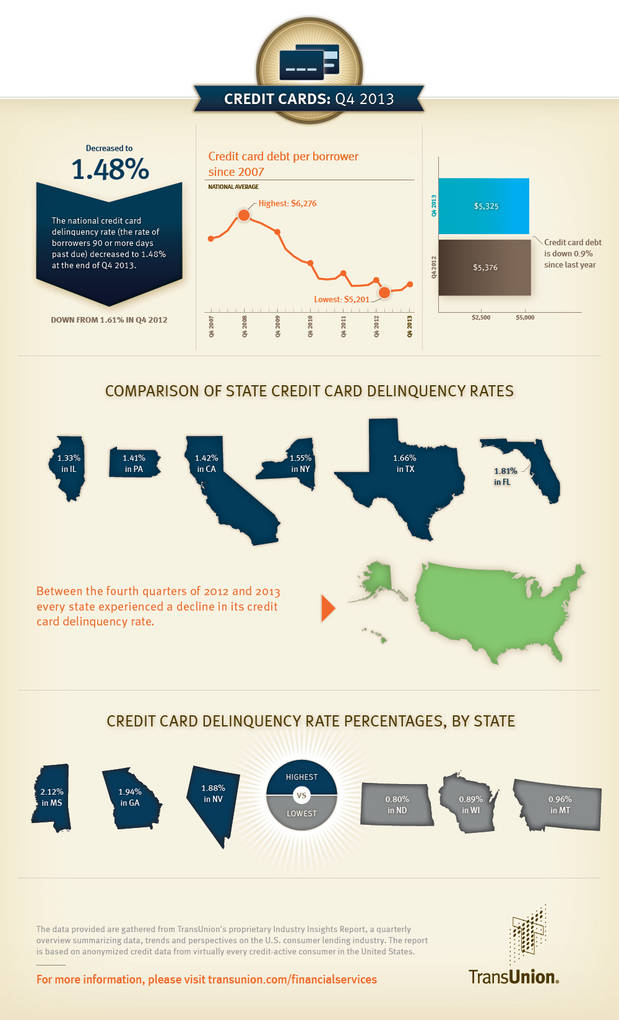

CHICAGO, IL--(Marketwired - Feb 18, 2014) - The credit card delinquency rate (the ratio of borrowers 90 days or more delinquent on their general purpose credit cards) dropped on a yearly basis from 1.61% in Q4 2012 to 1.48% in Q4 2013. In a sign that consumers continue to deleverage, average credit card debt per borrower also declined from $5,376 in Q4 2012 to $5,325 in Q4 2013.

On a quarterly basis, both the credit card delinquency rate (up from 1.36% in Q3 2013) and credit card debt (up from $5,235 in Q3 2013) increased due to seasonality associated with holiday shopping.

The data provided are gathered from TransUnion's proprietary Industry Insights Report, a quarterly overview summarizing data, trends and perspectives on the U.S. consumer lending industry. The report is based on anonymized credit data from virtually every credit-active consumer in the United States.

"Credit card delinquencies continue to remain much lower than historical norms. We also believe that there is a continuing reduced demand for new credit in the prime credit ranges," said Ezra Becker, vice president of research and consulting in TransUnion's financial services business unit. "While industry reports show that direct mail has increased by about 30% in the last year, we have seen originations only rise about 11% in that same timeframe. In short, consumers are managing the cards they have in their wallets effectively and do not seem to be seeking additional card credit at this point. This also speaks to the need for lenders to examine alternative channels for account acquisition beyond traditional direct mail campaigns."

United States |

Q4 2013 |

Q4 Average (2007-2013) |

Credit Card Delinquency Rate |

1.48% |

2.25% |

Credit Card Debt Per Borrower |

$5,325 |

$5,721 |

Every state experienced a decline in their credit card delinquency rate between Q4 2012 and Q4 2013. The largest delinquency declines occurred in Massachusetts, Rhode Island, Wisconsin and Oregon. Credit card debt per borrower increased in only seven states on a yearly basis.

TransUnion reported 341.40 million credit card accounts as of Q4 2013, up from 329.48 million in Q4 2012. Viewed one quarter in arrears (to ensure all accounts are included in the data), new account originations increased to 11.96 million in Q3 2013, up from 10.75 million in Q3 2012.

