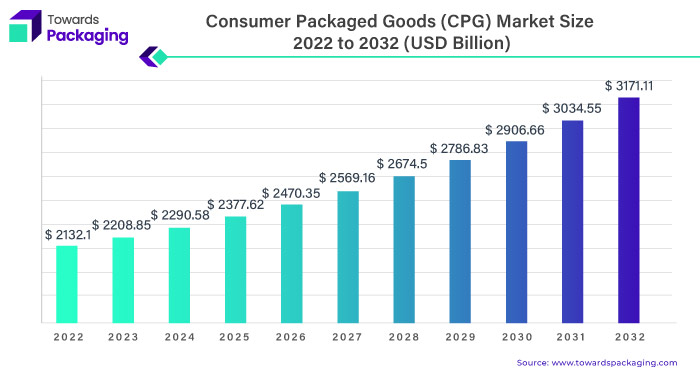

Ottawa, March 06, 2024 (GLOBE NEWSWIRE) -- The global consumer packaged goods (CPG) market size stood at USD 2,208.85 billion in 2023, grew to USD 2,290.58 billion in 2024, and is anticipated to reach around USD 2,786.83 billion by 2029, a study published by Towards Packaging a sister firm of Precedence Research.

Report Highlights: Important Revelations

- Interconnected markets driving consumer packaged goods companies to explore international opportunities.

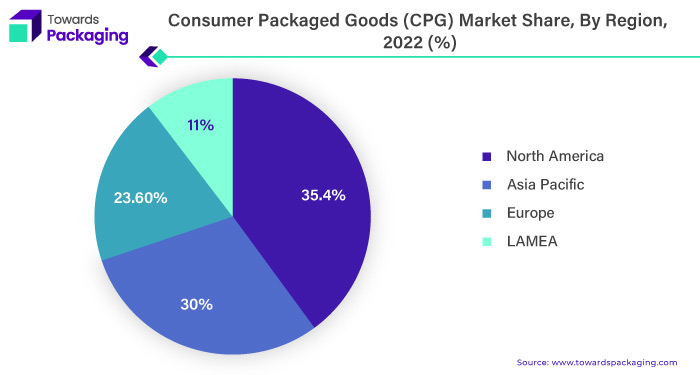

- North America's CPG industry commands a $2 trillion valuation.

- Asia Pacific’s consumer package goods set to expand rapidly by 2030.

- Food and beverage reigns supreme in consumer packaged goods sales.

- Consumer packaged goods companies prioritize large offline retailers in operations.

Consumer packaged goods are goods that the typical consumer consumes daily, such as food, beverages, and household supplies. and makeup.

Consumer packaged goods (CPG) play a pivotal role in the daily lives of individuals, encompassing a diverse range of products from food and beverages to apparel and cosmetics. These items are integral to households and necessitate consistent replenishment or replacement, fuelling an ongoing demand that fosters a fiercely competitive market for all brands. Underscores the robustness of the CPG sector, revealing an impressive 8% year-over-year growth and a projected annual sales figure of $1.62 trillion. This data signals a thriving market environment, prompting CPG firms to keenly observe shifting consumer patterns. A notable 40% of these firms actively respond to these changes by setting ambitious sustainability objectives.

For the short version of this report @ https://www.towardspackaging.com/personalized-scope/5098

In response to the imperative of sustainability, CPG companies are strategically incorporating comprehensive plans to align their operations with environmentally conscious practices. A prime example is the commitment to sustainable packaging for their product lines. By prioritizing eco-friendly materials and production processes, these firms aim to reduce their environmental footprint and contribute positively to global sustainability goals. Moreover, CPG companies are adopting holistic sustainability initiatives that extend beyond packaging. These initiatives encompass emission reduction strategies and other environmentally responsible objectives, collectively aimed at enhancing the overall eco-friendliness of their products. This strategic shift towards sustainability aligns with evolving consumer preferences and positions CPG firms as responsible contributors to a greener and more sustainable future.

