LONDON, ENGLAND--(Marketwired - Jan. 22, 2016) - Condor (AIM:CNR) ("Condor" or "the Company") is pleased to announce, further to its announcement of 20 October 2015, the full results, including Net Present Value ("NPV") and Internal Rate of Return ("IRR") figures, contained in the Whittle Consulting Limited's ("Whittle") Enterprise Optimisation study on La India Project, Nicaragua (the "Study"). The Company was in an Offer Period as defined by the Takeover Code at that point in time and was unable to publish the NPV and IRR figures derived from the independent optimisation study during the Offer Period, even though the purpose of the study was to optimise the mine schedules to NPV. One of the reasons that the Formal Sales Process was terminated on 18th January 2016 is to provide shareholders with the full details of the optimisation study. However, as the Company is now out of an Offer Period it is pleased to update investors with these improved NPV and IRR results which significantly increase the La India Project economics.

The Study involves the application of advanced analytical techniques to construct a model of the operation from the ore bodies through mining and ore treatment processes to products sold to the market with a view to maximising a project's NPV. The study used the reserves/resources and technical studies used in the NI 43-101 compliant Pre-Feasibility Study ("PFS") and Preliminary Economic Assessments ("PEA") produced by independent mineral resource and mining consultants SRK Consulting Limited ("SRK") in December 2014.

Highlights:

- NPV increases on average 56% across three production scenarios and 78% for the PFS case.

- Average NPV US$196M compared to the current market capitalisation US$12m highlights significant undervaluation with a price-to-book ratio 0.06 times

- IRR averages 30% across three production scenarios

- 29% increase to 866k oz gold from 674k oz gold of contained gold of Indicated ounces only in the base case La India open pit, as the pit pushes deeper

- 29% increase to 1,066k oz gold from 827k oz gold contained gold of Indicated and Inferred ounces within La India open pit + two feeder pits

- 18% increase to 1,544k oz gold from 1,313 oz gold of contained gold of Indicated and Inferred within all pits and underground

- 22% increase in average gold production for the first 5 years, ranging from 91,000 oz to 165,000 oz gold per annum across three production scenarios

- The recovered gold over life of mine ranges from 796,000 oz to 1,437,000 oz gold across the 3 production scenarios

- All in sustaining cash costs remain under US$700 per oz gold for all production scenarios

Mark Child CEO comments:

"We are very pleased to now be able to release the materially improved NPV and IRR figures contained within the optimisation study. The NPV of the PFS case of Indicated ounces gold only, increased 78%. The average NPV increases 56% for three production scenarios compared to the production scenarios within the PFS and PEAs announced in December 2014. The average NPV is US$196M compared to the current market capitalisation of US$12M, valuing the Company at a price-to-book ratio of 0.06 times, highlighting the material undervaluation of the Company's shares. The IRRs increase to an average of 30%. Indicated ounces of gold within the main La India open pit increase by 29% to 866k oz gold and also by 29% for the main pit + feeder pits to 1,066k oz gold as the pit pushed deeper. The annual gold production for the first 5 years increases on average 22% and ranges from 91,000 oz gold to 165,000 oz gold per annum versus the PFS and PEA studies. The recovered gold over life of mine ranges from 796,000 oz to 1,437,000 oz gold. The average pay back of upfront capital costs is between two and three production years highlighting the outstanding economics and versatility of La India Project."

Background

Whittle Consulting's (WCL) Enterprise Optimisation is an integrated approach to maximising the Net Present Value (NPV) of a mining business by simultaneously optimizing 10 different mechanisms across the mining value chain. Condor commissioned the independent optimisation study in May 2015 to investigate strategic options to improve project economics. The Study is a strategic planning tool and is not NI 43-101 compliant. However, WCL is the recognised world leader in a specialist field of maximising the economics of a mine and has completed work for major mining companies: Rio Tinto, Anglo American, Kinross, AngloGold Ashanti, Barrick, Xstrata, Vale. The report presents the findings from the Enterprise Optimisation Study for La India Project. An oil price of US$100 was used in the PFS and PEAs.

