TORONTO, ONTARIO--(Marketwire - Aug. 2, 2011) - Centamin Egypt Limited ("Centamin" or "the Company") (TSX:CEE)(LSE:CEY) is pleased to announce its quarterly update.

HIGHLIGHTS

Operations

- Quarterly gold production of 47,991 ounces was achieved from the Sukari Gold Mine.

- Cash operating cost averaged US$606 per ounce for the quarter.

- Average gold sales price received was US$1,545 per ounce.

- Reduced blasting activities due to irregular issues of blast products by Blast Inspectors negatively impacted open pit and underground production, and as a result, gold production. The Company is confident issuing practices will return to normal in Q3.

- As a result of the reduced blasting in Q2, the Company has been unable to recover as initially expected from the supply interruptions in Q1. With the expectation of blasting activities returning to previous levels in Q3, the Company has revised its guidance to 200-210,000 ounces for 2011 at a cash cost of approximately $550 per ounce.

- The underground operation commenced Commercial Production during the quarter with a total of 43kt @ 12.5 g/t being extracted.

- Maiden grade controlled underground ore reserve of 126,000t @ 11.9 g/t with definition drilling ongoing.

Mine Expansion / Development

- Stage 4 expansion to 10Mtpa was approved by the Board for a capital cost of US$255m (excluding contingency). Long lead items have been ordered and significant contracts awarded with commissioning expected to take place in Q1 2013.

- Planning and modelling commenced for a secondary decline development accessing the northern high grade Julius Zone of the Sukari porphyry.

- Regional exploration returned significant intercepts for first pass drilling at the V Shear prospect (approximately 3km north of the Sukari process plant) including 16m @ 3.00g/t from 151m. Follow up programmes are currently being planned.

Corporate/Finance Activities

- Quarterly operating profit of US$48.2m versus US$19.1m Q2 2010

- Cash and liquid assets of US$201M versus US$35m Q2 2010 (liquid assets includes $17m in share investments and $38m gold bullion)

- On 11 July 2011, the Company announced an offer for Sheba Exploration (UK) Plc, a PLUS listed UK registered company ("Sheba"). Sheba holds highly prospective mineral exploration licences in Ethiopia. On 29 July 2011, the offer was made unconditional with over 90% acceptances received.

- The Company remains debt free and unhedged.

- All capital and ongoing operating expenses in Egypt continue to be financed from cash flows generated by gold revenues from the Sukari Gold Mine.

Commenting on the quarterly results, Josef El-Raghy, Chairman of Centamin, said:

"The quarter enjoyed significant progress on the development of our underground operations, as well as defining the future production profile of Sukari with the approval for the construction of Stage 4. We continue to demonstrate the continued high prospectivity of our Sukari concession and we are excited with our entry into Ethiopia where we believe we will deliver value growth through exploration success and further development in a region where we have already delivered."

Centamin Egypt Limited will host a conference call on Tuesday, 02 August 2011 at 11:00am (London, UK time) to update investors and analysts on its quarterly results. Participants may join the call by dialling one of the following four numbers, approximately 10 minutes before the start of the call. Participant pass code: 862573#

| From UK: (toll free) 0800 368 1895 | From US: (toll free) 1866 928 6049 | |

| From Canada: (toll free) 1866 561 8617 | From rest of world: + 44 20 3140 0693 |

A live audio webcast of the call will be available on: http://mediaserve.buchanan.uk.com/2011/centamin020811/registration.asp

A replay of the webcast will be available on the same link from 12.30 pm (London, UK time) on Tuesday, 02 August 2011.

