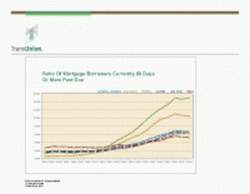

CHICAGO, IL--(Marketwire - August 17, 2010) - TransUnion's quarterly analysis of trends in the mortgage industry found that national mortgage loan delinquency rate (the ratio of borrowers 60 or more days past due) decreased again in the second quarter of 2010, suggesting that the credit conditions in the housing sector have now begun to stabilize. However, the delinquency rate only dropped to 6.67 percent -- a level marginally lower than in the first quarter of this year.

This statistic, which is traditionally seen as a precursor to foreclosure, reflects a decrease of 1.48 percent from the previous quarter's 6.77 percent national average. Year over year, mortgage borrower delinquency is still up approximately 14.8 percent (from 5.81 percent in the second quarter 2009).

The report is part of an ongoing series of quarterly consumer lending sector analyses focusing on credit card, auto loan and mortgage data available on TransUnion's Web site. Information for this analysis is culled quarterly from approximately 27 million anonymous, randomly sampled, individual credit files, representing approximately 10 percent of credit-active U.S. consumers and providing a real-life perspective on how they are managing their credit health.

Quarterly Statistics

Mortgage borrower delinquency rates in the second quarter of 2010 continued to be highest in Nevada (15.86 percent) and Florida (15.02 percent), while the lowest mortgage delinquency rates continued to be found in North Dakota (1.61 percent), South Dakota (2.23 percent) and Nebraska (2.61 percent). Twelve states showed increases in delinquency from the previous quarter with Rhode Island (+4.63 percent), New Mexico (+4.45 percent) and Washington (+3.39 percent) leading the pack.

Measures of later-stage mortgage delinquency, such as the ratio of borrowers 90 or 120 or more days past due, provide additional positive news. For the first time since before the recession began in 2007, these later-state delinquencies rates have now both declined nationally from where they were last quarter.

The average national mortgage debt per borrower again decreased (0.77 percent) to $191,284 from the previous quarter's $192,774. On a year-over-year basis, the second quarter 2010 average represents a 1.3 percent decrease over the second quarter 2009 average mortgage debt per borrower level of $193,811. The area with the highest average mortgage debt per borrower continued to be the District of Columbia at $366,627, followed by California at $345,502 and Hawaii at $311,130. The lowest average mortgage debt per borrower remained in West Virginia at $99,206. Quarter over quarter, Vermont showed the greatest percentage increase in mortgage debt (+2.1 percent), followed by New Mexico (+1.96 percent) and North Dakota (+0.65 percent). Areas showing the largest percentage drop in average mortgage debt were Nevada (-3.12 percent), Arizona (-3.0 percent) and Florida (-1.80 percent).

On a year-over-year basis at a national level, mortgage originations dropped almost 50 percent. The drop was across all states, with the smallest decline in year-over-year originations seen in North Dakota (-26.8 percent) and Arkansas (-31.4 percent). Idaho and Wisconsin experienced the steepest year-over-year declines (-58.7 percent and -58.6 percent, respectively).

Analysis

"The second quarter decline in mortgage delinquency gives further credence to the notion that the credit market is stabilizing. Although this is good news for the consumer, the economy is still burdened by high unemployment, upcoming ARM resets and a glut of foreclosures," said FJ Guarrera, vice president in TransUnion's financial services business unit.

"The dynamics inside the mortgage market are changing. It is ironic that, with record-setting low interest rates, a large inventory of homes and low home prices, this is one of the most affordable times to buy a house within the last 50 years -- yet most consumers are not considering a home purchase the investment opportunity it was considered in the past. Add to that irony and concurrent with these near perfect consumer buying conditions, tighter lending standards and increased documentation scrutiny have made it difficult for many consumers to qualify for a mortgage."

Just as mortgage delinquency trends differ between the national and state economies, metropolitan areas also showed different movements in the second quarter of this year. Sixty-two percent of the metropolitan statistical areas (MSAs) showed a decrease in their 60-day mortgage delinquency rates since last quarter, as compared to a 59 percent between the fourth quarter of last year and first quarter of 2010.

Changes are even more significant in later stage delinquency measures. Sixty-four percent of all MSAs showed a decrease in their 90-day mortgage delinquency measure as compared to only 45 percent from the previous period. Furthermore, the percentage of MSAs showing a decline in their 120-day delinquency ratio almost doubled from the previous quarter-over-quarter levels.

Forecast

"TransUnion believes that the 60-day mortgage delinquency rate will likely continue to drift downward in 2010, possibly nearing 6.4 percent nationally by the end of the year. Note that this forecast is based on various economic assumptions, including the assumption that both real estate values and the unemployment picture will improve gradually. This forecast would certainly change if there are unanticipated shocks to the economy affecting the recovery in the housing market," said Guarrera.

With regard to regional forecasts, Florida is again anticipated to experience the highest mortgage delinquency rate by the end of 2010, reaching as high as 16.2 percent. North Dakota is still expected to continue to exhibit the lowest mortgage delinquency by year-end with a rate of 1.5 percent.

TransUnion's Trend Data(SM) database

The source of the underlying data used for this analysis is TransUnion's Trend Data, a one-of-a-kind database consisting of 27 million anonymous consumer records randomly sampled every quarter from TransUnion's national consumer credit database. Each record contains more than 200 credit variables that illustrate consumer credit usage and performance. Since 1992, TransUnion has been aggregating this information at the county, Metropolitan Statistical Area (MSA), state and national levels.

About TransUnion

As a global leader in credit and information management, TransUnion creates advantages for millions of people around the world by gathering, analyzing and delivering information. For businesses, TransUnion helps improve efficiency, manage risk, reduce costs and increase revenue by delivering comprehensive data and advanced analytics and decisioning. For consumers, TransUnion provides the tools, resources and education to help manage their credit health and achieve their financial goals. Through these and other efforts, TransUnion is working to build stronger economies worldwide. Founded in 1968 and headquartered in Chicago, TransUnion employs associates in more than 25 countries on five continents. www.transunion.com/business

Contact Information:

Contact

Dave Blumberg

TransUnion

E-mail:

Telephone: 312 972 6646

Clifton ONeal

TransUnion

Telephone: 312 985 2540