Dublin, Dec. 18, 2025 (GLOBE NEWSWIRE) -- The "Automotive Commodities Market - Global Forecast 2025-2032" has been added to ResearchAndMarkets.com's offering.

The Automotive Commodities Market is projected to experience robust growth from USD 409.01 billion in 2024 to USD 710.36 billion by 2032, driven by a compound annual growth rate (CAGR) of 7.14%. In the rapidly changing automotive industry, foundational materials play a crucial role in enabling innovation, scaling operations, and meeting new consumer demands. As electrification and autonomous driving technologies become more prevalent, the interplay between raw material availability, supply chain resilience, and cost management becomes more significant. This report provides a framework to understand the forces reshaping the market, helping decision-makers strategically navigate challenges and opportunities for sustained growth.

Transformative Shifts in Automotive Commodities

The automotive commodities market is undergoing profound changes as electrification shifts demand from traditional materials to high-performance alloys and composite materials for battery enclosures and structural components. The advancement of circular economy principles encourages manufacturers to invest in recycling technologies to reduce reliance on virgin resources. Furthermore, digitalization in the supply chain is enhancing real-time visibility and inventory management to mitigate risks associated with counterfeit inputs. Suppliers adopting lower-carbon production processes are achieving both cost efficiencies and enhanced environmental credentials.

By understanding these shifts, companies can secure competitive advantages through strategic foresight, gaining both cost efficiencies and improved sustainability standings.

Key Takeaways from This Report

- The trend towards electrification and sustainability is reshaping material demands, necessitating industry-wide shifts in supply chain strategies.

- U.S. tariff changes in 2025 will prompt companies to reevaluate sourcing strategies and enhance collaboration with suppliers for stability and cost-effectiveness.

- Emerging technologies in blockchain and IoT offer solutions for real-time supply chain management and risk mitigation.

- Regional dynamics, especially in Asia-Pacific, play a crucial role in determining material availability and cost structures, impacting global market flows.

- Strategic collaborations and investments in sustainable materials can unlock new opportunities for cost savings and environmental leadership.

Segmentation Analysis

- Steel

- Coated Steel: Electrogalvanized, Galvanized

- Cold Rolled Steel

- Hot Rolled Steel

- Aluminum

- Primary Aluminum

- Secondary Aluminum

- Plastic

- Polyethylene: HDPE, LDPE

- Polypropylene

- Polyvinyl Chloride

- Rubber

- Natural Rubber

- Synthetic Rubber: BR, NBR, SBR

- Glass

- Aftermarket Glass

- OEM Glass: Rear Glass, Side Glass, Windshield

- Copper

- Copper Alloy: Brass, Bronze

- Pure Copper

Regional Dynamics

Each region brings unique influences on material flow and cost structures. For example, Asia-Pacific's dominance in automotive commodity processing is bolstered by its response to the growing demand for electric vehicles, offering opportunities for strategic competitive positioning. Meanwhile, America's established steel and aluminum capacity provides a strong base, while regulations around emissions drive innovations in low-carbon processes.

Conclusion

In conclusion, navigating the rapidly evolving landscape of automotive commodities requires strategic insights into technological trends, regional dynamics, and tariff implications. By synthesizing these elements, industry leaders can enhance their competitive differentiation and financial performance while achieving environmental goals. This report offers a comprehensive guide and strategic insights that empower decision-makers to fortify supply chains, mitigate risks, and capitalize on the burgeoning opportunities in the automotive commodities market.

Key Attributes:

| Report Attribute | Details |

| No. of Pages | 188 |

| Forecast Period | 2025 - 2032 |

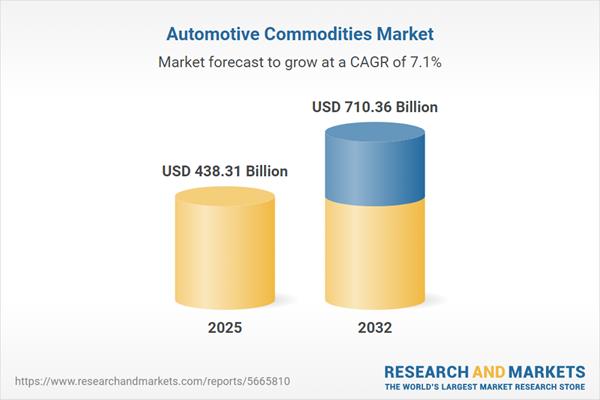

| Estimated Market Value (USD) in 2025 | $438.31 Billion |

| Forecasted Market Value (USD) by 2032 | $710.36 Billion |

| Compound Annual Growth Rate | 7.1% |

| Regions Covered | Global |

Companies Featured

The companies profiled in this Automotive Commodities market report include:

- China Baowu Steel Group Co., Ltd.

- ArcelorMittal S.A.

- Hesteel Group Co., Ltd.

- Nippon Steel Corporation

- POSCO Co., Ltd.

- Ansteel Group Corporation Limited

- JFE Holdings, Inc.

- Jiangsu Shagang Group Co., Ltd.

- Tata Steel Limited

- Nucor Corporation

For more information about this report visit https://www.researchandmarkets.com/r/qtcw4f

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world's leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Attachment