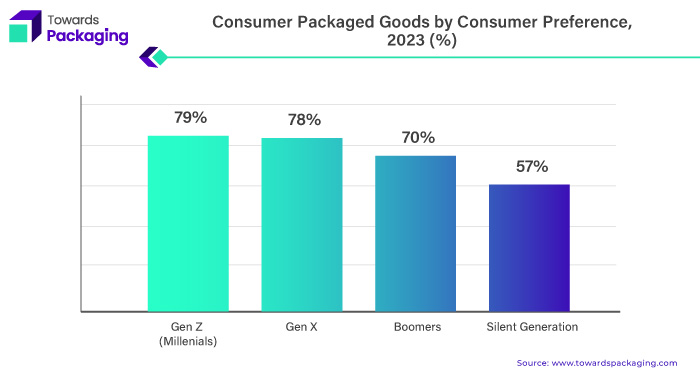

The preference for consumer packaged goods (CPG) varies across different generational cohorts, highlighting distinct consumer behaviours. Among Millennials (Gen Z), approximately 79% express preferences for CPG products, showcasing a significant affinity for these goods. Generation X closely follows, with 78% indicating a preference for CPG items. Boomers also exhibit a substantial inclination, with 70% expressing a preference for CPG. In contrast, the Silent Generation demonstrates a comparatively lower preference, with 57% indicating a favourable stance towards CPG products.

Interconnected Markets Driving Consumer Packaged Goods Companies to Explore International Opportunities

- CPG products, from food and beverages to personal care items, constitute essential and routine consumer purchases, driving consistent demand.

- The perishable nature of many CPG goods and the routine consumption patterns necessitates regular replenishment, ensuring a continuous market demand.

- The broad spectrum of CPG offerings, including food, clothing, cosmetics, and household items, caters to a wide range of consumer needs, expanding market reach.

- Shifting consumer preferences and evolving lifestyles influence the types of CPG products in demand, prompting innovation and adaptation by manufacturers.

- Technology integration in manufacturing, distribution, and marketing processes enhances efficiency, reduces costs, and improves overall supply chain management for CPG companies.

- The rise of online shopping platforms provides consumers convenient access to a wide array of CPG products, reshaping traditional retail dynamics and expanding market accessibility.

- Increasing health and wellness awareness influences consumer choices, driving demand for healthier food options, organic products, and environmentally friendly packaging within the CPG sector.

- As markets become increasingly interconnected, CPG companies are exploring global opportunities, leading to the expansion of their product distribution and market presence.

- Growing environmental consciousness among consumers propels CPG companies to adopt sustainable practices, including eco-friendly packaging, reducing emissions, and incorporating responsible sourcing.

If you have any questions, please feel free to contact us at sales@towardspackaging.com

Consumer Packaged Goods (CPG) Market Trends

| Trends | |

| Online Marketing and E-commerce Shift | The CPG industry is significantly transitioning towards online marketing and e-commerce platforms, reflecting changing consumer preferences for convenient and digital shopping experiences. |

| Embrace of Eco-friendly Practices | CPG companies increasingly adopt eco-friendly packaging, sustainable retail displays, and environmentally conscious business practices, responding to heightened consumer awareness and demand for products with reduced ecological impact. |

| Direct-to-Consumer Expansion | Traditional CPG firms are exploring new avenues with the rise of direct-to-consumer brands and purchasing options, recognizing the importance of establishing direct connections with consumers to enhance brand loyalty and adapt to evolving market dynamics. |

| Supply Chain Resilience | CPG companies prioritize developing more stable, diversified, and resilient supply chains, driven by the need to mitigate risks, ensure consistent product availability, and adapt to disruptions in the global market. |

North America's CPG Industry Commands a $2 Trillion Valuation

The consumer packaged goods (CPG) industry remains a cornerstone of North America's economic landscape, boasting an impressive valuation of around $2 trillion. Industry leaders, including renowned companies like Coca-Cola, Procter & Gamble, and L'Oréal, play pivotal roles in shaping this sector's trajectory. Despite healthy profit margins and robust financial standings, CPG manufacturers face perpetual challenges securing coveted shelf space within retail establishments. To maintain and expand market share, these companies consistently allocate substantial resources to advertising, aiming to enhance brand recognition and drive sales.

