Dublin, March 08, 2024 (GLOBE NEWSWIRE) -- The "India Residential Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2019 - 2029" report has been added to ResearchAndMarkets.com's offering.

The India Residential Construction Market size is estimated at USD 189.80 billion in 2024, and is expected to reach USD 272.67 billion by 2029, growing at a CAGR of 7.51% during the forecast period 2024-2029.

The cost of raw materials in India was on the rise, and since the COVID-19 pandemic, the cost kept increasing. A reason behind this increase in the cost of raw materials is the shortage of supply of raw materials because of the disruptive supply chain. Along with these, there has also been the introduction of several taxes by the state governments on these materials that are also contributing to the increasing costs. The scarcity of building materials raises the cost of overall construction, which is projected to hamper the growth of the Indian residential construction market.

The government's flagship initiative, the Pradhan Mantri Awas Yojana (Urban), which was launched in June 2015, aimed to provide housing for all in urban areas. To make the market more accessible to small and retail investors, the Securities and Exchange Board of India has reduced the minimum application value for Real Estate Investment Trusts (REITs) from INR 50,000 (USD 611.14) to INR 10,000-15,000 (USD 122.23-183.34). As a result, home sales volume in seven major Indian cities accelerated by 113% year-on-year in the third quarter of 2021. Private equity investment inflows into India's real estate sector totaled USD 3.3 billion in the first half of FY21-22. The top three cities, Mumbai (39%), Delhi (19%), and Bengaluru (19%), together attracted nearly 77% of the total investments.

Under the Pradhan Mantri Awas Yojana, the Indian government sanctioned the construction of 3.61 lakh homes in November 2021. In addition, with the clearance of the new housing units, 1.14 crore homes have been approved for the program. It is anticipated that the Indian Government's affordable housing program will continue to support the growth of the residential construction sector from a short- to medium-term perspective, which will subsequently aid the growth of India's residential construction industry. The central government is anticipated to approve more housing units under the PMAY scheme over the next four to eight quarters.

Need for Affordable Housing is Driving the Market

Indian governments, since independence have focused on the issue of affordable housing in the context of poverty reduction. In 2015, the government announced a housing program that aimed at providing a safe home to every Indian. Furthermore, the introduction of Real Estate Regulation Authorities in 2017 is meant to increase transparency in the market and strengthen the rights of buyers. As of May 2022, there were over one million housing units completed across the north Indian state of Uttar Pradesh within the Housing for All (HFA) program since 2014. In the financial year 2022, the government of India allocated 200 billion Indian rupees (USD 2.44 billion) for Pradhan Mantri Awaas Yojana-Gramin.

The national 2021 Budget, including INR 50,000 crore (USD 6111.43 billion) allocated to the Ministry of Housing and Urban Development (MoHUA) and the creation of a 3.5 billion USD fund to support the completion of stalled housing projects, there is strong government support for the housing sector at the national level. In India, where urbanization is predicted to increase from 33% to over 40% of the population by 2030, there will be a need for 25 million extra mid-range and inexpensive housing units, according to Invest India. In 2022, the total number of completed houses in urban areas of India under the Pradhan Mantri Awas Yojana (PMAY, The Prime Minister's Housing Plan) reached 5.4 million. The demand for housing facilities for the urban poor lies at around 11 million housing complexes in 2020.

Moreover, the industry has benefited from the push for policy that has resulted in legislation like the Real Estate Regulatory Authority (RERA), the introduction of Real Estate Investment Trusts (REITs), and SWAMIH (Special Window for Completion of Construction of Affordable and Mid-Income Housing Projects). It is anticipated that increased spending on residential projects by the state and central governments will continue to boost industry growth over the forecast period in the nation.