TransUnion's latest credit card report also found that the non-prime population (those consumers with a VantageScore® 2.0 credit score lower than 700) continues to represent a smaller portion of all credit card loans at 30.13% in Q3 2013, down from 30.23% in the same period last year. In Q3 2007, the non-prime population represented 44.03% of all credit card loans. "With relatively fewer subprime credit cards in the marketplace, delinquencies should remain low," said Becker.

"At first glance, the increased number of credit card accounts and new account originations appear to be quite positive. However, there are still at least 40 million fewer credit card accounts active in the marketplace than what we observed just five years ago," said Becker. "While there are more than one million more new account originations from one year ago, the non-prime percentage of this group has actually declined. Competition in the prime score ranges is fierce, and those consumers don't seem to need more card credit. With the economy improving and delinquency rates remaining so low, we may see lenders shifting their acquisition activities to somewhat higher-risk market segments."

TransUnion is forecasting consumer delinquencies to rise to approximately 1.57% by the end of the first quarter, which remains a relatively low level. TransUnion's forecast is based on various economic assumptions, such as gross state product, consumer sentiment, unemployment rates, real personal income, and others. The forecast would change if there were unanticipated shocks to the economy.

This information is reported by TransUnion and is part of its ongoing series of quarterly analyses of credit-active U.S. consumers and how they are managing credit related to mortgages, credit cards and auto loans. To subscribe to TransUnion news releases, please click here.

Q4 2013 Credit Card Statistics - Consumer-Level Delinquency Rates

| Quarter over Quarter | Q3 2013 | Q4 2013 | Pct. Change |

| USA | 1.36% | 1.48% | 8.8% |

| Year over year | Q4 2012 | Q4 2013 | Pct. Change |

| USA | 1.61% | 1.48% | (8.1%) |

| Credit Card Consumer Delinquency Rates for Select States | Q4 2013 |

| California | 1.42% |

| Florida | 1.81% |

| Illinois | 1.33% |

| New York | 1.55% |

| Texas | 1.66% |

| Largest Year-over-Year Declines | Q4 2012 | Q4 2013 | Pct. Change |

| Massachusetts | 1.63% | 1.34% | (17.8%) |

| Rhode Island | 1.77% | 1.55% | (12.4%) |

| Wisconsin | 1.01% | 0.89% | (11.9%) |

| Smallest Year-over-Year Declines | Q4 2012 | Q4 2013 | Pct. Change |

| North Dakota | 0.82% | 0.80% | (2.4%) |

| Alaska | 1.19% | 1.16% | (2.5%) |

| Arkansas | 1.87% | 1.82% | (2.7%) |

Q4 2013 Credit Card Statistics - Credit Card Debt Per Borrower

| Quarter over Quarter | Q3 2013 | Q4 2013 | Pct. Change |

| USA | $5,235 | $5,325 | 1.7% |

| Year over year | Q4 2012 | Q4 2013 | Pct. Change |

| USA | $5,376 | $5,325 | (0.9%) |

| Credit Card Debt per Borrower for Select States | Q4 2013 |

| California | $5,410 |

| Florida | $5,349 |

| Illinois | $5,389 |

| New York | $5,496 |

| Texas | $5,551 |

| Largest Year-over-Year Declines | Q4 2012 | Q4 2013 | Pct. Change |

| Arizona | $5,511 | $5,374 | (2.5%) |

| California | $5,531 | $5,410 | (2.2%) |

| Colorado | $5,865 | $5,747 | (2.0%) |

| Largest Year-over-Year Increases | Q4 2012 | Q4 2013 | Pct. Change |

| West Virginia | $4,681 | $4,708 | 0.6% |

| Vermont | $4,982 | $5,006 | 0.5% |

| Rhode Island | $5,355 | $5,377 | 0.4% |

About TransUnion

As a global leader in credit and information management, TransUnion creates advantages for millions of people around the world by gathering, analyzing and delivering information. For businesses, TransUnion helps improve efficiency, manage risk, reduce costs and increase revenue by delivering comprehensive data and advanced analytics and decisioning. For consumers, TransUnion provides the tools, resources and education to help manage their credit health and achieve their financial goals. Through these and other efforts, TransUnion is working to build stronger economies worldwide. Founded in 1968 and headquartered in Chicago, TransUnion reaches businesses and consumers in 33 countries around the world on five continents. www.transunion.com/business

Contact Information:

Contact:

Dave Blumberg

TransUnion

E-mail:

Telephone: (312) 972 6646