Four production scenarios were assessed, based on the study methodology employed by SRK and Condor.

- The PFS case includes measured and indicated material only from the La India open pit, with a processing capacity of 0.8 million tonnes per annum (mtpa) or 2,200 tonnes per day (tpd).

- The PEA 1.0 case also includes the La India open pit inferred material, with a process capacity of 1.0 mtpa or 2,800tpd

- The PEA 1.2 case includes all of the La India open pit material, and also includes material from two nearby smaller pits, America and Central Breccia. The processing capacity for this case is 1.2 mtpa or 3,300tpd. This is known as scenario "A" in the SRK reports.

- The PEA 1.6 case adds underground mining from La India and America, over and above the material in PEA 1.2. The processing capacity for this case is 1.6 mtpa or 4,400tpd. This is known as scenario "B" in the SRK reports.

Validation runs for each case were produced. Optimised runs were generated using multi-mine scheduling, fully variable cut-off grade and stockpiling. Reduced capacity cases were run, also optimised for schedule, cut-off grade and stockpiling. Grind-throughput-recovery relationships were developed for the La India open pit material, and this methodology was used to further optimize the schedule for all cases. Pit and Phase optimisation was completed on the La India pit using the Enterprise Optimisation economics, which improved NPV.

The optimised cases were developed from work done from May 2015 through to September 2015. The gold price for this work is $1,250 per troy ounce, and the silver price is $19.75/troz in order to have a like for like comparison with the PFS and PEAs. Metal recoveries were based on the PFS and PEA work completed in late 2014.

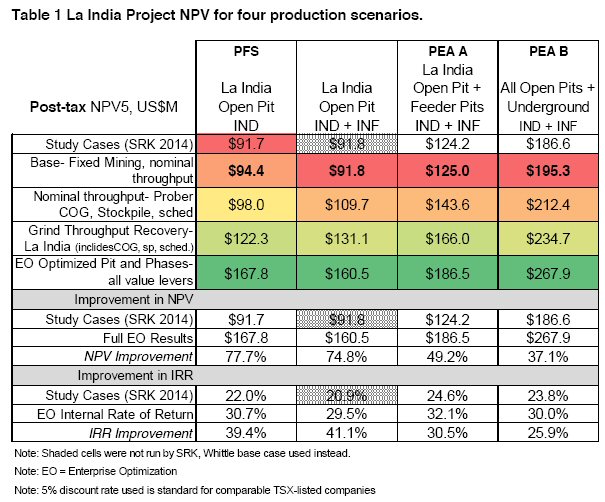

Post-tax results are indicated in Table 1 for the four production scenarios. The Enterprise Optimisation methodology improved NPV in all cases, with decreasing improvements across the larger plant / open pit scenarios. This is due to the Grind-Throughput-recovery (GTR) work being isolated to La India Vein Set only due to limited metallurgical data on the America and Central Breccia. Similar results may be recognized when data is collected and assessed for the America and Central Breccia open pit and underground material. It is important to note that the 1.0 mtpa case does not have a PFS/PEA study equivalent, nor corresponding pit designs, so there is no comparison data. In these cases, improvements are measured against the initial Enterprise Optimisation calibration runs.

To view Table 1, please visit the following link: http://media3.marketwire.com/docs/cnr0122table1.jpg.

{kind=link}

Table 2. Comparison of production scenarios to PFS and PEAs

| La India - PFS Open Pit - PFS IND Only |

La India Open Pit IND+INF |

All Open Pits PEA-A IND+INF |

All Open Pits + UG PEA-B IND+INF |

|||||||

| PFS | Whittle EO |

Whittle EO |

PEA A | Whittle EO |

PEA A | Whittle EO |

||||

| Nominal Processing Plant capacity tpd | 2,200 | 2,800 | 3,300 | 4,400 | ||||||

| Nom. Capacity in M-tpa | 0.8 | 1.0 | 1.2 | 1.6 | ||||||

| Contained gold koz | 674 | 866 | 955 | 827 | 1,066 | 1,313 | 1,554 | |||

| Recovered gold koz | 614 | 796 | 882 | 752 | 985 | 1,203 | 1,437 | |||

| 1st 5 years avg. production gold p.a. koz | 76 | 91 | 101 | 94 | 118 | 138 | 165 | |||