The CPG landscape has witnessed a notable trend of increased marketing expenditures across diverse sectors, sizes, and price tiers in the United States. According to a survey conducted among U.S. marketing professionals, 23 per cent of CPG companies' budgets were dedicated to marketing initiatives in early 2023. This proportion marked the highest share of advertising expenditures observed among various industries in the country during that period.

For Instance,

- In August 2023, A product produced with Crisp, an open data system for the consumer goods sector, North America's United Natural Foods, Inc. unveiled UNFI Insights.

While established market leaders like PepsiCo and L'Oréal continue their annual investments of billions of dollars in expansive marketing campaigns, they find themselves at the forefront of adapting to significant shifts in consumer behaviour. Consumers evolving preferences and behaviours necessitate a strategic realignment of marketing approaches, prompting these industry giants to navigate and capitalize on the changing dynamics to maintain their competitive edge in the ever-dynamic CPG landscape.

For Instance,

- In September 2023, the new Instacart for Shopify app allows rising consumer packaged goods (CPG) firms on Shopify to use Instacart Ads. Instacart is the leading grocery technology company in North America.

Asia's rapidly expanding consuming class is a noteworthy trend poised to reshape the region's economic landscape. By 2030, it is projected that an astounding three billion individuals, constituting 70% of Asia's total population, will join the consuming class. This surge represents a billion more individuals than the present and a substantial increase of 2.5 billion from the turn of the millennium. Such a demographic shift is anticipated to significantly enlarge the consuming class in various economies.

Projections indicate a substantial increase in the consumption class in specific countries. By 2030, Indonesia may see up to 200 million individuals becoming part of the consuming class, a noteworthy increase from the current 120 million. Similarly, India could witness an expansion to as high as 825 million individuals in the consuming class by 2030, up from approximately 340 million.

Notably, the growth in the consuming class is not only about an influx of new members but also about internal mobility within the class itself. The upward income movement within the consuming class will drive consumption growth over the next decade. This upward shift in revenue is set to alter the centre of gravity in the income pyramid, influencing consumption habits.

Over the last two decades, a substantial 80% of Asia's consumption growth has been attributed to the lower-income segments of the consuming class as new members entered. It is anticipated that higher-income consumers will take the lead, contributing up to 80% of future consumption growth in the next decade. This shift in the composition of the consuming class and their income levels presents a significant opportunity for consumer packaged goods (CPG) companies to cater to an expanding and evolving consumer base in the dynamic Asian market.

Customize this study as per your requirement @ https://www.towardspackaging.com/customization/5098

For Instance,

- In September 2023, India's Tata Consumer Products (TCPL), a packaged goods company, "limited its universe" for its subsequent product launches by focusing on five main areas. These categories, which include coffee, tea, and salt, reflect its current main products.

Food and Beverage Reigns Supreme in Consumer Packaged Goods Sales

The food and beverage sector has emerged as the predominant online consumer packaged goods (CPG) segment for the year, representing 44% of total sales. While the pandemic significantly boosted online sales, other market dynamics, such as adherence to hygiene standards and a growing consumer preference for personalized experiences, are expected to sustain the momentum of online shopping in this category. Projections indicate that the food and beverage segment is poised to generate a substantial $26,774 million in revenue.

