Contact Information: Media Contact: Michelle Sabolich Atomic PR for Clear Capital (415) 402-0230

Clear Capital(TM) Reports U.S. Home Price Gains Shrink to 3.7%

National Quarterly Price Gains Continue to Slow as the Winter Season Approaches; Investor Activity Helps Riverside, Calif. and Miami, Fla. Price Improvements; and Muted REO Influences Help Limit Price Declines in Seattle, Wash.

| Source: Clear Capital, Inc.

TRUCKEE, CA--(Marketwire - November 5, 2009) - Clear Capital (www.clearcapital.com), a premium

provider of data and solutions for real estate asset valuation, investment

and risk assessment, today released its Home Data Index™ (HDI) Market

Report. Patent pending rolling quarter technology significantly reduces the

multi-month lag time associated with other indices to help investors, loan

servicers and individual buyers and sellers make more informed, timely and

profitable decisions. This month's report features data compiled through

Oct. 25, 2009.

Report highlights include:

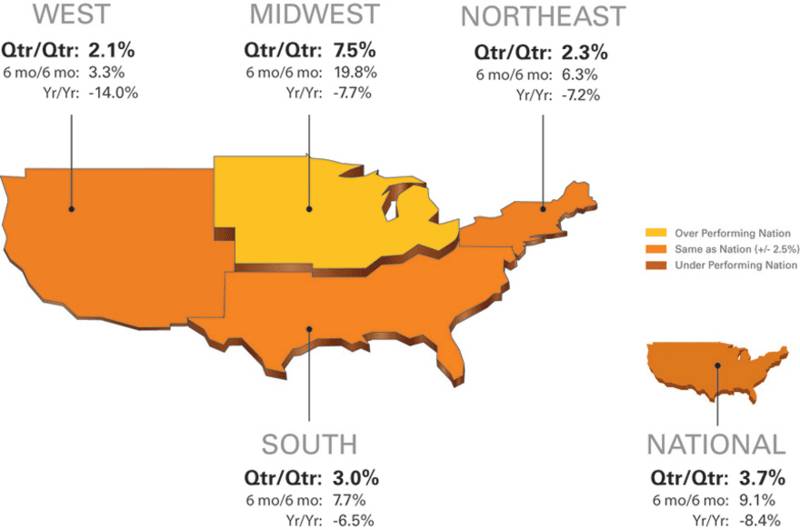

-- National / Four Region Overview: The national quarterly price change

extended its softening trend, posting a 3.7 percent gain, while the

national year-over-year price decline was trimmed again, producing single

digit losses for the second month in a row (-8.4%).

-- Metropolitan Statistical Area (MSA) drilldown: Quarterly price gains

remained strong among the highest performing major markets, helped by the

continued decline in the percentage of total sales that are real estate

owned (REO).

-- Micro Market Analysis: Steep declines in the first half of this past

year produced a -13.8 percent yearly price change for the Seattle MSA.

The Clear Capital HDI Market Report offers the industry, investors and

lenders a near real-time look at pricing conditions not only at the

national and metropolitan level, but within local markets. Clear Capital

data is built on the most recent data available from recorder/assessor

offices, and then further enhanced by adding the Company's proprietary

market data for the most comprehensive geographic coverage available.

"Nationally, both the top and bottom performing markets are converging to

modest quarterly changes, indicating a return to stable markets," said Alex

Villacorta, Sr. Statistician, Clear Capital. "As we've seen since the

spring season, many markets have returned to traditional seasonal

fluctuations and the strong summer gains are showing signs of slowing."

"The continued decline in REO saturation rates, as well as an increase in

the proportion of cash buyers in both distressed and fair market sales, are

an encouraging sign of investor optimism coming into the traditionally slow

months," added Villacorta. "If the home buyer tax credit is extended and

possibly expanded, it could add even more momentum through the slow months

to build up to a very strong spring in 2010 as more buyers are sensing that

home prices truly have hit the bottom of the current cycle."

National/Four Region Market Overview (Sept. 26, 2008 - Oct. 25, 2009)

The national year-over-year price decline was trimmed another 1.5 percent

from last month, producing single digit losses for the second month in a

row (-8.4%). The national quarterly price change extended its softening

trend, posting 3.7 percent gains -- down from the 6.3 percent gains

experienced last month. This pattern held true across all four regions

which continue to post more consistent price changes, a likely reflection

of more uniform lending and foreclosure practices, along with a reduced

influence of the REO segment. This month's national REO saturation rate

declined to 28.0 percent -- a 5.1 percent improvement since July.

