Contact Information: Contact Dave Blumberg TransUnion Telephone (312) 985-3059

TransUnion Study Finds More Consumers Making Payments on Their Credit Cards Before Their Mortgages

"New" Payment Hierarchy May Be Here to Stay

| Source: TransUnion

CHICAGO, IL--(Marketwire - February 3, 2010) - A new study developed by TransUnion confirms

that the "new" payment hierarchy -- where consumers pay their credit cards

prior to their mortgages -- is continuing, with the trend occurring more

readily than ever before.

"Conventional wisdom has always been that, when faced with a financial

crisis, consumers will pay their secured obligations first, specifically

their mortgages," said Sean Reardon, the author of the

study and a consultant in TransUnion's analytics and decisioning services

business unit. "However, a recent TransUnion analysis has found that

increasingly more consumers are paying their credit cards before making

mortgage payments. This analysis reaffirms the results of a previous

TransUnion study that examined data between the third quarter of 2006 and

the first quarter of 2008."

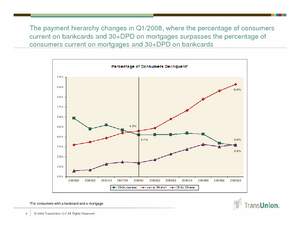

The percentage of consumers current on credit cards

and delinquent on mortgages first

surpassed the percentage of consumers current on their mortgages and

delinquent on credit cards in the first quarter of 2008. This "flip" is

representative of the change in the conventional wisdom around the payment

hierarchy, or which debt obligations consumers would choose to pay first.

The latest study, conducted on consumers that had at least one credit card

and one mortgage, examined 30-day credit card and mortgage delinquency data

between the second quarter of 2008 (Q2/2008) and the third quarter of 2009

(Q3/2009). Although many industry analysts believed that a reversion to

the conventional payment hierarchy would ensue once we had passed through

the worst of the recession -- that has not, in fact, been the case. To the

contrary, this study found that the hierarchy reversal has become even more

widespread, with the percentage of consumers who are delinquent on their

mortgages and current on their credit cards rising to 6.6 percent in

Q3/2009 (from 4.3 percent in Q1/2008). Conversely, the percentage of

consumers who are delinquent on their credit cards and current on their

mortgages has decreased to 3.6 percent in Q3/2009 (from 4.1 percent in

Q1/2008).

"This same trend is evident within the lowest scoring risk segment," added

Reardon. "Moreover, it should be noted that the 'flip' in payment

hierarchy in the lowest scoring segment was evident earlier during Q4/2007,

compared to Q1/2008 for the total market."

The study found that the magnitude of delinquency in the lowest scoring

segment is significantly higher than that of the total market. The

delinquency rate for consumers in this segment who were delinquent on their

mortgages but current on their credit cards during Q4/2007 was 19.1

percent, and rose to 29 percent in Q3/2009. In a trend similar to that of

the total market, the percentage of consumers delinquent on their credit

cards but current on their mortgages decreased from 18.1 percent in Q1/2008

to 14.5 percent in Q3/2009.

The payment hierarchy shifts are even more pronounced in states such as

California and Florida that experienced a more severe housing bubble

effect. Within California, the percentage of consumers delinquent on their

mortgages but current on their credit cards increased from 3.5 percent in

Q3/2007 to 10.2 percent in Q3/2009 (a 191 percent increase). In Florida,

this same variable increased from 5.1 percent in Q3/2007 to 12.4 percent in

Q3/2009 (a 143 percent increase). In this same timeframe, the United States

experienced a 68 percent increase (from 4.0 percent in Q3/2007 to 6.6

percent in Q3/2009).

In contrast, the number of California consumers delinquent on their credit

cards but current on their mortgages declined from 3.3 percent in Q3/2007

to 2.7 percent in Q3/2009. In Florida, this variable declined from 5.0

percent in Q3/2007 to 3.9 percent in Q3/2009.

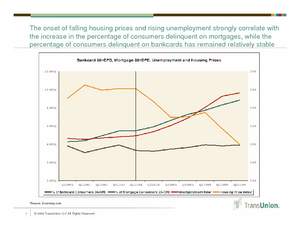

"The implosion of the mortgage industry over the last 24 months, the

resetting of adjustable-rate mortgages and the weak job market have all

come together to redefine how consumers are managing their finances and

meeting (or not meeting) their credit obligations," said Ezra Becker, director

of consulting and strategy in TransUnion's financial services business

unit. "The insight gained through this analysis reveals a lot about

changing consumer preferences. The financial services industry must

recognize and adjust to the payment hierarchy shift with judicious

modifications to business models, new assessments of specific areas of

risk, and by strategic revisions to acquisition and account management

strategies."

The source of the underlying data used for this analysis was TransUnion's Trend Data, a proprietary historical

database consisting of 27 million anonymous consumer records randomly

sampled every quarter from TransUnion's national consumer credit database.

Using TransUnion's standard definitions of credit card and mortgage trades,

TransUnion was able to create and evaluate the custom attributes that are

the basis of this study.

About TransUnion

As a global leader in credit and information management, TransUnion creates

advantages for millions of people around the world by gathering, analyzing

and delivering information. For businesses, TransUnion helps improve

efficiency, manage risk, reduce costs and increase revenue by delivering

comprehensive data and advanced analytics and decisioning. For consumers,

TransUnion provides the tools, resources and education to help manage their

credit health and achieve their financial goals. Through these and other

efforts, TransUnion is working to build stronger economies worldwide.

Founded in 1968 and headquartered in Chicago, TransUnion has employees in

more than 25 countries on five continents. www.transunion.com/business