In recent years, consumer packaged goods and food and beverage industries have faced persistent challenges, with ongoing disruptions extending beyond the initial impact of the global pandemic. Raw material shortages originating from Ukraine and Russia, along with delays in production and processing and surging oil and gas costs, have directly affected various aspects of food-related manufacturing, transportation, and agricultural supply chains. These challenges are not confined to a specific region, as CPG manufacturing, food distribution, and retail operations grapple with issues on a global scale.

In December 2022,

- The FMCG division of Reliance Retail, Reliance Consumer Products, announced the debut of it made-in-India consumer packaged goods brand, Independence.

Specifically, the availability of raw ingredients critical to the production of staple products such as cereal, flour, bread, beer, and other commodities has been constrained in the United States. Furthermore, disruptions in the shipping and container industries have led to delayed shipments and increased costs, exacerbating concerns about inflation. The cumulative impact of these factors underscores the intricate challenges faced by the food and beverage sector within the larger CPG landscape, necessitating strategic adaptation to navigate the complexities of the current market environment.

Consumer Packaged Goods Companies Prioritize Large Offline Retailers in Operations

The forefront of the consumer packaged goods (CPG) market, demonstrating substantial dominance in both offline and online dimensions. This sector is impressive in offline transactions, amounting to $297, emphasizing the enduring significance of traditional brick-and-mortar retail channels. The offline basket size signifies the average amount spent on food and beverage products in physical stores, highlighting the substantial revenue generated through these conventional retail outlets.

Browse More Insights of Towards Packaging:

- The global green packaging market size is estimated to grow from USD 303.83 billion in 2022 to reach an estimated USD 510.93 billion by 2032, at 5.3% CAGR from 2023 to 2032.

- The global pet food packaging market size is estimated to grow from USD 11.38 billion in 2022 to set a foot on USD 22.08 billion by 2032, at 6.9% CAGR from 2023 to 2032.

- The global corrugated packaging market size is expected to grow from USD 276 billion in 2022 and it is predicted to hit around USD 410.50 billion by 2032, at 4.10% CAGR from 2023 to 2032.

- The global cosmetic packaging market size accounted for USD 33.07 billion in 2022 to reach USD 54.13 billion by 2032 at 4.5% CAGR from 2023 to 2032.

- The global edible packaging market size current valuation, standing at USD 1.4 billion in 2022 projected to culminate zenith of USD 5.26 billion by 2032 at 14.2% CAGR between 2023 and 2032.

In contrast, the online basket size for the food and beverage sector is $64, indicating the average expenditure on these products in the digital realm. Although the online dimension is a growing aspect of the market, it is noteworthy that the offline component retains its substantial share, underscoring the continued importance of physical retail channels for CPG companies.

For Instance,

- In September 2023, the pioneer of next-generation product visualization technology for retailers and brands, Nfinite, unveiled new research findings from Dimensional Research today and increased CPG offerings.

| 2023 Top 10 Consumer Goods Companies | ||||

| 2023 Rank | Company | 2022 Net Revenue | One Year Sales Growth | |

| 1 | Nestlé SA | $99.32 Billion | 3.78 | % |

| 2 | PepsiCo | $86.392 Billion | 8.70 | % |

| 3 | LVMH Moët Hennessey Louis Vuitton* | $84.677 Billion | 23.28 | % |

| 4 | Procter & Gamble | $80.187 Billion | 5.35 | % |

| 5 | JBS S.A. | $72.609 Billion | 11.73 | % |

| 6 | Unilever N.V. | $63.293 Billion | 2.01 | % |

| 7 | Anheuser-Busch InBev | $55.786 Billion | 6.41 | % |

| 8 | Tyson Foods | $53.282 Billion | 13.25 | % |

| 9 | Nike, Inc. | $46.71 Billion | 4.88 | % |

| 10 | Coca-Cola Co. | $43.005 Billion | 11.25 | % |

CPG companies strategically prioritize large brick-and-mortar retailers as a focal point of their operations, recognizing that these outlets constitute most of their business. The emphasis on brick-and-mortar retail is particularly relevant for high-volume perishable items within the food and beverage sector. These products, widely available at retailers globally, are frequently purchased for immediate consumption, with consumers instinctively replenishing their preferred frozen meals. The chronic nature of these purchases, often made with minimal deliberation, contributes to the enduring strength of brick-and-mortar retail for CPG companies operating in the food and beverage sector.