SUKARI GOLD MINE

Production Statistics

| June 2011 Quarter |

March 2011 Quarter |

December 2010 Quarter |

September 2010 Quarter |

|||||||

| Open Pit Ore Mined | ('000t) | (1) 1,039 | 1,212 | 2,123 | 1,682 | |||||

| Total Open Pit Material Mined | ('000t) | 3,030 | 4,552 | 5,975 | 4,916 | |||||

| Strip Ratio | waste/ore | 1.9 | 2.8 | 1.8 | 1.9 | |||||

| U/ground Development Ore Mined | ('000t) | 39 | 41 | 40 | - | |||||

| U/ground Ore Mined | ('000t) | 4 | - | - | - | |||||

| Ore Processed | ('000t) | 850 | 741 | 773 | 605 | |||||

| Head Grade | (g/t) | 1.82 | 1.94 | 2.30 | 1.75 | |||||

| Gold Recovery | (%) | 85.0 | 86.7 | 88.1 | 82.6 | |||||

| Gold Produced - Dump Leach | (oz) | 2,765 | 2,676 | 2,387 | 3,049 | |||||

| Gold Produced - Total(2) | (oz) | 47,991 | 45,204 | 53,189 | 30,243 | |||||

| Cash Operating Cost of Production (3) | US$/oz | 606 | 525 | 498 | 638 | |||||

| Gold Sold | (oz) | 50,262 | 63,240 | 35,150 | 31,228 | |||||

| Average Sales Price | US$/oz | 1,545 | 1,405 | 1,369 | 1,239 |

| Notes:- |

| (1) Includes 224k tonnes @ 0.5 g/t placed on dump leach pads. |

| (2) Gold produced is gold poured and does not include gold-in-circuit at period end. |

| (3) Cash operating costs excludes royalties, exploration and corporate administration expenditure. |

Operational Performance Overview

Gold production was adversely affected due to below budget material movement from both open pit and underground mining operations. Whilst imports and deliveries of blast products have returned to normal and sufficient quantities exist at Sukari, daily restrictions imposed by local blast inspectors drastically curtailed mine production activities during the quarter.

The Company is confident that the recent actions by the blast inspectors are not supported or condoned by Government policy and that the company has taken appropriate action such that the company remains confident that the situation will be resolved in the 3rd quarter. Unfortunately the initial 1st quarter supply interruptions along with the more recent restricted issuance of blasting products in Sukari itself has impaired the company's ability to meet its' production targets for 2011.

With the expectation of normal product issues being restored early in the 3rd quarter a revised production guidance of 200-210,000 oz at a cash cost of approximately US$550 per ounce can be expected.

Open Pit Operations

For the June quarter, a total of 1.0mt of ore @ 1.05g/t Au was mined with a total quarterly material movement of 3.0Mt and resultant waste to ore ratio of 1.9:1.

The bench level of the Stage 1A cutback reached the 1052mRL with mining focused in this area to ensure access to the ore at the bottom of the Stage 1 where the current bench level is 1028mRL (approximately 72 metres below the Wadi level). Stage 2 mining during the period progressed to the 1112mRL.

Project work continued at the Tailings Storage Facility with material being mined for the North east wall to complete the area to 1090.3mRL.

Underground Operations

Commercial production commenced from the underground development in Sukari effective 01 May 2011 as a result of two stopes being in a position to draw ore, sufficient development headings (now on three levels) and decline advance in place to sustain a consistent ore production rate.

Definition drilling has clearly identified two significant and highly mineralized zones, the first a stacked en echelon high grade quartz vein zone on the footwall of the porphyry typically averaging between 15-20 Au g/t and the second a broader (several metres) but lower grade classical quartz stockwork zone associated with the hanging wall contact and typically having average grades of between 5-7g/t.

The higher grade zones are planned to be extracted using a longhole retreat mining method while the broader stockwork zones will utilize a bulk longhole stoping method of extraction. As is typical with such ore bodies, whilst a high degree of continuity can be expected, detailed mine planning and proven ore reserves can only be provided a maximum of 12-18 months in advance of mining activity. Currently grade controlled ore reserves stand at 126,000t @ 11.9 g/t with definition drilling ongoing.