The softening gains reflect a step back from this year's strong summer

price increases spurred by the deeply discounted prices of last winter,

homebuyer incentives and a general sense by investors that the bottom of

the price decline was occurring. Investor activity does appear to be on the

rise. This past year, the proportion of REO purchases made with cash grew

12.4 percent. Homes purchased with cash, compared to a traditional

mortgage, are more prevalent among investors than those purchasing a

primary residence. The magnitude of this increase indicates investor

activity is contributing to the recent gains in home prices and has the

potential to carry us through the normally slower winter season.

Metro Markets (Sept. 26, 2008 - Oct. 25, 2009)

Quarterly price gains remain strong among the highest performing major

markets, helped by the continued decline in the percentage of total sales

that are real estate owned (REO). Only New Orleans, La., Louisville, Ky.

and Cleveland, Ohio saw increased REO saturation rates, and even then the

increases were slight (less than one-half percent each).

Excluding the additional one percent quarterly improvement in New Haven,

Conn., all the markets experienced slowing quarterly price gains,

continuing last month's general shift to more moderate gains. On average,

the highest performing major markets saw a decrease of 5.5 percent in their

quarterly gains. If this trend continues into the winter, it is possible

that some of the current top performers will see single digit quarterly

gains or even quarterly declines by the new year. This plausible scenario,

while a slowdown, would still represent a significant improvement from the

extreme and broad price declines and elevated REO saturation levels

experienced last winter.

Of particular note, the price spike we've seen in Cleveland has started to

diminish, dropping to 26.0 percent for the quarter, while continuing to

post a strong yearly price increase (50.4%). Cleveland returned a flat REO

saturation rate as compared to last month, as well.

The lowest performing major markets continue to reflect the relatively

healthy changes that occurred across the nation in recent months, with only

two modest quarter-over-quarter losses present. However, the similarly

minor and reduced gains in these markets serve caution that we may

experience a pause in price increases as we head into winter. Las Vegas,

Nev., Tucson, Ariz. and Riverside, Calif. saw slight improvements in their

quarterly gains compared to last month, while the remaining 12 markets saw

continued gains but of reduced magnitude.

Raleigh, N.C. experienced the largest increase in REO saturation since last

month, but its modest 1.4 percent increase reflects a general stability in

these markets. Although five other markets (Seattle, Richmond,

Jacksonville, Charlotte and Tucson) experienced minor increases in REO

saturation, the average increase was just 0.7 percent. The remaining nine

markets saw declining REO saturation rates, generally seen as a positive

sign, with a combined average reduction of 2.1 percent.

The Riverside and Miami MSAs continue to experience improved results,

having dropped from near the top to the bottom of the list over the past

few months. Both are experiencing a much higher percentage of cash sales,

which is indicative of heightened demand by investors for all property

types, not just REOs. Historically, these markets have seen cash sales

account for less than ten percent of all non-REO sales. Currently,

Riverside is seeing 23.6 percent of all non-REO sales completed without

financing (i.e. cash sales), and Miami is experiencing an even greater 30.3

percent. These high percentages in non-REO cash sales highlight the

magnitude of investment activity which has spread beyond the REO segment.

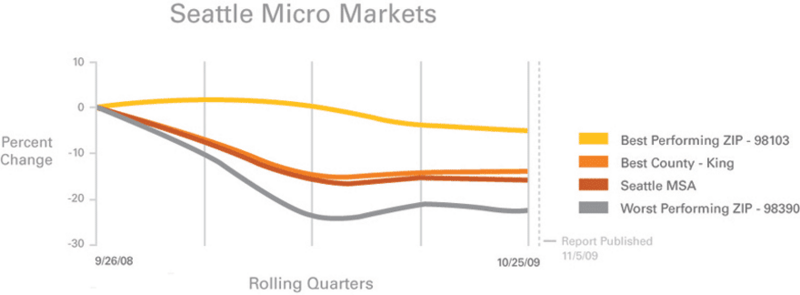

Micro Markets (Sept. 26, 2008 - Oct. 25, 2009)

This section highlights a single market every month with a deeper dive into

how the micro- and macro-markets relate to each other.

