MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

SELECTED FINANCIAL HIGHLIGHTS

(Dollars in thousands, except per

share data) For The Period Ended

-------------------------------------

September 30, December 31, September 30,

2010 2009 2009

----------- ----------- -----------

(Unaudited) (Unaudited)

Selected Financial Condition Data

(at end of period):

Assets $ 499,006 $ 515,377 $ 513,180

Loans 382,727 384,310 384,100

Investment securities 37,450 46,513 80,203

Deposits 404,524 421,389 418,581

Borrowings 36,069 36,140 36,140

Shareholders' Equity 55,987 55,299 55,766

Selected Statements of Income Data

(nine months and year ended):

Net interest income $ 12,109 $ 16,287 $ 11,856

Provision for loan losses 4,700 3,700 1,400

Income (Loss) before taxes and

preferred dividend (3,103) 3,536 3,552

Net income 934 1,907 2,087

Income per common share - Basic .27 .56 .61

Income per common share - Diluted .27 .56 .61

Three Months Ended:

Net interest income $ 4,064 $ 4,431 $ 4,310

Income (Loss) before taxes and

preferred dividend 111 (16) 2,585

Net income (Loss) (104) (180) 1,536

Income (Loss) per common share -

Basic (.03) (.05) .45

Income (Loss) per common share -

Diluted (.03) (.05) .45

Weighted average shares outstanding 3,419,736 3,419,736 3,419,736

Selected Financial Ratios and Other

Data (nine months and year ended):

Performance Ratios:

Net interest margin 3.59% 3.59% 3.54%

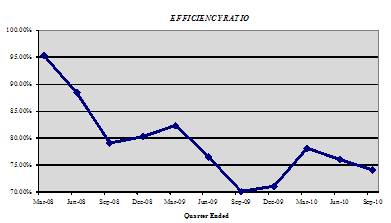

Efficiency ratio 74.12 73.37 77.71

Return on average assets .25 .39 .57

Return on average equity 2.21 3.77 5.72

Average total assets $ 507,938 $ 493,652 $ 486,760

Average total shareholders' equity $ 56,561 $ 50,531 $ 48,801

Average loans to average deposits

ratio 93.19% 92.99% 93.22%

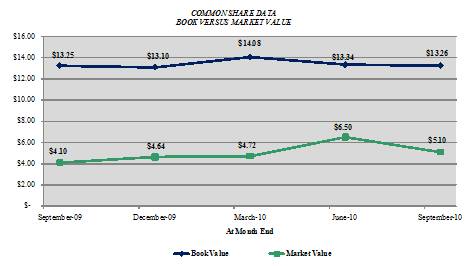

Common Share Data (at end of

period):

Market price per common share $ 5.10 $ 4.64 $ 4.10

Book value per common share $ 13.26 $ 13.10 $ 13.25

Common shares outstanding 3,419,736 3,419,736 3,419,736

Other Data (at end of period):

Allowance for loan losses $ 5,437 $ 5,225 $ 4,081

Non-performing assets $ 17,005 $ 21,041 $ 17,349

Allowance for loan losses to total

loans 1.42% 1.36% 1.06%

Non-performing assets to total

assets 3.41% 4.08% 3.38%

Texas Ratio* 27.68% 34.77% 28.99%

Number of:

Branch locations 11 10 10

FTE Employees 98 100 97

* Texas Ratio: Non-performing Assets divided by Total Equity plus

Allowance for Loan Losses

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

September 30, December 31, September 30,

(Dollars in thousands) 2010 2009 2009

----------- ----------- -----------

(Unaudited) (Unaudited)

ASSETS

Cash and due from banks $ 36,561 $ 18,433 $ 23,249

Federal funds sold 12,000 27,000 -

----------- ----------- -----------

Cash and cash equivalents 48,561 45,433 23,249

Interest-bearing deposits in other

financial institutions 692 678 662

Securities available for sale 37,450 46,513 80,203

Federal Home Loan Bank stock 3,794 3,794 3,794

Loans:

Commercial 295,262 305,670 306,590

Mortgage 82,312 74,350 73,116

Installment 5,153 4,290 4,394

----------- ----------- -----------

Total Loans 382,727 384,310 384,100

Allowance for loan losses (5,437) (5,225) (4,081)

----------- ----------- -----------

Net loans 377,290 379,085 380,019

Premises and equipment 9,843 10,165 10,281

Other real estate held for sale 5,758 5,804 5,821

Other assets 15,618 23,905 9,151

----------- ----------- -----------

TOTAL ASSETS $ 499,006 $ 515,377 $ 513,180

=========== =========== ===========

LIABILITIES AND SHAREHOLDERS' EQUITY

LIABILITIES:

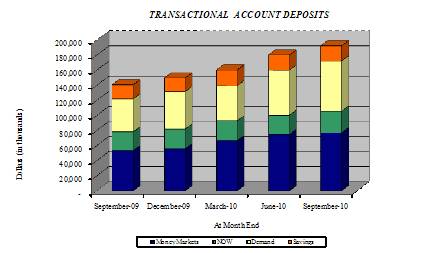

Deposits:

Noninterest bearing deposits $ 44,402 $ 35,878 $ 33,254

NOW, money market, checking 127,828 95,790 88,843

Savings 20,265 18,207 18,807

CDs < $100,000 94,560 59,953 59,637

CDs > $100,000 22,809 36,385 25,409

Brokered 94,660 175,176 192,631

----------- ----------- -----------

Total deposits 404,524 421,389 418,581

Borrowings:

Federal Home Loan Bank 35,000 35,000 35,000

Other 1,069 1,140 1,140

----------- ----------- -----------

Total borrowings 36,069 36,140 36,140

Other liabilities 2,426 2,549 2,693

----------- ----------- -----------

Total liabilities 443,019 460,078 457,414

TOTAL SHAREHOLDERS' EQUITY 55,987 55,299 55,766

----------- ----------- -----------

TOTAL LIABILITIES AND SHAREHOLDERS'

EQUITY $ 499,006 $ 515,377 $ 513,180

=========== =========== ===========

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS

(Dollars in thousands except per

share data) Three Months Ended Nine Months Ended

September 30, September 30,

------------------- -------------------

2010 2009 2010 2009

-------- --------- -------- ---------

(Unaudited) (Unaudited)

INTEREST INCOME:

Interest and fees on loans:

Taxable $ 5,300 $ 5,106 $ 15,718 $ 15,212

Tax-exempt 46 63 145 237

Interest on securities:

Taxable 324 888 1,077 2,020

Tax-exempt 7 7 21 11

Other interest income 23 28 100 44

-------- --------- -------- ---------

Total interest income 5,700 6,092 17,061 17,524

-------- --------- -------- ---------

INTEREST EXPENSE:

Deposits 1,414 1,550 4,309 4,894

Borrowings 222 232 643 774

-------- --------- -------- ---------

Total interest expense 1,636 1,782 4,952 5,668

-------- --------- -------- ---------

Net interest income 4,064 4,310 12,109 11,856

Provision for loan losses 1,000 700 4,700 1,400

-------- --------- -------- ---------

Net interest income after provision

for loan losses 3,064 3,610 7,409 10,456

-------- --------- -------- ---------

OTHER INCOME:

Service fees 264 235 737 750

Net security gains (1) 644 215 644

Net gains on sale of secondary

market loans 322 247 897 389

Other 63 1,292 199 1,465

-------- --------- -------- ---------

Total other income 648 2,418 2,048 3,248

-------- --------- -------- ---------

OTHER EXPENSES:

Salaries and employee benefits 1,779 1,603 5,281 4,761

Occupancy 358 336 1,048 1,069

Furniture and equipment 202 193 593 604

Data processing 193 221 587 665

Professional service fees 168 161 502 458

Loan and deposit 441 402 3,297 1,175

Telephone 53 50 145 139

Advertising 77 80 220 238

Other 330 397 887 1,043

-------- --------- -------- ---------

Total other expenses 3,601 3,443 12,560 10,152

-------- --------- -------- ---------

Income (Loss) before provision for

income taxes 111 2,585 (3,103) 3,552

Provision for (benefit of) income

taxes 30 864 (4,593) 1,142

-------- --------- -------- ---------

NET INCOME (LOSS) 81 1,721 1,490 2,410

-------- --------- -------- ---------

Preferred dividend expense 185 185 556 323

-------- --------- -------- ---------

NET INCOME (LOSS) AVAILABLE TO

COMMON SHAREHOLDERS $ (104) $ 1,536 $ 934 $ 2,087

======== ========= ======== =========

INCOME (LOSS) PER COMMON SHARE:

Basic $ (0.03) $ .45 $ .27 $ .61

======== ========= ======== =========

Diluted $ (0.03) $ .45 $ .27 $ .61

======== ========= ======== =========

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

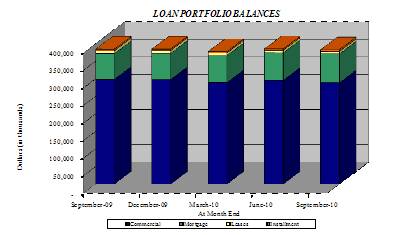

LOAN PORTFOLIO AND CREDIT QUALITY

(Dollars in thousands)

Loan Portfolio Balances (at end of period):

September 30, December 31, September 30,

2010 2009 2009

------------ ------------ ------------

Commercial Loans

Real estate - operators of

nonresidential buildings $ 52,192 $ 48,689 $ 47,007

Hospitality and tourism 39,998 45,315 45,867

Commercial construction 25,718 24,591 24,076

Real estate agents and managers 19,675 24,242 23,996

Other 157,679 162,833 165,644

------------ ------------ ------------

Total Commercial Loans 295,262 305,670 306,590

1-4 family residential real estate

and construction 82,312 74,350 73,116

Consumer 5,153 4,290 4,394

------------ ------------ ------------

Total Loans $ 382,727 $ 384,310 $ 384,100

============ ============ ============

Credit Quality (at end of period):

September 30, December 31, September 30,

2010 2009 2009

----------- ----------- -----------

Nonperforming Assets :

Nonaccrual loans $ 4,447 $ 14,368 $ 10,655

Loans past due 90 days or more - - -

Restructured loans 6,800 869 873

----------- ----------- -----------

Total nonperforming loans 11,247 15,237 11,528

Other real estate owned 5,758 5,804 5,821

----------- ----------- -----------

Total nonperforming assets $ 17,005 $ 21,041 $ 17,349

=========== =========== ===========

Nonperforming loans as a % of loans 2.94% 3.96% 3.00%

----------- ----------- -----------

Nonperforming assets as a % of

assets 3.41% 4.08% 3.38%

----------- ----------- -----------

Reserve for Loan Losses:

At period end $ 5,437 $ 5,225 $ 4,081

----------- ----------- -----------

As a % of average loans 1.42% 1.39% 1.10%

----------- ----------- -----------

As a % of nonperforming loans 48.34% 34.29% 35.40%

----------- ----------- -----------

As a % of nonaccrual loans 122.26% 36.37% 38.30%

=========== =========== ===========

Charge-off Information (year to

date):

Average loans $ 384,028 $ 374,796 $ 370,952

----------- ----------- -----------

Net charge-offs $ 4,488 $ 2,752 $ 1,596

----------- ----------- -----------

Charge-offs as a % of average

loans 1.17% .73% .43%

----------- ----------- -----------

MACKINAC FINANCIAL CORPORATION AND SUBSIDIARIES

QUARTERLY FINANCIAL HIGHLIGHTS

QUARTER ENDED

----------------------------------------------------------

(Unaudited)

----------------------------------------------------------

September December September

30, June 30, March 31, 31, 30,

2010 2010 2010 2009 2009

--------- --------- ---------- --------- ----------

BALANCE SHEET

(Dollars in

thousands)

Total loans $ 382,727 $ 384,839 $ 377,311 $ 384,310 $ 384,100

Allowance for

loan losses (5,437) (6,371) (4,737) (5,225) (4,081)

