New York, Jan. 24, 2024 (GLOBE NEWSWIRE) -- According to Market.us latest industry analysis, The global data center construction market size is expected to be worth around USD 453.5 Billion by 2033, from USD 237.1 Billion in 2023, growing at a CAGR of 6.7% during the forecast period from 2024 to 2033.

The Data Center Construction Market is becoming increasingly vital across various industries, highlighting the growing reliance on big data, cloud computing, and the Internet of Things (IoT). As businesses across sectors such as healthcare, finance, and technology continue to generate vast amounts of data, the need for efficient, reliable, and scalable data storage solutions becomes paramount. This surge in data generation and storage needs is driving the expansion of the Data Center Construction Market, making it a critical component in the infrastructure of modern digital economies.

The growing importance of data centers has opened up opportunities for new entrants in the market. The rising demand for data center construction has created a favorable environment for companies and startups looking to establish their presence in the industry. As existing data centers reach their capacity limits and new projects are initiated to meet the growing demand, there is a need for skilled professionals, innovative technologies, and specialized services.

To gain greater insights, Request a sample report @ https://market.us/report/data-center-construction-market/request-sample/

New entrants in the data center construction market have the opportunity to provide cutting-edge solutions and cater to the evolving needs of businesses. They can introduce advanced construction techniques, energy-efficient designs, and innovative cooling systems that address the challenges of sustainability, scalability, and cost-effectiveness. Moreover, the emergence of modular data center construction methods has further opened avenues for new players to enter the market with flexible and scalable solutions.

The rising demand for data centers, driven by trends such as digital transformation, IoT, artificial intelligence, and big data analytics, offers immense potential for growth. New entrants can capitalize on this demand by offering customized and tailored solutions that align with the specific requirements of industries, including finance, healthcare, e-commerce, and telecommunications.

Important Revelation:

- The global data center construction market is projected to reach a valuation of USD 453.5 Billion by 2033, with a Compound Annual Growth Rate (CAGR) of 6.7%. This represents significant growth, considering it was USD 237.1 Billion in 2023.

- In 2023, Colocation Data Centers held a dominant market share of over 46%, followed by Enterprise Data Centers and Hyperscale Data Centers.

- Tier III data centers captured more than 41% of the market in 2023, offering a balance of affordability and reliability. Tier I, Tier II, and Tier IV data centers serve specific market needs.

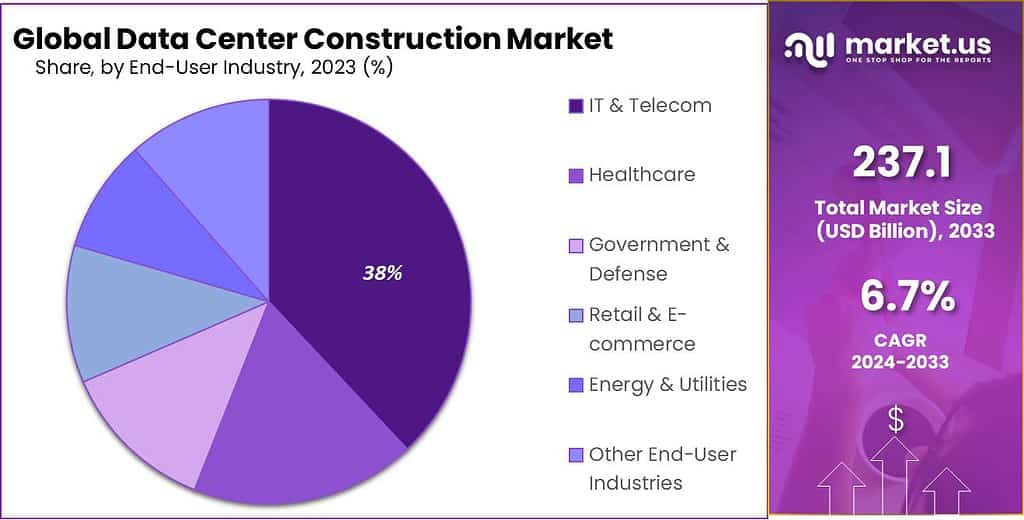

- The IT & Telecom sector led in 2023, accounting for over 38% of the market. Healthcare, Government & Defense, Retail & E-commerce, Energy & Utilities, and other industries are also driving growth.