On this basis it is likely the current underground operation will deliver higher grades at lower tonnes in the order of 250,000tpa at between 10-12g/t. This throughput is limited due to the current location and number of development headings possible for the currently defined ore zone.

As such planning has commenced for a secondary decline development to drive development towards the north of Sukari Hill and access the high grade Julius Zone. The aim of this is to potentially double the tonnage extraction rate stated above but at similar grades. The assessment and decision to proceed with this will be made in the latter part of this year.

Underground development recorded an overall advance of 638m for the quarter, including continued development of the main Amun decline (347m), ore drives and cross cut development (291m) as well as associated ventilation decline and escape way infrastructure.

Stoping commenced during the quarter, with a total of 3,865 tonnes @ 18.2g/t being stoped out. In addition, 39,152 tonnes of development ore @ 11.9g/t was mined during the quarter.

A total of 1,574m of underground definition drilling was completed during the quarter.

Process Operations

Process plant throughput for the June quarter was 850kt, 15% higher than the previous quarter with the commissioning of the secondary crushing circuit. Whilst substantially higher throughput rates have been achieved the circuit has not yet been optimised due to ore feed interruptions and the inclusion of some transitional ore to maintain feed supply which also impacted metallurgical recoveries.

Dump Leach Operations

Dump leach pads continue to be irrigated with a total placement by end of quarter of approximately 4.2Mt of low grade oxide ore at an average dumped grade of 0.5 g/t with 2,765 ounces recovered during the quarter.

Exploration

Sukari Hill

During the quarter, resource definition drilling continued to be mainly concentrated in the Hapi, Hapi Deeps and the west dipping high grade structures at Pharaoh Zone and in converting inferred resource into measured and indicated status. In total, 15,100m of diamond drilling was completed during the quarter. The current drill programme continues to show success in targeting the down dip and along strike extension of the Hapi Zone and other parallel high grade structures and/or the west dipping high grade structures as well; within the main porphyry.

Significant assays returned were as follows:-

| D1638- | 127m | @ | 2.31g/t from 684m, including | |

| 13m | @ | 7.09g/t from 770m. | ||

| D1646- | 13m | @ | 3.25 g/t from 204m. | |

| D1650- | 21m | @ | 2.41g/t from 604m. | |

| D1657- | 10m | @ | 3.35g/t from 38m. | |

| D1658- | 80m | @ | 2.95g/t from 599m. |

A revised resource and reserve estimate is planned to be produced early in the 4th quarter.

Quartz Ridge

Drilling continued at Quartz Ridge with results confirming continuity of an east-west trending mineralised structure approximately 1.5 km east of the Sukari process plant.

Current intercepts include:

| 22m | @ | 1.11g/t | from surface, including | ||

| 5m | @ | 3.90g/t | from 17m. | ||

| 11m | @ | 1.08g/t | from 58m | ||

| 5m | @ | 2.04g/t | from 31m | ||

| 4m | @ | 16.4g/t | from 156m | ||

| 5m | @ | 7.03g/t | from 42m over a 150m strike length. |

A follow up 10,000m RC program to test the strike extent of this zone will commence in the 3rd quarter followed by a resource estimate which will be included in the overall resource estimate of the project later in the year.

V- Shear

V Shear lays approximately 1km north west of Quartz Ridge and just over a kilometre from the Sukari process facility.

Following initial soil and BLEG sampling programmes 3 RC holes (600m) were drilled during the quarter with the following significant results:

| 7m | @ | 21.4 g/t | (from 28m) | ||

| 16m | @ | 3.00 g/t | (from 151m) |

The above intercepts as well as the relationship of V Shear to the Quartz Ridge mineralisation are potentially highly significant. As such a 20,000 m RC program is being planned for this area as well as a soil/rock chip sampling program between the two mineralised zones.

SUKARI GOLD MINE EXPANSION

Stage 3 Expansion – Secondary Crushing Circuit

Commissioning of the secondary crushing circuit continued throughout the quarter with no major issues being encountered. The second secondary crusher unit was installed late in the quarter as part of the overall completion of the project. Once commissioned this will provide the circuit with the additional flexibility for continuous operations and improved circuit availability that was not available during this quarter.