| Production improvement 1st 5 years | 20 | % | n/a | 25 | % | 20 | % | |||

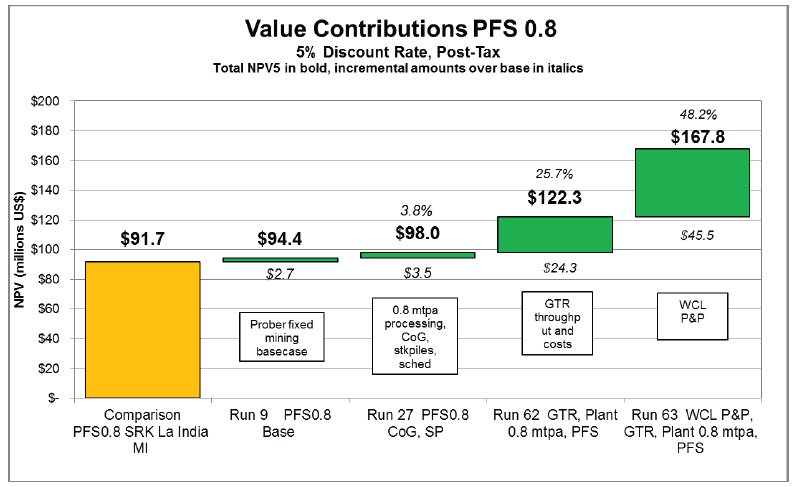

Figure 1 presents a waterfall summary of the value contributions for the PFS 0.8 ktpa / 2200 tpd case. The initial optimised schedule, utilizing fully variable cut-off grade and a maximum of 1.5 mt of stockpiling, adds 3.8% to the base NPV. The grind-throughput-recovery methodology improves NPV by another 25.7% over the prior case due to faster/coarser grinding and reduced costs. The Enterprise Optimisation net value economics generate a larger pit and higher early value phases, improving NPV by an additional 48.2%. This exercise did generate a larger pit with more ounces - it should be stressed that this is not at a PFS level of study. The overall value improvement in the PFS 0.8 case with the Enterprise Optimisation methodology is 78% at a gold price of US$1,250. The bold numbers in the graph are the total NPV at 5%, and the italicized numbers are the increment value and percent change over the base.

To view Figure 1 - La India PFS Value Contributions, please visit the following link: http://media3.marketwire.com/docs/cnr0122fig1.jpg.

{kind=link}

Figure 2 provides a similar presentation of the value contributions for the PEA 1.2 "A" case, which includes all Measured, Indicated &Inferred material from all three pits, with a nominal processing capacity of 1.2 mtpa (3300 tpd). There are two cut-off grade and stockpile optimised Prober schedules for reduced processing rates presented in this graph, both of which exceed the initial study NPV. The run at the nominal throughput of 1.2 mtpa has a better NPV than the 1.0 mtpa case, but only by about 1%, which may mean that the optimal processing capacity for this case may be less than the nominal 1.2mpta level. Cut-off grade and stockpiling improves NPV by 13% over the base, and GTR adds 17.9% to the NPV. The Enterprise Optimisation-generated pit and phase optimisation added 16.4% over the base. Overall, the Enterprise Optimisation methodology improved NPV for the PEA "A" 1.2 case by over 50%.

To view Figure 2 - La India PEA 1.2 "A" Value Contributions, please visit the following link: http://media3.marketwire.com/docs/cnr0122fig2.jpg.

{kind=link}

Figure 3 presents the value contributions for the PEA 1.6 "B" case. This case has all of the open pit material available, plus a conceptual view of underground resource from the La India and America deposits, with a nominal processing capacity of 1.6 mtpa / 4400 tpd.