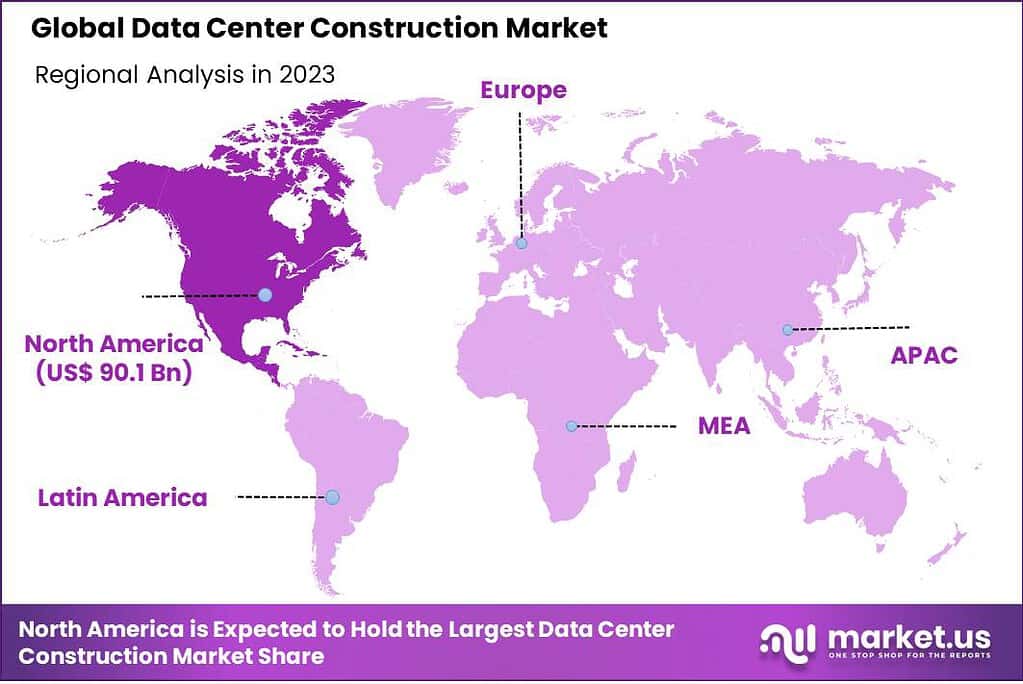

- In 2023, North America dominated with over 38% market share, followed by Europe, Asia-Pacific, Latin America, and the Middle East & Africa.

- Biggest players in data center construction include Turner Construction Company, Holder Construction Group, DPR Construction, Skanska AB, Mortenson Construction, AECOM, Jacobs Engineering Group, and others.

Buy Now this Premium Report to Grow your Business: https://market.us/purchase-report/?report_id=15340

Recent Developments

- In 2023, Skanska AB: Investments in digitalization: Implemented advanced technologies like BIM and 3D modeling for efficient data center construction.

- In 2023, Mortenson Construction: Built several large-scale data centers for major cloud providers like Amazon Web Services and Microsoft Azure.

Factors Affecting the Growth of the Global Data Center Construction Market

- Technological Advancements: The rapid evolution in technology, particularly in cloud computing, Big Data analytics, and the Internet of Things (IoT), has significantly increased the demand for data storage and processing capabilities. This has led to a surge in the construction of data centers equipped with advanced infrastructure to handle vast amounts of data efficiently.

