Contact Information: Media Contact: Michelle Sabolich Atomic PR for Clear Capital (415) 402-0230

Clear Capital(TM) Reports Late-Summer Softening of Home Price Gains and Reduced REO Saturation Rates

National Quarterly Price Gains (6.3%) Begin to Soften as We Move Into Fall and Winter; REO Saturation Rates (28.6%) Continue to Decline; Riverside, CA and Orlando, FL Return Quarterly Gains for the First Time in Three Years; and Baltimore, MD Ends Seven Quarters of Price Declines

| Source: Clear Capital

TRUCKEE, CA--(Marketwire - October 7, 2009) - Clear Capital (www.clearcapital.com), a premium

provider of data and solutions for real estate asset valuation, investment

and risk assessment, today released its Home Data Index™ (HDI) Market

Report. Patent pending rolling quarter technology significantly reduces the

multi-month lag time associated with other indices to help investors, loan

servicers and individual buyers and sellers make more informed, timely and

profitable decisions. This month's report features data compiled through

Sept. 25, 2009.

Key report highlights include:

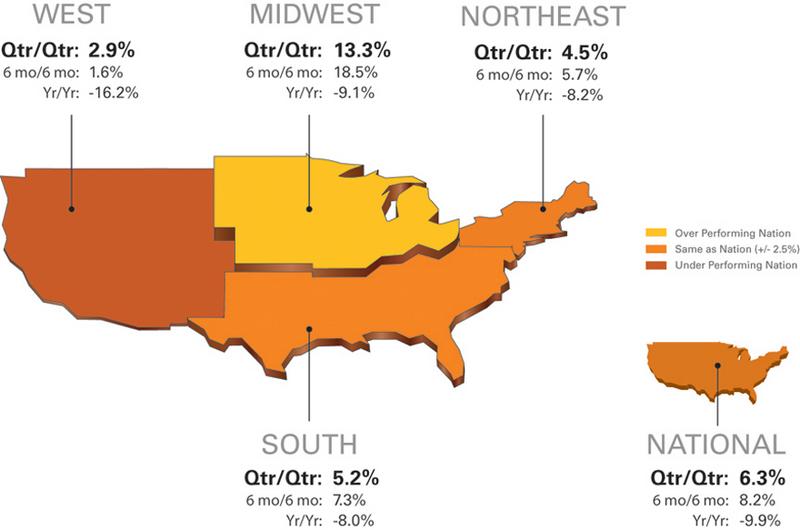

-- National / Four Region Overview: National quarterly price gains

soften to 6.3 percent, and the national yearly decline returns to the

single digit numbers (-9.9%) for the first time since summer of 2007.

The West region continues its price improvement, posting 2.9 percent

quarterly and 1.6 percent six-month gains. The national real estate

owned (REO) saturation rate (percentage of REOs sold to all properties

sold in the last rolling quarter) dropped to 28.6 percent.

-- Metropolitan Statistical Area (MSA) drilldown: Riverside, CA and

Orlando, FL return first positive quarterly price gains since mid-2006,

(0.5% and 1.2%, respectively).

-- Micro Market Analysis: Baltimore, MD returned positive quarterly

price gains (0.1%) after seven consecutive quarters of decline.

The Clear Capital HDI Market Report offers the industry, investors and

lenders a near real-time look at pricing conditions not only at the

national and metropolitan level, but within local markets. Clear Capital

data is built on the most recent data available from recorder/assessor

offices, and then further enhanced by adding the Company's proprietary

market data for the most comprehensive geographic coverage available.

"As anticipated, the strong gains we've been experiencing this summer are

showing signs of softening," said Kevin Marshall, Clear Capital President.

"But growth remains sufficiently strong -- providing hope as we head into a

winter that will test the strength of the recovery."

"Prices remain low, driving investor activity into the non-REO marketplace

across the nation. This is a good sign that the recovery is reaching beyond

the distressed segment," added Marshall. "Historically, investors move in

at the bottom which creates confidence for the bargain hunting fair-market

buyers to enter the market as well."

National/Four Region Market Overview (Aug. 27, 2008 - Sept. 25, 2009)

Quarterly price gains softened from last month, but remain substantial

across all four regions. The national year-over-year price decline was

trimmed by 2.2 percent from last month, producing the first single digit

loss (-9.9%) for the nation since the summer of 2007.

