MCLEAN, VA--(Marketwired - Sep 24, 2014) - Freddie Mac (

News Facts:

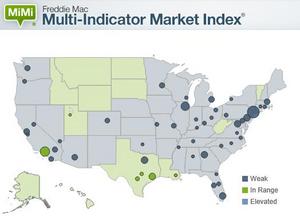

- The national MiMi value stands at 73.4, indicating a weak housing market overall and showing a slight decline (-0.45%) from June to July and a 3-month decline of (-0.98%). On a year-over-year basis, the U.S. housing market has improved (+5.39%). The nation's all-time MiMi high of 121.9 was June 2008; its low was 59.8 in September, 2011, when the housing market was at its weakest. Since that time, the housing market has made a 22.7 percent rebound.

- Thirteen of the 50 states plus the District of Columbia have MiMi values in a stable range, with North Dakota (95.9) the District of Columbia (94.4), Wyoming (91.3), Montana (89.5) and Alaska (88.4) ranking in the top five.

- Six of the 50 metro areas have MiMi values in a stable range, with San Antonio (91.3), Austin (87.5), New Orleans (83.9), Salt Lake City (83.6), and Houston (83.5) ranking in the top five.

- The most improving states month-over-month were Illinois (+0.92%), Rhode Island (+0.72%), Washington (+0.53%), Nevada (+0.38%) and Florida (+0.31%). On a year-over-year basis, the most improving states were Nevada (+20.51%), Illinois (+12.16%), Florida (+11.75%), California (9.15%) and South Carolina (+8.01%).

- The most improving metro areas month-over-month were Miami (+0.88%), Chicago (+0.64%) Las Vegas (0.62%), Providence (+0.56%) and Seattle (+0.27%). On a year-over-year basis the most improving metro areas were Las Vegas (+23.35%), Riverside, (+14.97%), Chicago (+14.73%), Miami (+13.70%) and Orlando (+11.93%).

- In July, 8 of the 50 states and 11 of the 50 metros are showing an improving three month trend. The same time last year, every state plus the District of Columbia, and every metro was showing an improving three month trend.

Quote attributable to Freddie Mac Chief Economist Frank Nothaft:

"We will continue to see 'two steps forward and one step backward' movement in our housing stability index until the broader economy sees better growth, labor markets tighten further and household formations pick-up to bring more first-time and move-up buyers into the market. The good news is overall the housing market continues to improve and is up 5 percent on a yearly basis in the latest MiMi reading."

Quote attributable to Freddie Mac Deputy Chief Economist Len Kiefer:

"We didn't notice a large decline in any one market this month, but more of softening across the board. Even the MiMi top ranked state and metro markets all saw a slight decline except for Austin. But the real drag on the most market's housing recovery continues to be the lack of purchase application activity. Even the hot housing markets in the northwest which are back in their stable range of housing activity are seeing their purchase application activity slow. The one area where momentum hasn't slowed is among the hardest hit markets. Places like Las Vegas, Miami, Chicago and Riverside, among others, are still showing double-digit yearly improvements, but that's largely a reflection of significant gains in the local employment picture as well as a real improvement in borrowers making timely mortgage payments."

MiMi monitors and measures the stability of the nation's housing market, as well as the housing markets of all 50 states, the District of Columbia, and the top 50 metro markets. MiMi combines proprietary Freddie Mac data with current local market data to assess where each single-family housing market is relative to its own long-term stable range by looking at home purchase applications, payment-to-income ratios (changes in home purchasing power based on house prices, mortgage rates and household income), proportion of on-time mortgage payments in each market, and the local employment picture. The four indicators are combined to create a composite MiMi value for each market. Monthly, MiMi uses this data to show, at a glance, where each market stands relative to its own stable range of housing activity. MiMi also indicates how each market is trending, whether it is moving closer to, or further away from, its stable range. A market can fall outside its stable range by being too weak to generate enough demand for a well-balanced housing market or by overheating to an unsustainable level of activity.

For more detail on MiMi see the FAQs. MiMi is released at 10 a.m. EDT monthly. The most current version can be found at FreddieMac.com/mimi.

Freddie Mac was established by Congress in 1970 to provide liquidity, stability and affordability to the nation's residential mortgage markets. Freddie Mac supports communities across the nation by providing mortgage capital to lenders. Today Freddie Mac is making home possible for one in four home borrowers and is one of the largest sources of financing for multifamily housing. Additional information is available at FreddieMac.com, Twitter @FreddieMac and Freddie Mac's blog FreddieMac.com/blog.