Increasing Investments in Residential Property Drives the Market

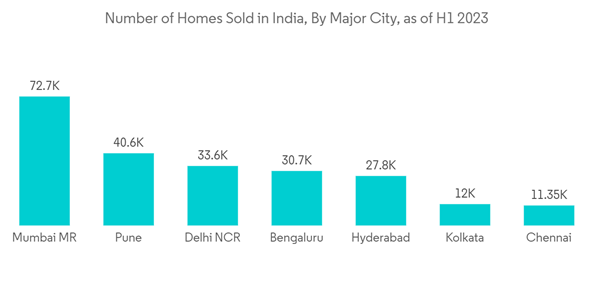

India has seen tremendous urban progress. It is estimated that by 2030, more than 400 million people will be living in cities in India. The demand for residential properties has been fuelled by India's expanding urban population, rising household incomes, and decade-long low loan rates, which have increased sales volume. In the first half of 2022, around 44 thousand housing units were sold in Mumbai, India's most demanding residential housing market. There was a total of 158,705 residential properties sold during the period.

In 2021, over 232 thousand housing units were launched on the residential market across India. Even though there is a big demand for housing in the country, residential launches have been on a comparatively high level over the past few years. Moreover, in 2021, Hyderabad recorded an increase in housing launches in the residential market of India by 179 percent. The national capital region of Delhi recorded 110 percent more launches than in 2020.

Mumbai Metropolitan Region recorded the highest residential property launches in Q1 2022. The city alone accounted for 92 percent quarter-on-quarter and 126 percent year-on-year change and launched more than 28,000 new housing units in Q1 2022 as against 12,000 in Q1 2021. In the first quarter of 2022, East Pune saw the maximum number of new residential units and accounted for 28 percent of the total new project launches. The financial and technology hub of India, Gurugram, launched about 3,800+ new residential units in Q1, 2022 (witnessing quarterly growth of 35 percent). The city consists of five major zones, including Golf Course Road, New Gurgaon, Central Gurgaon, Southern Peripheral Road, and Dwarka Expressway.

Hyderabad is one of the top contributors, accounting for an 83 percent year-on-year increase in the number of new launches in the recent quarter. Of all zones in the city, West Hyderabad furnished the maximum number of houses, which accounted for 52 percent of the total launches in the city. This was followed by North Hyderabad, which comprised about one-third of the total new projects launched in the city during Q1 2022. East Bengaluru witnessed the highest number of new residential property launches with 52 percent share, followed by North Bengaluru.

India Residential Construction Industry Overview

The Indian residential construction market has become increasingly competitive and fragmented, with a large number of local and regional players and a few global players. Some of the major players in India include Delhi Land & Finance, Merlin Group, StepsStone Builders, Godrej Properties Limited, Prestige Group, and many others. Key players are expanding their projects to meet the increasing demand from end users.

Key Topics Covered:

1 INTRODUCTION

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Current Market Scenario

4.2 Technological Innovations in the Residential Construction Sector

4.3 Industry Value Chain/Supply Chain Analysis

4.4 Government Initiatives and Regulatory Aspects in the Indian Residential Construction Market

4.5 Insights into Rental Yields

4.6 Insights into Affordable Housing Support Provided by Government and Public-private Partnerships

4.7 Insights into Services allied to Construction (Design and Engineering, Fit-out Services, Facility management, etc.)

4.8 Insights into Costs Related to Construction and Building Materials

4.9 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Government Initiatives Promoting Affordable Housing

5.1.2 Economic Growth and Rising Disposable Incomes

5.2 Market Restraints/Challenges

5.2.1 Shortage of Skilled Labor

5.2.2 Fluctuating Construction Materials Costs

5.3 Market Opportunities

5.3.1 Growing Awareness of Sustainable and Energy Efficient Construction Practices

5.3.2 Surge in Renovation and Retrofitting Projects

5.4 Industry Attractiveness - Porter's Five Forces Analysis

6 MARKET SEGMENTATION

6.1 By Type

6.1.1 Apartments and Condominiums

6.1.2 Villas

6.1.3 Other Types

6.2 By Construction Type

6.2.1 New Construction

6.2.2 Renovation

7 COMPETITIVE LANDSCAPE

7.1 Overview (Market Concentration and Major Players)

7.2 Company Profiles

- Delhi Land & Finance

- Merlin Group

- StepsStone Builders

- Godrej Properties Limited

- Prestige Group

- Puravankara

- Ansal API

- Mahindra Lifespace

- buildAhome

- VGN Projects Estates Pvt. Ltd.

8 FUTURE OF THE MARKET

For more information about this report visit https://www.researchandmarkets.com/r/skymc5

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world's leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Attachment