For the PEA 1.6 "B" case, the reduced processing runs all have increasing values commensurate with increasing processing rates, meaning that the mine fleet size is not a mismatch for the higher production cases. However, it may be the mining fleet is over-sized for the lower production rates, which, if recapitalized, could improve NPVs for the lower production cases. This was not tested in this study, since contractor mining is the baseline assumption.

The cut-off grade and stockpile schedule improves NPV by 17.6% over the base, and the GTR case adds 2.6%. The GTR approach had less impact in this case as only the La India material has sufficient information for GTR analysis. With the addition of the Central Breccia (CBZ) material, the America pit material, and the higher grade underground material, there is proportionally less material eligible for this methodology. The Enterprise Optimised economics-base pit and phase optimisation generated significant value for the PEA 1.6 "B" case, 17% over the base. The total value gain for the PEA 1.6 "B" case is 40% over the base.

To view Figure 3 - PEA 1.6 "B" Value Contributions, please visit the following link: http://media3.marketwire.com/docs/cnr0122fig3.jpg.

{kind=link}

Outcomes

This Enterprise Optimisation Study developed the NPV-optimised schedules through variable cut-off grade, stockpile capacity, grind-throughput-recovery, multi-mine scheduling, and optimised pit and phasing. Significant outcomes of this process include:

- An optimised schedule utilizing fully variable cut-off grade with stockpiling adds significantly to the project NPV in all cases.

- The permitted maximum stockpile capacity of 1.5Mt should be utilized, and additional stockpile capacity may add value.

- The grind size-throughput-recovery (GTR) methodology adds significant value to the project in all cases where it can be utilized.

- Modification of the ultimate pit and phase selection based on the methodology presented here increases NPV significantly in all cases, partially due to incorporating additional tonnes and ounces.

- The theory of constraints indicates using US Dollar per kilowatt hour as the limiting factor in the business system will improve value. The Enterprise Optimised pit and phase optimisation based on this, combined with cut-off and GTR optimisation adds significantly to project NPV.

- When additional mining material is added, processing capacity may not necessarily need to be increased, and may not yield the optimal NPV.

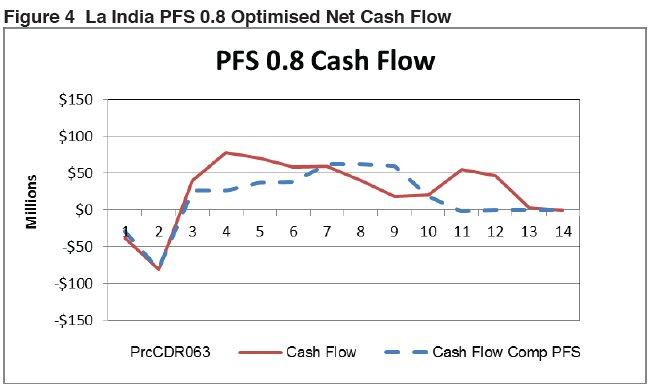

The Enterprise Optimisation methodology as applied in this study was able to pull cash flow forward as indicated in Figure 4 through Figure 6. These three figures represent the PFS 0.8 mtpa case, the PEA 1.2 mtpa case, and the PEA 1.6 mtpa case.

To view Figure 4 - La India PFS 0.8 Optimised Net Cash Flow, please visit the following link: http://media3.marketwire.com/docs/cnr0122fig4.jpg.

{kind=link}

To view Figure 5 - La India, America, CBZ PEA 1.2 Net Cash Flow, please visit the following link: http://media3.marketwire.com/docs/cnr0122fig5.jpg.

{kind=link}

To view Figure 6 - La India, America, CBZ, Underground PEA 1.6 Net Cash Flow, please visit the following link: http://media3.marketwire.com/docs/cnr0122fig6.jpg.

{kind=link}

Conclusion

Overall, the independent optimisation analysis conducted by WCL clearly demonstrates the potential to unlock substantial additional value from the La India Project. Across 3 production scenarios, NPV increases over 50%, IRRs average 30%, the payback on upfront capital costs is between two to three production years, and gold production increases on average 22% for the first 5 years. WCL's study is a strategic planning tool, which is used to maximise the economics, particularly the NPV, ahead of a "build decision" and can often form part of a more detailed Definitive/Bankable Feasibility Study. It should be noted that WCL's study is not NI 43-101 compliant and would require re-generation of the PFS and PEAs to confirm the improvements. Phase 2 of the study will consist of optimisation of the underground potential for the project, as well as sensitivities to accommodate the impact of lower metal and oil prices.

