LONDON, UNITED KINGDOM and BOSTON, MA--(Marketwired - Nov 3, 2016) - Investors who picked emerging markets stocks based on their environmental, social and governmental (ESG) rating potentially outperformed those that ignored them, according to a new report by global investment firm Cambridge Associates, The Value of ESG Data: Early Evidence for Emerging Markets Equities.

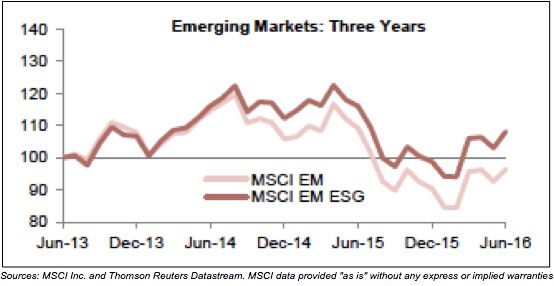

The analysis found that over the past three years -- when the MSCI Emerging Markets ESG Index outperformed its parent index, the MSCI Emerging Markets Index, by a cumulative 12 percent on a total return US dollar basis -- more than 50 percent of the outperformance was attributable to ESG factors alone. Analysis of all the emerging markets ESG data that was available for the preceding six and half years broadly supported this finding.

According to MSCI guidelines, there are nearly 40 different types of ESG factors. Those under "environmental" include carbon emissions, toxic waste, and opportunities such as green buildings and renewable energy. Those under "social," the largest of the three categories, include health and safety for employees, product safety and quality, controversial sourcing and opportunities such as access to finance. Under "governance," factors include business ethics and anti-competitive practices.

Chris Varco, Senior Investment Director for Mission-Related Investing at Cambridge Associates and author of the report, said: "Using these criteria to help pick stocks in emerging markets really helps to separate the wheat from the chaff. Of the 367 basis points of annualised outperformance achieved by the MSCI Emerging Markets ESG Index, some 199 basis points were attributable to ESG factors after we accounted for the contribution of other factors such as country, currency, sector and style."

Varco continued: "This is particularly important because ESG factors typically tilt towards equity styles that have recently outperformed, for example, quality-focused growth. Our study therefore refutes the assertion that ESG factors are just proxies for other things, rather than valuable investment tools in their own right."

Cambridge Associates conducted an attribution analysis to determine the unique contribution of ESG selection. The other factors were significantly smaller contributors to the outperformance than ESG considerations: sector (107 basis points), style (63 basis points), and currency (4 basis points). The country factor was a detractor, reducing the ESG version's outperformance by 5 basis points.

The three-year period under review ran from June 2013, when the MSCI Emerging Markets ESG Index was launched. The Value of ESG Data report from Cambridge Associates looked further back at older data from January 2007 up to the index launch, and found that ESG ratings were a strong source of stock-specific outperformance during most of this earlier six and a half year period as well.

Why ESG Factors Matter in the Emerging Markets

Many investors are overlooking the value of ESG factors -- in effect, ignoring the stream of new data that has become available over the past five years, according to Varco.

"ESG data should be a key tool for investors in the emerging markets," said Varco. "When making investment decisions, investors in emerging markets equities often focus on commodity prices, currency, and macroeconomic factors, as well as domestic consumption trends, and they tend to underestimate the value of this widely available information on the ESG strength of companies in emerging markets."

Varco also attributed the success of the MSCI Emerging Markets ESG Index to the avoidance of state-owned enterprises (SOEs), which feature prominently in the parent MSCI Emerging Markets Index. "SOEs are influenced by interests beyond generating profits for shareholders, which can negatively impact operational aspects of the business," he said. "The same accusation has been made for some family-owned businesses, which are also common in emerging markets."

Cambridge Associates found that there were 13 SOEs among the 40 largest companies in the parent MSCI Emerging Markets Index during the last three years. Of those 13, the MSCI Emerging Markets ESG Index had a zero weighting in 11 of them. In the two companies where the MSCI Emerging Markets ESG Index was overweight relative to the parent index, Cambridge Associates concluded that "this was a poor decision, as both detracted from relative performance on a stock-specific basis."

Active Management and ESG Stocks

There are few dedicated active ESG funds focusing on the emerging markets -- but this is set to change. Noelle Laing, Managing Director for MRI Research at Cambridge Associates, said: "As a result of growing demand from investors, we have been consulting on and facilitating the creation of several emerging market ESG funds which integrate consideration of ESG factors in a meaningful way."

Laing added: "Even beyond the actively-managed funds that outperformed the MSCI Emerging Markets Index since their inception, a growing number of mainstream asset managers are placing more emphasis on ESG factors of the companies they analyse, even if their products do not necessarily have a defined ESG label."

ESG Factors Should Be Used in a "Nuanced Way" in Developed Markets

While ESG factors have a clear value for investors in emerging markets, their value for investors in developed markets is less clear. Cambridge Associates found that for the nearly six-year period that could be examined for developed markets, the MSCI World ESG Index slightly underperformed the MSCI World Index, its parent index, by 10 basis points. Further analysis found that ESG factors negatively impacted the performance of the MSCI World Index, detracting 54 basis points from the excess return on an annualised basis. The key observation is that ESG-based stock selection added value outside the United States, but struggled with stock selection in this market.

Explaining this, Varco said: "Some mega-cap US companies that performed well in recent years were excluded from the ESG index, significantly harming relative performance." He cited four stocks -- Amazon, Apple, Facebook, and Home Depot -- which were completely excluded from the ESG index during the entire three-year period.

Cambridge Associates found that ESG data could be valuable in developed markets if used in a nuanced way. Unlike the MSCI World ESG Index, many active managers integrating ESG analysis alongside financial analysis have outperformed MSCI World in recent years.

For more information, or to speak with Chris Varco or Noelle Laing, please contact Eric Mosher, Sommerfield Communications, Inc., at +1 (212) 255-8386 / Eric@sommerfield.com.

About Cambridge Associates

Cambridge Associates is a global investment firm founded in 1973 that builds customised investment portfolios for institutional investors and private clients around the world. Working alongside its early clients, among them several leading universities, the firm pioneered the strategy of high equity orientation and broad diversification, which since the 1980s has been a primary driver of performance for these leading fiduciary investors. Cambridge Associates serves over 1,100 global investors -- primarily foundations and endowments, pensions and family offices -- and delivers a range of services, including outsourced investment (OCIO) solutions, traditional consulting services, and access to research and tools across global asset classes. Cambridge Associates has more than 1,300 employees -- including over 150 research staff -- serving its client base globally. The firm maintains offices in Arlington, VA; Boston; Dallas; Menlo Park and San Francisco, CA; London; Singapore; Sydney; and Beijing. Cambridge Associates consists of five global investment consulting affiliates that are all under common ownership and control. For more information about Cambridge Associates, please visit www.cambridgeassociates.com.

This press release is provided for informational purposes only and is not intended to be investment advice. Any references to specific investments are for illustrative purposes only. The information herein does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. This release is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction. Past performance is not a guarantee of future returns. Broad-based securities indices are unmanaged and are not subject to fees and expenses typically associated with managed accounts or investment funds. Investments cannot be made directly in an index.

Copyright © Cambridge Associates Limited 2016. All rights reserved.

Contact Information:

Media Contact:

Eric Mosher

Sommerfield Communications, Inc.

212-255-8386

eric@sommerfield.com