- Increasing Data Consumption and Digital Transformation: With the digitalization of businesses and the growing reliance on online services, there is an escalated need for data storage and processing facilities. The proliferation of streaming services, remote work, e-commerce, and social media platforms contributes to this increased demand, necessitating the expansion of data center capacities.

- Governmental Policies and Regulations: Government regulations regarding data sovereignty, privacy, and security influence the data center market. Policies mandating local data storage can drive the construction of new data centers in specific regions. Additionally, compliance with international standards for data security and privacy, like the General Data Protection Regulation (GDPR) in Europe, can also impact market growth.

- Environmental Considerations: There is a growing focus on building energy-efficient and sustainable data centers due to concerns over high energy consumption and carbon footprint. This has led to the adoption of green data center technologies, use of renewable energy sources, and innovative cooling systems, which can influence construction costs and design.

- Economic Factors: The economic stability of a region can impact investment in data center construction. Regions with strong economic growth are more likely to see increased investment in data infrastructure.

- Geographical Factors: The location of a data center is crucial, as it needs to balance factors like climate (to reduce cooling costs), proximity to users (to reduce latency), risk of natural disasters, and availability of skilled labor.

Are you a start-up willing to make it big in the business? Grab an exclusive sample of this report here

Report Segmentation of Data Center Construction Market

Type Analysis

In 2023, the Colocation Data Centers segment held a dominant market position, capturing more than a 46% share in the global data center construction market. This significant market share can be attributed to several key factors. Primarily, colocation data centers offer a cost-effective solution for businesses by enabling them to rent space for servers and other computing hardware, thereby avoiding the high capital expenditures associated with building and maintaining their own data center facilities. This model is particularly appealing to small and medium-sized enterprises (SMEs) that require robust IT infrastructure without the associated high costs.

Another factor contributing to the dominance of colocation data centers is their ability to provide scalability and flexibility. Businesses can easily scale their IT infrastructure up or down, depending on their evolving needs, without investing in physical space and infrastructure. This flexibility is vital in today's rapidly changing technology landscape.

Furthermore, colocation data centers often provide enhanced security, connectivity, and professional management, which are crucial for businesses prioritizing data security and uptime. By outsourcing data center needs to colocation facilities, companies benefit from advanced security measures, including physical security, cybersecurity protocols, and redundancy systems, ensuring minimal downtime and data loss.

Tier Type Analysis

In 2023, the Tier III segment held a dominant market position in the data center construction market, capturing more than a 41% share. This notable dominance can be attributed to the balanced blend of cost-efficiency and reliability that Tier III data centers offer. Unlike Tier I and Tier II facilities, Tier III data centers provide a significant upgrade in terms of uptime and redundancy. They are designed to ensure that any component can be replaced or maintained without disrupting operations, making them highly attractive for businesses that require high availability but must also manage costs effectively.

Further driving the growth of the Tier III segment is the increasing adoption of cloud services and big data analytics by small and medium-sized enterprises (SMEs). These enterprises are typically looking for data centers that offer a higher level of reliability than Tier II, but do not require the extremely high levels of fault tolerance found in Tier IV. The moderate investment and operational costs associated with Tier III data centers make them a pragmatic and popular choice in the rapidly evolving digital landscape, where downtime can result in significant financial and reputational losses.

End-User Industry

In 2023, the IT & Telecom segment held a dominant market position in the data center construction market, capturing more than a 38% share. This substantial market share can be primarily attributed to the escalating demand for data processing and storage solutions driven by the proliferation of digital communication and the expansion of telecommunications infrastructure globally. The IT & Telecom industry, being at the forefront of digital transformation, necessitates robust, scalable, and secure data centers to manage the vast volumes of data generated and to support the increasing reliance on cloud computing and IoT (Internet of Things) technologies.