Whittle Consulting Limited

Whittle Consulting's (www.whittleconsulting.com.au) approach to Enterprise Optimisation involves the application of advanced analytical techniques to construct a model of the operation from the ore bodies through mining and ore treatment processes to products sold to the market. Once modelled, a powerful mathematical optimiser is applied to manipulate the variables which are regarded as "negotiable", to develop long-term plans that excel in terms of a wide range of economic and other operational and business criteria.

Modelling techniques and facilities are comprehensive, capturing and harnessing the client's information on geology, geotechnical, mining engineering, process engineering and metallurgy, finance and marketing, to combine into an integrated Enterprise Optimisation Model that contains the details of all development options under consideration. The model is used to direct underground mine design or as a basis for pit and phase optimisation and to develop life-of-mine business plans which identify the optimal operating configuration for the scenario presented. The result is a unique capability that can resolve planning issues beyond the scope of available packaged planning software and conventional techniques.

It is common for Whittle Consulting to interface with diverse commercial and in-house software packages during an Enterprise Optimisation exercise. These may be limited to mine planning and scheduling packages or financial reporting, or may for example already incorporate 2 or 3 of the twelve Enterprise Optimisation steps or could even utilise highly technical plant optimisation routines. It is typical for the Enterprise Optimisation work to use the output of any of these packages as input to overall optimisation of an operation or project. The Enterprise Optimisation results provide conceptual guidance for the detailed operational plans which will be developed by the client or their engineering and cost study consultants in most cases using their existing software.

All the mechanisms required for this study have been implemented before - most of them on a routine basis.

Whittle's Enterprise Optimisation study on Condor was prepared by Richard Peevers (B.A. (Geology), MBA (Finance), M.Eng. (Civil), Registered Professional Civil Engineer California). Richard holds degrees in geology, engineering, and business administration and has managed copper, gold, borate, and nickel optimisation studies for Whittle Consulting.

Competent Person's Declaration

Information in this announcement that relates to the project evaluation, Preliminary Feasibility Study, engineering and mine planning is based on information compiled and/or reviewed by Gerald David Crawford, the Chief Operating Officer, who is a Registered Professional Engineer in the states of Colorado and Nevada and member of the Society of Mining, Metallurgy and Exploration, and a mining engineer with 38 years of experience in the design and evaluation of precious and base metal mineral resources. Mr. Crawford is a full-time employee of Condor Gold plc and has sufficient experience which is relevant to the mining method and type of deposit under consideration, and to the type of activity which he is undertaking to qualify as a Qualified Person as defined under Canadian NI 43-101. Mr. Crawford consents to the inclusion in the announcement of the matters based on their information in the form and context in which it appears and confirms that this information is accurate and not false or misleading.

Technical Glossary

| $/kWhr | Dollars per kilowatt-hour, one means of optimizing mill throughput. Mills are frequently a bottleneck / constraint in improvement of net present value | |

| CBZ | Central Breccia deposit, a near surface inferred resource located bout 2km to the northeast of the La India Pit | |

| CDR | Whittle's abbreviation for the Condor project | |

| COG | Cut-off Grade - a grade of gold in ore that segregates ore from waste or stockpile material. One of the variables that Prober manipulates to improve NPV | |

| Constraint | A term from Linear Programming, any attribute of a cash flow and operating cost model that serves to limit increases in the net present value of the system | |

| Enterprise Optimisation | Enterprise Optimisation - Whittle terminology for 'Whole Mine' optimisation | |

| GTR | Grind-Throughput-Recovery - Prober optimisation of the grind size, gold recovery and mill throughput variables in the EO process | |

| LP | Linear Programming - A mathematical technique used to optimize a process subject to a set of constraints | |