Competitive Landscape

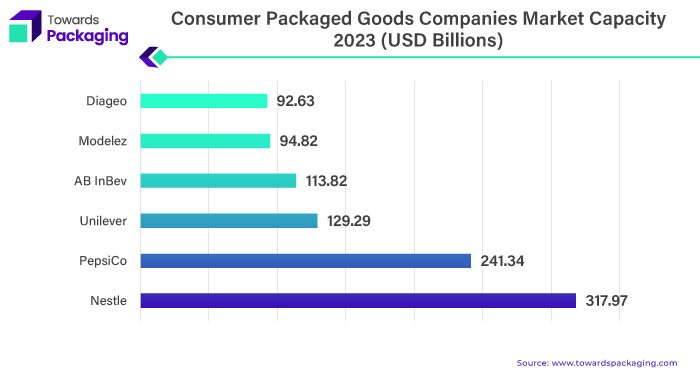

The competitive landscape of the consumer packaged goods (CPG) market is characterized by established industry leaders such as PepsiCo, Unilever, Nestle, General Mills, Danone, Mondelez, JBS, AB InBev, Kraft Heinz and Diageo. These giants face competition from emerging direct-to-consumer brands, leveraging digital platforms for market entry. Key factors influencing competition include innovation in product offerings, sustainable practices, and the ability to adapt to changing consumer preferences. Additionally, the sector sees dynamic collaborations, acquisitions, and strategic partnerships as companies strive to capture market share in this highly competitive and evolving industry.

Consumer Packaged Goods (CPG) Market Key Players

- PepsiCo

- Unilever

- Nestle

- General Mills

- Danone

- Mondelez

- JBS

- AB InBev

- Kraft Heinz and Diageo

Recent Developments

- In December 2023, Chobani, a consumer goods company, acquired the ready-to-drink coffee manufacturer La Colombe to its portfolio. The $900 million acquisition was completed in December.

- In November 2023, Mars acquired the UK Chocolate Brand Hotel Chocolate. The acquisition will boost Hotel Chocolates' growth prospects in the United Kingdom and new global markets.

- In November 2023, General Mills acquired Veterinarians and established Fera Pets, a line of pet supplements. This new product will be the first supplement in General Mills' pet portfolio and the first purchase made by the company's recently established growth equity fund.

- In August 2023, Naturium was purchased by e.l.f. Beauty, Cosmetic brand leader, for $355 million in shares and cash.

Market Segments

By Application

- Food and Beverage

- Household Supplies

- Personal Care and Cosmetics

- Others

By Distribution Channel

- Online

- Offline

By Region

- North America

- Europe

- Asia Pacific

- LAMEA

Explore the statistics and insights concerning the packaging industry and its segmentation: Get a Subscription

If you have any questions, please feel free to contact us at sales@towardspackaging.com

About Us

Towards Packaging is a leading global consulting firm specializing in providing comprehensive and strategic research solutions. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations. We stay abreast of the latest industry trends and emerging markets to provide our clients with an unrivalled understanding of their respective sectors. We adhere to rigorous research methodologies, combining primary and secondary research to ensure accuracy and reliability. Our data-driven approach and advanced analytics enable us to unearth actionable insights and make informed recommendations. We are committed to delivering excellence in all our endeavours. Our dedication to quality and continuous improvement has earned us the trust and loyalty of clients worldwide.

Browse our Brand-New Journal@ https://www.towardshealthcare.com/

Browse our Consulting Website@ https://www.precedenceresearch.com/

For Latest Update Follow Us: https://www.linkedin.com/company/towards-packaging/