--------- --------- ---------- --------- ----------

Total loans,

net 377,290 378,468 372,574 379,085 380,019

Intangible

assets - - - - -

Total assets 499,006 500,774 502,427 515,377 513,180

Core deposits 287,055 271,026 236,227 209,828 200,541

Noncore

deposits (1) 117,469 134,758 168,985 211,561 218,040

--------- --------- ---------- --------- ----------

Total

deposits 404,524 405,784 405,212 421,389 418,581

Total borrowings 36,069 36,140 36,140 36,140 36,140

Total

shareholders'

equity 55,987 56,231 58,722 55,299 55,766

Total shares

outstanding 3,419,736 3,419,736 3,419,736 3,419,736 3,419,736

AVERAGE BALANCES

(Dollars in thousands)

Assets $ 512,335 $ 502,942 $ 508,495 $ 514,102 $ 513,687

Loans 385,268 382,169 384,640 386,203 370,310

Deposits 416,847 405,449 413,897 418,280 419,102

Equity 56,668 57,889 55,109 55,665 54,594

INCOME STATEMENT

(Dollars in

thousands)

Net interest

income $ 4,064 $ 4,023 $ 4,022 $ 4,431 $ 4,310

Provision for

loan losses 1,000 2,800 900 2,300 700

--------- --------- ---------- --------- ----------

Net interest

income after

provision 3,064 1,223 3,122 2,131 3,610

Total noninterest

income 648 593 807 1,503 2,418

Total noninterest

expense 3,601 5,330 3,629 3,650 3,443

--------- --------- ---------- --------- ----------

Income (Loss)

before taxes 111 (3,514) 300 (16) 2,585

Provision for

(benefit of)

income taxes 30 (1,212) (3,411) (22) 864

Preferred

dividend

expense 185 186 185 186 185

--------- --------- ---------- --------- ----------

Net income (loss)

available to

common

shareholders $ (104) $ (2,488) $ 3,526 $ (180) $ 1,536

========= ========= ========== ========= ==========

PER SHARE DATA

Earnings

(Losses) -

basic $ (.03) $ (.73) $ 1.03 $ (.05) $ .45

Earnings

(Losses)-

diluted (.03) (.73) 1.03 (.05) .45

Book value per

common share 13.26 13.34 14.08 13.10 13.25

Market value,

closing price 5.10 6.50 4.72 4.64 4.10

ASSET QUALITY RATIOS

Nonperforming

loans/total

loans 2.94% 2.87% 2.62% 3.96% 3.00%

Nonperforming

assets/total

assets 3.41 3.34 3.51 4.08 3.38

Allowance for

loan

losses/total

loans 1.42 1.66 1.26 1.36 1.06

Allowance for

loan losses/

nonperforming

loans 48.34 57.69 47.87 34.29 35.40

Texas Ratio(2) 27.68 26.71 27.76 34.77 28.99

PROFITABILITY RATIOS

Return on

average assets (.08)% (1.98)% 2.81% (.14)% 1.19%

Return on

average equity (0.73) (17.24) 25.95 (1.28) 11.16

Net interest

margin 3.69 3.56 3.51 3.74 3.66

Efficiency ratio 75.98 76.04 78.12 71.03 70.09

Average

loans/average

deposits 92.42 94.26 92.93 92.33 88.36

CAPITAL ADEQUACY

RATIOS

Tier 1 leverage

ratio 9.22% 9.38% 9.85% 9.75% 9.74%

Tier 1 capital

to risk weighted

assets 11.73 11.65 12.48 11.92 12.18

Total capital

to risk weighted

assets 12.98 12.91 13.69 13.17 13.19

Average equity/

average assets 11.06 11.51 10.84 10.83 10.63

Tangible equity/

tangible assets 11.06 11.51 10.84 10.83 10.87

(1) Noncore deposits includes Internet CDs, brokered deposits and

CDs greater than $100,000

(2) Texas Ratio: Nonperforming Assets divided by Total Equity plus

Allowance for Loan Losses

Contact Information: Contact: Investor Relations (888) 343-8147 Website: www.bankmbank.com