 - -

--------- ---------- ---------- ---------- ----------

Net interest

income

after

provision 2,230 2,921 2,368 3,045 3,410

Total

noninterest

income 308 288 3,747 310 355

Total

noninterest

expense 2,961 2,935 3,471 3,191 2,978

--------- ---------- ---------- ---------- ----------

Income before

taxes (423) 274 2,644 164 787

Provision for

income taxes (171) 58 875 25 260

--------- ---------- ---------- ---------- ----------

Net income $ (252) $ 216 $ 1,769 $ 139 $ 527

========= ========== ========== ========== ==========

PER SHARE DATA

Earnings -

basic $ (.07) $ .06 $ .52 $ .04 $ .15

Earnings -

diluted (.07) .06 .52 .04 .15

Book value 12.15 12.11 11.98 11.56 11.47

Market value,

closing price 4.40 5.26 7.00 8.50 8.98

ASSET QUALITY RATIOS

Nonperforming

loans/total

loans 1.32% 1.29% 1.27% .94% 1.13%

Nonperforming

assets/total

assets 1.57 1.45 1.83 1.08 1.28

Allowance for

loan losses/

total loans 1.16 .94 .99 1.09 1.17

Allowance for

loan losses/

nonperforming

loans 87.52 72.81 77.22 116.06 103.42

PROFITABILITY RATIOS

Return on

average assets (.23)% .20% 1.70% .13% .51%

Return on

average equity (2.42) 2.08 17.62 1.42 5.36

Net interest

margin 3.20 3.39 3.19 3.13 3.55

Efficiency

ratio 80.30 79.12 88.45 95.34 78.02

Average loans/

average deposits 102.20 105.12 108.97 106.48 107.98

CAPITAL ADEQUACY RATIOS

Leverage ratio 8.01% 8.31% 8.56% 7.85% 8.05%

Tier 1 capital

ratio 9.25 9.40 9.48 8.84 8.97

Total capital

ratio 10.38 10.31 10.45 9.92 10.13

Average

equity/average

assets 9.40 9.70 9.66 9.45 9.59

Tangible

equity/tangible

assets 9.20 9.38 9.35 9.48 9.59

(1) Noncore deposits includes Internet CDs, brokered deposits and CDs

greater than $100,000

Contact Information: Contact: Investor Relations (888) 343-8147 Website: www.bankmbank.com