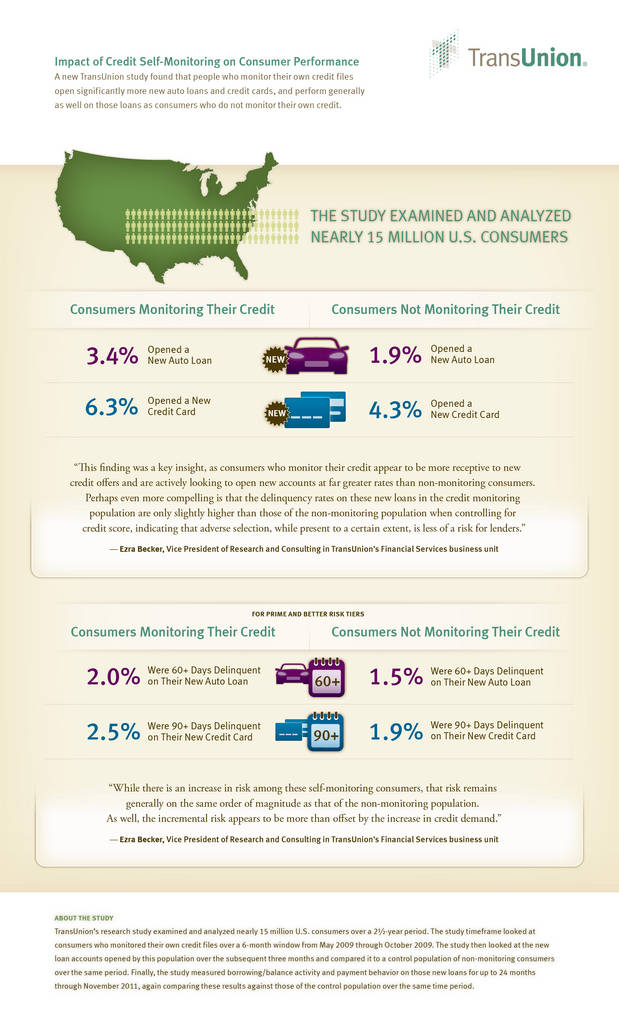

CHICAGO, IL--(Marketwire - Oct 17, 2012) - A new TransUnion study has found that people who monitor their own credit files open significantly more new auto loans and credit cards, and perform generally as well on those loans as consumers who do not monitor their own credit.

The study found that consumers who monitor their credit in any given credit score range not only open far more new accounts than those who do not, but it may indicate that these consumers recognized the importance of a healthy credit profile; and are actively looking for ways to improve it prior to making new purchases.

"Our study started with the conjecture that individuals who monitor their credit health might be motivated the same way as people who monitor their physical health," said Ezra Becker, vice president of research and consulting in TransUnion's financial services business unit. "We assume the latter generally fall into two categories: healthier people who want to stay that way, and less healthy consumers who want to become fit. We have found that consumers who monitor their credit tend to fall into two similar groups: credit-healthy consumers who wish to maintain that health and/or guard against identity theft; and riskier consumers that are looking to take proactive measures to better manage their credit profiles in anticipation of acquiring additional credit."

TransUnion's "Impact of Credit Self-Monitoring on Consumer Performance" study revealed that nearly 3.4% of consumers who monitored their credit during the study timeframe opened a new auto loan, while only 1.9% of consumers who did not monitor their credit opened an auto loan. This held true for other credit instruments such as general purpose credit cards, where nearly 6.3% of consumers monitoring their credit opened new credit cards; only 4.3% of consumers not monitoring their credit opened new credit card accounts in the same period.

"This finding was a key insight, as consumers who monitor their credit appear to be more receptive to new credit offers and are actively looking to open new accounts at far greater rates than non-monitoring consumers," said Becker. "Perhaps even more compelling is that the delinquency rates on these new loans in the credit monitoring population are only slightly higher than those of the non-monitoring population when controlling for credit score, indicating that adverse selection, while present to a certain extent, is less of a risk for lenders."

The study looked at the VantageScore® credit score distribution of the credit monitoring population versus that of the non-monitoring population. The credit score distribution of the monitoring consumer group was riskier than the non-monitoring group: 50.4% of the monitoring consumer population had non-prime credit scores (VantageScore credit score less than 700), compared to 40.1% of the non-monitoring population. "The difference in score distribution tends to support the theory that many self-monitoring consumers are doing so because they wish to improve their credit profiles," said Becker. "It is also why we have to control for credit score in studies such as this."

In the prime and better risk tiers, the 60-day or worse delinquency rate on new auto loans opened by the credit self-monitoring population was 2.0%, compared to 1.5% for the non-monitoring population. Similarly, the 90-day or worse delinquency rate on new credit cards opened by the credit self-monitoring population was 2.5%, compared to 1.9% for the non-monitoring population. "While there is an increase in risk among these self-monitoring consumers, that risk remains generally on the same order of magnitude as that of the non-monitoring population. As well, the incremental risk appears to be more than offset by the increase in credit demand," said Becker. "This is valuable insight for lenders who may be interested in marketing to consumers whom they may not have valued as prospective customers otherwise."

About the study

TransUnion's research study examined and analyzed nearly 15 million U.S. consumers over a 2 1/2-year period. The study timeframe looked at consumers who monitored their own credit files over a 6-month window from May 2009 through October 2009. The study then looked at the new loan accounts opened by this population over the subsequent three months and compared it to a control population of non-monitoring consumers over the same period. Finally, the study measured borrowing/balance activity and payment behavior on those new loans for up to 24 months through November 2011, again comparing these results against those of the control population over the same time period.

About TransUnion

As a global leader in credit and information management, TransUnion creates advantages for millions of people around the world by gathering, analyzing and delivering information. For businesses, TransUnion helps improve efficiency, manage risk, reduce costs and increase revenue by delivering comprehensive data and advanced analytics and decisioning. For consumers, TransUnion provides the tools, resources and education to help manage their credit health and achieve their financial goals. Through these and other efforts, TransUnion is working to build stronger economies worldwide. Founded in 1968 and headquartered in Chicago, TransUnion reaches businesses and consumers in 32 countries around the world on five continents. www.transunion.com/business

Contact Information:

Contact

Dave Blumberg

TransUnion

E-mail

Telephone 312 972 6646