| mtpa | Million tonnes per annum (metric tonnes) | |

| NPV | Net Present Value - standard financial tool for determining the present value of a series of cash flows in the future at a given discount rate. Unless otherwise noted, the discount rate in the Whittle study is 5%. NPV is the basis by which Prober decides the 'best' option. | |

| P&P | Pit and Phase - Whittle optimisation of the ultimate pit shell and all contained phases to achieve maximum NPV using EO net value economics | |

| PEA | Preliminary Economic Assessment - A conceptual-level study used to demonstrate basic economic viability under Canadian National Instrument 43-101 | |

| PFS | Preliminary Feasibility Study - Overall economic accuracy of +/- 25% | |

| Prober | The proprietary software package used by Whittle Consulting Ltd. to implement Enterprise Optimisation | |

| Stockpile | A means of controlling the grade of material sent through the mill, whereby higher grades are given preferential treatment, particularly when a surplus of ore is available within any mining period. | |

| Theory of Constraints | All production processes are limited by any number of factors, such as advance rate within the mine, truck capacity, or power that can be applied through the SAG mill (for example). Prober uses these constraints to eliminate unworkable scenarios, solving for the maximum NPV achievable within the constraints | |

| tr.oz | Troy Ounce, standard transaction unit for gold and silver sales, at 31.1031 grams per troy ounce. | |

| UG | Underground Mining | |

| Validation Run | The initial test of the Whittle cash flow model and fixed-mining Prober run that ensures that pre-optimisation economics calculated by Whittle agree with existing PFS and PEA results |

For further information please visit www.condorgold.com.

About Condor Gold plc:

Condor Gold plc was admitted to AIM on 31st May 2006. The Company is a gold exploration and development company with a focus on Central America.

Condor completed a Pre-Feasibility Study (PFS) and two Preliminary Economic Assessments (PEA) on La India Project in Nicaragua in December 2014. The PFS details an open pit gold mineral reserve of 6.9M tonnes at 3.0g/t gold for 675,000 oz gold producing 80,000 oz gold p.a. for 7 years. The PEA for the open pit only scenario details 100,000 oz gold production p.a. for 8 years whereas the PEA for a combination of open pit and underground details 140,000 oz gold production p.a. for 8 years. La India Project contains a total attributable mineral resource of 18.4Mt at 3.9g/t for 2.33M oz gold and 2.68M oz silver at 6.2g/t to the CIM Code.

In El Salvador, Condor has an attributable 1,004,000 oz gold equivalent at 2.6g/t JORC compliant resource. The resource calculations are compiled by independent geologists SRK Consulting (UK) Limited for Nicaragua and Ravensgate and Geosure for El Salvador.

Consent by Whittle Consulting

Whittle Consulting hereby accepts responsibility for the accuracy of the NPV and IRR calculations based on the data and assumptions provided by Condor and SRK, extracted from the Enterprise Optimisation study prepared for the Company dated September 2015 as contained in this announcement. Furthermore, Whittle Consulting consents to the use of its name in this announcement.

Disclaimer

Neither the contents of the Company's website nor the contents of any website accessible from hyperlinks on the Company's website (or any other website) is incorporated into, or forms part of, this announcement.

Whittle Consulting is acting exclusively for Condor Gold plc and no one else in connection with the Enterprise Optimisation study and will not be responsible to anyone other than Condor Gold plc for providing the protections afforded to clients of Whittle Consulting. Neither Whittle Consulting nor any of its affiliates owes or accepts any duty, liability or responsibility whatsoever (whether direct or indirect, whether in contract, in tort, under statute or otherwise) to any person who is not a client of Whittle Consulting in connection with this Announcement, any statement contained herein, or otherwise.

Contact Information:

Mark Child

Executive Chairman and CEO

+44 (0) 20 7408 1067

www.condorgold.com

Beaumont Cornish Limited

Roland Cornish and James Biddle

+44 (0) 20 7628 3396

Numis Securities Limited

John Prior and James Black

+44 (0) 20 72601000

Farm Street Media

Simon Robinson

+44 (0) 7593 340107