PARIS and NEW YORK, April 22, 2015 (GLOBE NEWSWIRE) -- For the second year in a row, improvement in global retail bank customer experience levels has stalled with a decline of less than one percent leaving banks challenged to drive top-line growth, finds the twelfth annual World Retail Banking Report (WRBR) released today by Capgemini and Efma. Stagnating global customer experience levels combined with an alarming increase in customers willing to leave their banks, points to weakening bank-customer relationships and the increased possibility of disintermediation1 by non-bank competitors such as brand-name retailers, FinTech firms, crowd-funding websites, peer-to-peer lenders, Internet/mobile service providers, and Apple NFC-based payment systems. These findings underscore the need for retail banks to make investments to improve customer experience, especially with middle and back offices2, which have historically been ignored and are essential to providing engaging digital services through faster processing times and reduction in errors. The report draws on research insights from 32 markets and global data from over 16,000 retail banking customers as part of its annual Customer Experience Index.

A graphic accompanying this release is available at http://media.globenewswire.com/cache/29447/file/33452.pdf

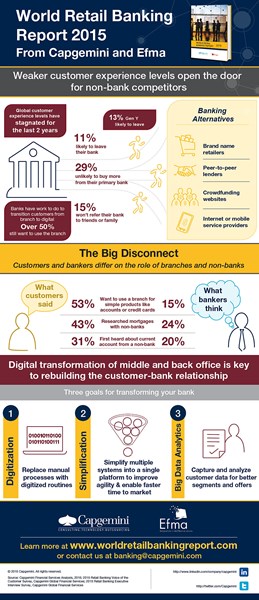

Troubling Changes in Customer Behaviors

In addition to lower customer experience levels, the WRBR found that globally customers' propensity to leave their primary bank3 (especially Gen Y4) is on the rise, while willingness to make referrals or buy additional products has decreased significantly. The percentage of customers who said they were likely to leave their primary bank in the next six months rose into double-digits in every region except Western Europe. According to the WRBR data, customers' likelihood to leave their banks increased anywhere from nearly 4 percentage points (pp) to over 12pp last year depending on region. Globally, less than 50 percent of Gen Y customers are likely to continue with their primary bank in the next six months. Reasons for customers leaving banks could be the increase in non-bank competition, growth of start-up banks which offer attractive digital products, and the ease in logistically switching banks.

Also concerning for banks was the expanding number of customers who said they were not likely to make referrals or purchase an additional product from their primary bank. Customers unlikely to make referrals rose over 9.5pp in some regions (10.5 pp in Asia-Pacific and 9.7 pp in Western Europe) and the unlikelihood to purchase a second product from their primary bank increased as much as 25pp in Western Europe.

Banks also appear to have stalled in their ability to steer customers away from the branch toward lower-cost channels. Despite significant leaps to high rates of usage for both the internet and mobile channels, the impact on branch usage was minimal. In fact, branch usage rose modestly in North America and Europe during 2014, while decreasing only slightly in Latin America and barely at all in Asia-Pacific.

Stage Is Set for Non-Bank Competitors to Gain a Foothold

All of these factors provide non-banks with the opportunity to attract customers away from their primary banks. Internet and technology firms, in particular, with their simple, agile, and intuitive offerings and freedom from legacy systems, are at the top of the list of competitors, with 83 percent of bank executives viewing customers as comfortable with banking through these entities. Already, such firms have carved out a significant presence in the area of payments and credit cards, particularly in North America and Western Europe.

Middle and Back Offices Need Attention

Bank executives have not hesitated to invest in the front office, with almost 93 percent citing customer experience as the main driver behind such investments. However, underfunding in the middle and back offices has undermined these front-office investments through slow processing times, errors, and exceptions that contribute greatly to reduced service in customer interactions.

"Disenchanted customers, combined with the agility and innovative nature of non-bank competitors, is leaving the door wide open for capturing market-share," said Jean Lassignardie, Chief Sales and Marketing Officer at Capgemini Global Financial Services. "Improving customer experience is the best strategy to deflect competition from non-bank players. While investments in improving front office customer experience have expanded banks' offerings, middle and back office transformation has been plagued by under-investment and will be the key to resolving disjointed customer experiences and improving longer term loyalty rates."

To overcome these challenges, banks need to develop a roadmap that outlines a gradual approach to digital transformation, encompassing digitization, simplification/agility and big data analytics. Digitization seeks to replace manual processes with digital routines. Simplification increases agility by reducing multiple systems in to fewer and enabling faster time to market. Big Data analytics puts in place the ability to capture, manage, and derive insights from customer data effectively. The plan for full digital maturity must place as high a priority on the middle and back offices, as the front office as the majority (60 percent) of customer dissatisfaction emanates from back office issues leading to an increase in overall negative customer experience levels5. "With a thoughtful, methodical plan for digital transformation," said Patrick Desmarès, Secretary General of Efma, "banks can begin to improve their customer experience scores and position themselves to compete against nimbler, non-traditional entrants."

The World Retail Banking Report

The World Retail Banking Report 2015 draws on research insights from 32 markets. Featuring its annual Customer Experience Index, the report presents the cumulative findings of its Voice of the Customer survey which includes global data from over 16,000 retail banking customers and executive interviews across six geographies. Eighty customer interaction touch points were analyzed to present an examination of the factors that are most important to banking customers, measured across the entire banking customer journey.

For more information visit www.worldretailbankingreport.com

About Capgemini

With almost 145,000 people in over 40 countries, Capgemini is one of the world's foremost providers of consulting, technology and outsourcing services. The Group reported 2014 global revenues of EUR 10.573 billion. Together with its clients, Capgemini creates and delivers business and technology solutions that fit their needs and drive the results they want. A deeply multicultural organization, Capgemini has developed its own way of working, the Collaborative Business Experience™, and draws on Rightshore®, its worldwide delivery model.

Capgemini's Global Financial Services Business Unit brings deep industry experience, innovative service offerings and next generation global delivery to serve the financial services industry. With a network of 24,000 professionals serving over 900 clients worldwide Capgemini collaborates with leading banks, insurers and capital market companies to deliver business and IT solutions and thought leadership which create tangible value.

Learn more about us at www.capgemini.com and www.capgemini.com/financialservices.

Rightshore® is a trademark belonging to Capgemini

About Efma

As a global not-for-profit organization, Efma brings together more than 3300 retail financial services companies from over 130 countries. With membership from almost a third of all large retail banks worldwide, Efma has proven to be a valuable resource for the global industry, offering members exclusive access to a multitude of resources, databases, studies, articles, news feeds and publications. Efma also provides numerous networking opportunities through work groups, online communities and international meetings.

Visit: www.efma.com

1 Disintermediation occurs when customers make transactions directly with non-banks and bypass traditional banks.

2 The banking customer journey value chain consists of front office, middle office and back office interactions. The front office represents the customer interface with the bank whether it be digitally or in-person at a branch. The middle and back offices consist of the inner workings of the bank to process transactions.

3 A primary bank is the bank with which a customer does the majority or most important banking transactions.

4 Generation Y consists of individuals born between 1980 and 2000 whom have always had digital connections as part of their adult lives.

5 "Backing up the Digital Front: Digitizing the Banking Back Office," Capgemini, 2013.

The photo is also available via AP PhotoExpress.