Generally seen as an improvement, the national REO saturation rate declined

1.5 percentage points to 28.6% from last month's quarterly value of 30.1

percent. With the reported decline being 3.2 percent last month, this

month's 1.5 point decline represents continued improvement, but at a

slowing rate. While the rate of improvement may be slowing, the impact of

declining saturation rates has been significant, with the current level

being 12.3 percentage points lower than the rates of last winter.

Despite the positive signs, a year-over-year price decline reminiscent of

2007 and marked reductions of the REO Saturation rate, we're still far from

the 10 percent REO saturation rates seen in 2007. Amid these conditions,

it's notable that the recent price gains have occurred alongside a record

number of REO sales, indicating that the reductions in REO Saturation has

been caused by non-REO sale volumes outpacing the growth in REO sales.

This demand for the non-REO segment is important if a broad recovery is to

be sustained.

The quarterly gains in the Midwest (13.3%) have brought its year-over-year

loss (-9.1%) close to that of the South (-8.0%) and Northeast (-8.2%),

leaving the West with the lowest quarterly gains (2.9%) and largest yearly

losses (-16.2%) for the group.

Metro Markets (Aug. 27, 2008 - Sept. 25, 2009)

Spurred by a growing shift in sales to the non-REO segment of the market,

the

Cleveland, OH MSA paced the highest performing major markets for the fourth

month in a row, maintaining price gains of more than 50 percent. Even if

only the homes in the top price tier (homes valued at more than $160,000)

were counted, Cleveland would still return a 19.9 percent quarterly gain,

keeping it at the top of the list.

Overall, these markets continue to produce strong quarter-over-quarter

price gains, improving the year-over-year numbers for all but one of the

markets (Cincinnati, OH posted a minor -0.2 percent dip from last month).

Eleven of the fifteen markets saw decreased quarterly gains from those

reported last month. This marks a slowing of the price rate increases they

experienced over the past few months. While the slowing gains lead into the

seasonally slow fall and winter months, and questions remain about the

durability of the recovery, it's encouraging that REO saturation rates

continued to improve among twelve of the fifteen markets. The markets of

St. Louis, MO, San Francisco, CA, New Haven, CT, Columbus and Cleveland, OH

all experienced more than a two percent improvement (reduction) in REO

saturation rates this past month.

The San Francisco market, inclusive of the generally lower priced areas of

Oakland and Fremont, CA, appeared on the list for the first time with a

strong 11.9 percent quarterly gain and a 16 percentage point drop in REO

saturation from the previous quarter (March 2009 through May 2009). This

places San Francisco well below its peak REO saturation rate of 59.7

percent experienced last winter, and like in other markets, reflects a

broadening interest in non-REO properties.

Of the lowest performing major markets, only the top two retain negative

quarter-over-quarter price changes this month; an improvement over the four

listed on last month's report. Orlando, FL and Riverside, CA saw their

first, albeit slight, quarterly price gains since mid-2006, while Baltimore

saw its first gain since the summer of 2007. Tucson, AZ faltered slightly,

giving up last month's 0.3 percent gain for a loss of -0.5 percent.

Las Vegas, NV and Riverside, CA (the two highest REO saturated markets)

lead the group with the largest declines in saturation from last month's

numbers with 2.7 and 2.9 point declines, respectively. While Las Vegas

maintained its position at the top of the lowest performing markets for the

fourth consecutive month, fewer REO sales and a slight improvement in

non-REO activity, helped this MSA to its softest quarterly price decline

(-2.3%) since the winter of 2007. Similarly, Riverside saw a slight

quarterly price gain helped by declining REO volumes and a steady number of

non-REO sales.

Though most markets on this list experienced softening price declines or

modest gains, several markets still have highly elevated saturation rates.

Compared to the highest performing major markets, where no market had an

REO saturation rate above 40 percent, the lowest performing major markets

list still finds six markets above 40 percent in REO saturation. This

indicates additional risk still exists for these markets unless the non-REO

segment can manage to maintain strength during the upcoming winter.

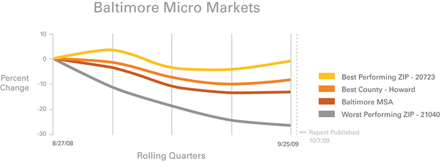

Micro Markets (Aug. 27, 2008 - Sept. 25, 2009)

This section highlights a single market every month with a deeper dive into

how the micro- and macro-markets relate to each other.