Ore supply interruptions during the quarter due to restricted blasting product issuance prevented the full commissioning of the circuit. This is now expected to take place during the 3rd quarter.

Stage 4 Expansion – 10Mtpa

The Stage 4 expansion project has been approved by the Board.

The Stage 4 project will increase the process capacity of the operation to 10Mtpa (currently ramping up to 5Mtpa) which will include the provision of related infrastructure and services to support the same. The key construction/mobilisation activities to be undertaken will include:

- a 5Mtpa SABC circuit along with commensurate flotation, fine grind and flotation/CIL facilities;

- a 28MW HFO/Diesel fuelled power station;

- a 25km sea water pipeline capable of delivering 900m3/hr of raw water to the process plant;

- expansion of the current tails storage facility to accommodate the larger throughput and accelerated deposition rates;

- purchase, mobilization and assembly of additional mining equipment to support the initial increase in mining rate;

- appropriate infrastructure to support the above facilities including mobile fleet workshops, expanded warehouse and offices as well as camp accommodation expansion.

As part of this approval the following long lead items and contracts have been awarded, orders placed, initial deposits paid and production slots locked in with the relevant manufacturers:

- SAG and Ball mill shells and motors;

- Initial mining mobile equipment purchases;

- Award of power plant construction (EPC) contract and ordering of engines;

- Award of Engineering and Design contract for sea water pipeline.

With the completion of the Front End Engineering and Design (FEED) phase by the company's EPCM consultants, GBM Mineral Consultants, the following total project capital cost and implementation schedule has been developed:

Stage 4 Estimated Capital Cost:

| Mining Equipment (1) | $ | 50.0 | M |

| Process Plant | $ | 110.0 | M |

| 28MW Power Plant | $ | 32.2 | M |

| Tails Storage Facility | $ | 17.8 | M |

| Sea Water Pipeline | $ | 25.8 | M |

| Infrastructure | $ | 6.6 | M |

| Plant Mobile Equipment | $ | 2.3 | M |

| Owner's Costs | $ | 10.7 | M |

| Total Project (excluding contingency) | $ | 255.4 | M |

| (1) Mining Equipment expenditure does not include replacement capital and only includes expenditure up to project completion. |

A capital cost for the above has been estimated at US$255.4M excluding contingency with project completion and commissioning scheduled to occur in the 1st quarter of 2013.

It is intended that the Stage 4 expansion will be financed entirely from cash flow generated from the Sukari Gold Project.

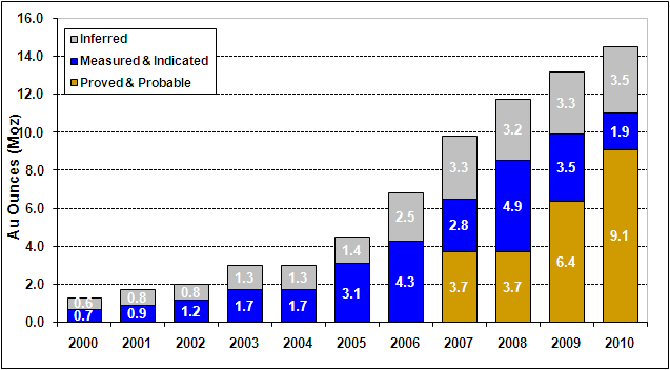

RESOURCE AND RESERVE DEFINITION

Sukari Global Resource

| 0.5 g/t Cut-off Au | Tonnes (Mt) |

Grade (g/t Au) |

Gold (Moz) |

|||

| Measured & Indicated | 235.73 | 1.45 | 10.99 | |||

| Inferred | 68.9 | 1.6 | 3.5 | |||

| TOTAL | 304.6 | 1.48 | 14.5 |

| Notes to table: Figures in table may not add correctly due to rounding. Proven and probable ore reserves are included in mineral resources. Figures are below the August 2010 mined surface. |