Steep declines in the first half of this past year produced a -13.8 percent

price change for the Seattle MSA. Compared to most of the major western

markets, however, the overall price decline in Seattle was less severe

because of muted REO influences. For the most part, Seattle's REO

saturation rate has remained below 20 percent percent, spiking briefly last

winter at 24.7 percent, before returning to its current rate of 15.8

percent.

A latecomer to the housing market decline, Seattle didn't experience a

reduction in prices until the fall of 2007 -- a full year after home prices

generally began to fall across the nation. Seven consecutive quarters of

decline followed, ending in an abrupt halt this past spring, making the

recovery to date resemble a floor. In total, Seattle home prices fell 23.4

percent since they peaked in the fall of 2007.

In contrast to last month's micro market report on Baltimore, Md., support

for home prices emanated from Seattle's popular city center. The urban and

scenic areas to the north of downtown, as compared to the more industrial

south end of town, have fared relatively well during the downturn.

Immediately north of the financial district and across Lake Union resides

the best performing area (ZIP 98103) with a price change of only -14.8

percent since the peak and -5.6 percent for the year. The close proximity

to downtown and the University of Washington has helped support home prices

in this neighborhood.

Well south of the city's core, and east of Tacoma, lies the small town of

Sumner (ZIP 98390). Lacking the financial base that benefits Seattle and

Tacoma, and outside the typical Seattle commute, Sumner represents the more

rural region of the micro market. While not substantially worse off than

its immediate neighbors, Sumner has experienced the greatest price decline

in the MSA for the year (-20.6%). Despite the steeper declines early in the

year, however, Sumner has followed the general trend for the MSA, reaching

a floor six months ago and has demonstrated a 1.2 percent gain since.

Clear Capital Home Data Index™ Methodology

The Clear Capital Home Data Index (HDI) provides weighted paired sales, and

price-per-square-foot index models that use multiple sale types, including

single-family homes, multi-family homes and condominiums. These models are

combined with an address-level cascade to provide sale-type-specific

analysis for thousands of geographic areas across the country. The indices

include both fair market and institutional (real estate owned)

transactions. They also provide indicators of REO activity such as REO

discount rates, REO days on market and REO saturation. The Clear Capital

HDI generates indices in patent pending rolling quarter intervals that

compare the most recent four months to the previous three months. The

rolling quarters have no fixed start date and can be used to generate

indices as data flows in, or at any arbitrary time period.

About Clear Capital

Clear Capital (www.clearcapital.com) is a premium provider of data and

solutions for real estate asset valuation and risk assessment for large

financial services companies. Our products include appraisals, broker-price

opinions, property condition inspections, value reconciliations, and home

data indices. Clear Capital's combination of progressive technology, high

caliber in-house staff and a well-trained network of more than 40,000 field

experts sets a new standard for accurate, up-to-date and well documented

valuation data and assessments. The Company's customers include 75 percent

of the largest U.S. banks, investment firms and other financial

organizations.

Legend

Address Level Cascade -- Provides the most granular market data available.

From the subject property, progressively steps out from the smallest market

to larger markets until data density and statistical confidence are

sufficient to return a market trend.

Home Data Index (HDI) -- Major intelligence offering that provides

contextual data augmenting other, human-based valuation tools. Clear

Capital's multi-model approach combines address-level accuracy with the

most current proprietary home pricing data available.

Metropolitan Statistical Area (MSA) -- Geographic entities defined by the

U.S. Office of Management and Budget (OMB) for use by Federal statistical

agencies in collecting, tabulating, and publishing Federal statistics.

Paired Sales Model -- Weighted linear model based on repeat sales of same

property over time.

Price Per Square Foot (PPSF) Model -- Median price movement of sale prices

divided by square footage over a period of time -- most commonly a quarter.

Real Estate Owned (REO) Saturation -- Calculates the percentage of REOs

sold as compared to all properties sold in the last rolling quarter.

Rolling Quarters -- Patent pending rolling quarters compare the most recent

four months to the previous three months.

The information contained in this report is based on sources that are

deemed to be reliable; however no representation or warranty is made as to

the accuracy, completeness, or fitness for any particular purpose of any

information contained herein. This report is not intended as investment

advice, and should not be viewed as any guarantee of value, condition, or

other attribute.