Baltimore's micro markets returned to a positive quarterly gain (0.1%)

after seven consecutive quarters of decline, contributing to a 21.0 percent

decline in home values since its market peaked in late 2006. As a whole,

the Baltimore market performed similar to much of the Northeast and South,

returning modest pricing declines compared to the national decline of -31.6

percent since the market peaked. REO saturation rates in Baltimore also

remained below the national rate, peaking at only 19.5 percent last spring.

However, a disparity exists within Baltimore's micro markets, with notable

differences between the REO-saturated city limits and the more distant

suburbs -- particularly those suburbs to the Southwest which are closer to

the better performing housing markets of Washington, D.C. Within the city

limits of Baltimore, REO saturation peaked last winter at 31.5 percent due

to declining non-REO sales amidst growing REO activity. These conditions

reflected a -17.7 percent decline in price the last year alone;

significantly worse than the more suburban southern counties of Carroll

(-11.7%) and Howard (-7.9%), which peaked at less than 19 percent REO

saturation.

While its market has not fully recovered, the suburban city of Laurel (ZIP

20723) is proving more resilient to price declines (-0.9%) this past year

than the Baltimore market as a whole. Laurel seems well-served by its

location between the two metro cores of Baltimore and Washington, D.C. and

its proximity to Interstate 95 and the Baltimore-Washington Parkway. Even

though Laurel has seen its number of REO sales grow over the past year, in

recent months the city has maintained a healthier amount of non-REO sales

activity than the city's core.

Edgewood (ZIP 21040), on the other hand, continues to perform well below

the Baltimore market, experiencing a -24.5 percent year-over-year price

change. REO saturation in Edgewood continues to climb and has reached 34.3

percent. Combine this with its predominantly lower-tier priced homes and

proximity to the Aberdeen Proving Ground, a nearby arsenal to the south;

Edgewood is the worst performing ZIP in the area.

Clear Capital Home Data Index™ Methodology

The Clear Capital Home Data Index (HDI) provides weighted paired sales, and

price-per-square-foot index models that use multiple sale types, including

single-family homes, multi-family homes and condominiums. These models are

combined with an address-level cascade to provide sale-type-specific

analysis for thousands of geographic areas across the country. The indices

include both fair market and institutional (real estate owned)

transactions. They also provide indicators of REO activity such as REO

discount rates, REO days on market and REO saturation. The Clear Capital

HDI generates indices in patent pending rolling quarter intervals that

compare the most recent four months to the previous three months. The

rolling quarters have no fixed start date and can be used to generate

indices as data flows in, or at any arbitrary time period.

About Clear Capital

Clear Capital (www.clearcapital.com) is a premium provider of data and

solutions for real estate asset valuation and risk assessment for large

financial services companies. Our products include appraisals, broker-price

opinions, property condition inspections, value reconciliations, and home

data indices. Clear Capital's combination of progressive technology, high

caliber in-house staff and a well-trained network of more than 40,000 field

experts sets a new standard for accurate, up-to-date and well documented

valuation data and assessments. The Company's customers include 75 percent

of the largest U.S. banks, investment firms and other financial

organizations.

Legend

Address Level Cascade - Provides the most granular market data available.

From the subject property, progressively steps out from the smallest market

to larger markets until data density and statistical confidence are

sufficient to return a market trend.

Home Data Index (HDI) - Major intelligence offering that provides

contextual data augmenting other, human-based valuation tools. Clear

Capital's multi-model approach combines address-level accuracy with the

most current proprietary home pricing data available.

Metropolitan Statistical Area (MSA) - Geographic entities defined by the

U.S. Office of Management and Budget (OMB) for use by Federal statistical

agencies in collecting, tabulating, and publishing Federal statistics.

Paired Sales Model - Weighted linear model based on repeat sales of same

property over time.

Price Per Square Foot (PPSF) Model - Median price movement of sale prices

divided by square footage over a period of time -- most commonly a quarter.

Real Estate Owned (REO) Saturation - Calculates the percentage of REOs sold

as compared to all properties sold in the last rolling quarter.

Rolling Quarters - Patent pending rolling quarters compare the most recent

four months to the previous three months.

The information contained in this report is based on sources that are

deemed to be reliable; however no representation or warranty is made as to

the accuracy, completeness, or fitness for any particular purpose of any

information contained herein. This report is not intended as investment

advice, and should not be viewed as any guarantee of value, condition, or

other attribute.