Sukari Mineral Reserve

| Proven | Probable | Mineral Reserve | ||||||||||

| Tonnes (Mt) |

Au (g/t) |

Tonnes (Mt) |

Au (g/t) |

Tonnes (Mt) |

Au (g/t) |

Cont Au (Moz) |

||||||

| 102.4 | 1.09 | 142.9 | 1.19 | 245.4 | 1.15 | 9.1 | ||||||

| The mineral reserves are based on the resource model announced on 08 June 2010 which includes drilling up to 31 May 2010 and below the August 2010 mined surface, a gold price of US$900 per ounce and a cut-off grade of 0.3 g/t Au for oxide transition and sulphide material. |

Sukari Global Resource and Mineral Reserve Growth

To view graph 1, please visit the following link: http://media3.marketwire.com/docs/cen_graph_1.jpg

{kind=link}

CORPORATE / FINANCE ACTIVITIES

On 11 July 2011, the Company announced an offer for Sheba Exploration (UK) Plc, a PLUS quoted company (PLUS: SHE), for the entire issued and to be issued share capital of the company. The offer is fully supported by the Sheba Board and is made on the basis of:

- A cash payment of 3.0 pence per Sheba share and,

- The number of ordinary shares in the capital of Centamin equal to the number of Sheba shares divided by 40.

Sheba owns and operates three gold and base metal exploration licences in Ethiopia. The Offer was open for acceptance until 1pm on 01 August 2011 (see Centamin announcement dated 11 July 2011).

On 29 July 2011, the Company announced that the offer had been declared unconditional in all respects, with over 90% acceptances received.

At the end of the quarter, the Company had US$201m in available cash and liquid assets. The Company remains debt free and unhedged.

On behalf of Centamin Egypt Limited

Josef El-Raghy, Chairman

02 August 2011

COMPETENT PERSONS STATEMENT

Quality Assurance and Control and Qualified Person

The information in this report that relates to ore reserves has been compiled by Mr Andrew Pardey. Mr Pardey is a Member of the Australasian Institute of Mining and Metallurgy and is a full time employee of the Company. He has sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity he is undertaking, to qualify as a "Competent Person" as defined in the 2004 Edition of the "Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves" and is a "Qualified Person" as defined in the "National Instrument 43-101 of the Canadian Securities Administrators" and "CIM Definition Standards For Mineral Resources and Mineral Reserves" of December 2005 as prepared by the CIM Standing Committee on Reserve Definitions of the Canadian Institute of Mining. Mr Pardey's written consent has been received by the Company for this information to be included in this report in the form and context which it appears.

The information in this report that relates to mineral resources is based on work completed independently by Mr Nicolas Johnson, who is a Member of the Australian Institute of Geoscientists. Mr Johnson is a full time employee of Hellman and Schofield Pty Ltd and has sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he is undertaking to qualify as a "Competent Person" as defined in the 2004 edition of the "Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves" and is a "Qualified Person" as defined in "National Instrument 43-101 of the Canadian Securities Administrators". Mr Johnson consents to the inclusion in the report of the matters based on his information in the form and context in which it appears.

Information in this report which relates to exploration, geology, sampling and drilling is based on information compiled by geologist Mr Richard Osman who is a full time employee of the Company, and is a member of the Australasian Institute of Mining and Metallurgy with more than five years experience in the fields of activity being reported on, and is a 'Competent Person' for this purpose and is a "Qualified Person" as defined in "National Instrument 43-101 of the Canadian Securities Administrators". His written consent has been received by the Company for this information to be included in this report in the form and context which it appears.

All exploration and resource samples were analysed by Ultra Trace Pty Ltd, Canning Vale, Western Australia. All mine based production samples were analysed by Sukari Assay Laboratory, Egypt.

