MCLEAN, VA--(Marketwired - Jun 6, 2013) - Freddie Mac (

News Facts

- Borrowers who refinanced in the first quarter of 2013 will save on net approximately $7 billion in interest over the next 12 months.

- Additionally, the net dollars of home equity converted to cash as part of a refinance, adjusted for consumer-price inflation, remained at a low volume. In the first quarter, an estimated $8.1 billion in net home equity was cashed out during the refinance of conventional prime-credit home mortgages, about the same as the previous quarter and substantially less than during the peak cash-out refinance volume of $84 billion during the second quarter of 2006.

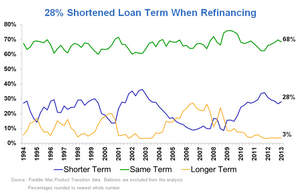

- Of borrowers who refinanced during the first quarter of 2013, 28 percent shortened their loan term, while 68 percent of borrowers kept the same term as the loan that they had paid off; 3 percent chose to lengthen their loan term. Likewise, 85 percent of those who refinanced their first-lien home mortgage maintained about the same loan amount or lowered their principal balance by paying-in additional money at the closing table. That's just shy of the 88 percent peak during the second quarter of 2012.

- More than 95 percent of refinancing borrowers chose a fixed-rate loan. Fixed-rate loans were preferred regardless of what the original loan product had been. For example, 87 percent of borrowers who had a hybrid ARM chose a fixed-rate loan during the first quarter, the highest share since the first quarter of 2010.

Property-value change, loan age, and rate reduction differed between refinancings under the Home Affordable Refinance Program (HARP) and other refinances.

- HARP has enabled many borrowers who traditionally would not have had access to refinance to obtain low rates and significantly reduce their interest rate and monthly payment. The program has helped about 2.5 million refinancing borrowers since its inception through March 2013. HARP loans made up just over 20 percent of first quarter refinance loans purchased by Freddie Mac and Fannie Mae.

- For loans refinanced during the first quarter through HARP, the median depreciation in property value was 28 percent, the prior loan had a median age of about 6 years (to be eligible for HARP, the prior loan had to be originated before June 1, 2009), and the HARP borrower with a 30-year fixed-rate refinance (no product change) had an average interest-rate reduction of 2.1 percentage points.

- For all other (non-HARP) refinances during the fourth quarter, the median property had very little change in value between the dates of placement of the old loan and the new refinance loan. The prior loan had a median age of 4.1 years, and borrowers who refinanced a 30-year fixed-rate into the same product had an average interest-rate decline of 1.6 percentage points.

Quotes

Attributed to Frank Nothaft, Freddie Mac vice president and chief economist:

"Borrowers continue to strengthen their fiscal house by taking advantage of near record low mortgage rates. In total, borrowers who refinanced in the first quarter of this year will save approximately $7 billion in interest payments over the next 12 months, which they can put towards savings, paying down debt or to support additional expenditures. Further, the estimated $8 billion in 'cash-out' activity will further augment borrowers' investment and consumption spending."

About the Quarterly Refinance Report

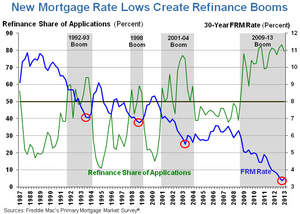

These estimates come from a sample of properties on which Freddie Mac has funded two successive conventional, first-mortgage loans, and the latest loan is for refinance rather than for purchase. The analysis does not track the use of funds made available from these refinances. The analysis also does not track loans paid off in entirety, with no new loan placed. Some loan products, such as 1-year ARMs and balloons, are based on a small number of transactions. During the first quarter of 2013, the refinance share of applications averaged 79 percent in Freddie Mac's monthly refinance survey, and the ARM share of applications was 5 percent in Freddie Mac's monthly ARM survey, which includes purchase-money as well as refinance applications.

With the report for the first quarter of 2013, the calculation of the principal balance at payoff of the previous loan has been modified. Previously, the payoff balance was calculated as the amount due based on the loan's amortization schedule, and "cash-in" was defined as a new loan amount that was less than the scheduled amortization amount. Data for 1994 to current have been recalculated using the actual payoff amount of the old loan, with an allowance for rounding down the principal at refinance; thus, from 1994 to present, "cash-in" is defined as a new loan amount that is at least $1,000 less than the payoff principal balance of the old loan. Data are presented under both methods for 1994 for comparison purposes.

Freddie Mac was established by Congress in 1970 to provide liquidity, stability and affordability to the nation's residential mortgage markets. Freddie Mac supports communities across the nation by providing mortgage capital to lenders. Today Freddie Mac is making home possible for one in four home borrowers and is one of the largest sources of financing for multifamily housing. For more information please visit www.FreddieMac.com and Twitter: @FreddieMac.

Contact Information:

MEDIA CONTACT:

Chad Wandler

703.903.2446

Chad_Wandler@freddiemac.com