Refer to the updated Technical Report which was filed in December 2010 for further discussion of the extent to which the estimate of mineral resources/reserves may be materially affected by any known environmental, permitting, legal, title, taxation, socio-political, or other relevant issue.

CORPORATE INFORMATION

CORPORATE DIRECTORY

| Directors | |

| Mr Josef El-Raghy, Chairman | |

| Mr Harry Michael, Chief Executive Officer | |

| Mr Trevor Schultz, Executive Director of Operations | |

| Mr Edward Haslam, Senior Non Executive Director | |

| Professor Robert Bowker, Non Executive Director | |

| Mr Mark Arnesen, Non Executive Director | |

| Mr Mark Bankes, Non Executive Director | |

| Senior Management | |

| Mr Pierre Louw, Chief Financial Officer | |

| Mr Chris Aujard, General Counsel and Company Secretary | |

| Mrs Heidi Brown, Company Secretary | |

| Registered Office | |

| 57 Kishorn Road, Mount Pleasant WA 6153, Australia | |

| Tel: + 61 8 9316 2640 | |

| Fax: + 61 8 9316 2650 | |

| Email: centamin@centamin.com | |

| Website: http://www.centamin.com/ | |

| Egypt Office | |

| 361 El-Horreya Road, Sedi Gaber, Alexandria, Egypt | |

| Tel: + 203 541 1259 | |

| Fax: + 203 522 6350 | |

| Auditor | |

| Deloitte Touche Tohmatsu | |

| Level 14, 240 St Georges Terrace, Perth WA 6000 | |

| Share Registries | |

| Australia | |

| Computershare Investor Services Pty Ltd | |

| Level 2, 45 St Georges Terrace | |

| Perth WA 6000 | |

| Canada | |

| Computershare | |

| 100 University Avenue, 8th Floor | |

| Toronto, Ontario, ONM5J 2Y1 | |

| United Kingdom | |

| Computershare Investor Services | |

| PO Box 82, The Pavilions, Bridgwater Road | |

| Stock Exchange Listings | |

| London Stock Exchange, LSE code: CEY | Toronto Stock Exchange, TSX code: CEE |

ABOUT CENTAMIN EGYPT LIMITED

Centamin is a mineral exploration, development and mining company that has been actively exploring in Egypt since 1995. The principal asset of Centamin is its interest in the Sukari Gold Mine, located in the Eastern Desert of Egypt. Construction at the Sukari Gold Project commenced in March 2007 with the first gold bar being produced on 26 June 2009.Optimal design throughput at the Sukari Gold Mine was achieved during December 2009.

The Sukari Gold Mine is the first large-scale modern gold mine in Egypt. Centamin's operating experience in Egypt gives it a significant first-mover advantage in acquiring and developing other gold projects in the prospective Arabian-Nubian Shield.

FORWARD LOOKING STATEMENTS

Certain information contained in this report, including any information on Centamin's plans or future financial or operating performance and other statements that express management's expectations or estimates of future performance, constitute forward-looking statements. Such statements are based on a number of estimates and assumptions that, while considered reasonable by management at the time, are subject to significant business, economic and competitive uncertainties. Centamin cautions that such statements involve known and unknown risks, uncertainties and other factors that may cause the actual financial results, performance or achievements of Centamin to be materially different from the Company's estimated future results, performance or achievements expressed or implied by those forward-looking statements. These factors include the inherent risks involved in exploration and development of mineral properties, changes in economic conditions, changes in the worldwide price of gold and other key inputs, changes in mine plans and other factors, such as project execution delays, many of which are beyond the control of Centamin.

Nothing in this report should be construed as either an offer to sell or a solicitation to buy or sell Centamin securities.

ABN 86 007 700 352

Contact Information:

Josef El-Raghy

Chairman

+ 61 (8) 9316 2640 or + 203 5411 259

www.centamin.com

Buchanan Communications Limited

Bobby Morse / Katharine Sutton

+ 44 (0) 20 7466 5000