The surge in mobile data traffic, the rollout of 5G networks, and the growing adoption of smart devices have further intensified the need for advanced data center infrastructures in this sector. These data centers are integral to ensuring seamless connectivity, high-speed data transmission, and uninterrupted service delivery, which are critical in the IT & Telecom industry. Furthermore, the adoption of big data analytics, AI (Artificial Intelligence), and machine learning applications in telecommunications operations is driving the demand for more sophisticated data processing capabilities, which in turn fuels the growth of the data center construction market in this segment.

Get a Complete and Professional sample PDF @ https://market.us/report/data-center-construction-market/request-sample/

Competitive Landscape

The competitive landscape of the market has also been examined in this report. Some of the major players include:

- Turner Construction Company

- Holder Construction Group

- DPR Construction

- Skanska AB

- Mortenson Construction

- AECOM

- Jacobs Engineering Group

- M. A. Mortenson Company

- Hensel Phelps Construction Co.

- Holder Construction Company

- Other Key Players

Scope of the Report

| Report Attributes | Details |

| Market Value (2023) | US$ 237.1 Billion |

| Forecast Revenue 2033 | US$ 453.5 Billion |

| CAGR (2024 to 2033) | 6.7% |

| North America Revenue Share | 38% |

| Base Year | 2023 |

| Historic Period | 2018 to 2022 |

| Forecast Year | 2024 to 2033 |

Key Market Segments

Type

- Enterprise Data Centers

- Colocation Data Centers

- Hyperscale Data Centers

Tier Type

- Tier I

- Tier II

- Tier III

- Tier IV

End-User Industry

- IT & Telecom

- Healthcare

- Government & Defense

- Retail & E-commerce

- Energy & Utilities

- Other End-User Industries

Impactful Driver

The most impactful driver in the data center construction market is the escalating demand for cloud services. This surge is primarily due to the increasing reliance of businesses on cloud computing for data storage, management, and processing. As enterprises continue to adopt cloud-based solutions for scalability, flexibility, and cost-efficiency, the need for robust data center infrastructure becomes critical. This shift is further accelerated by the rapid growth of data generated from various digital platforms, Internet of Things (IoT) devices, and big data analytics, necessitating significant expansion in data center capacities.

Key Trend

A key trend in the data center construction market is the growing emphasis on sustainable and energy-efficient data center designs. With rising concerns about the environmental impact of data centers, which are significant consumers of electricity and resources, there is a notable shift towards green data centers. These facilities are designed to minimize energy consumption and reduce carbon footprints, utilizing renewable energy sources, advanced cooling systems, and energy-efficient building materials. This trend is not only environmentally responsible but also cost-effective in the long run, as it leads to lower operational expenses.

Major Challenges

One of the major challenges facing the data center construction market is the increasing complexity and cost of building state-of-the-art data centers. The need for advanced security measures, high-speed connectivity, and scalable infrastructure adds to the complexity of data center construction. Additionally, adhering to various regulatory compliances and data protection laws, especially in regions with strict data sovereignty requirements, poses significant challenges.

Another notable challenge is the limited availability of skilled professionals in the field of data center construction and management. This skill gap can lead to project delays and increased costs. Furthermore, the rising prices of raw materials and land, along with the logistical challenges associated with sourcing and transporting these materials, especially in less accessible regions, also present considerable hurdles in the development of new data center facilities.

Download Latest Analysis Sample PDF (Including Full Table of contents, List of Tables & Figures, Chart): https://market.us/report/data-center-construction-market/request-sample/

Regional Analysis

In 2023, North America held a dominant market position in the data center construction market, capturing more than a 38% share. This prominence can be attributed to the region's advanced technological infrastructure, high concentration of global technology companies, and significant investments in cloud services and big data analytics. The United States and Canada, as leading economies in North America, have witnessed a surge in the construction of hyper-scale data centers, driven by the escalating demand for cloud-based services and the proliferation of Internet of Things (IoT) technologies.

Transitioning to Europe, the region has exhibited robust growth in data center construction, propelled by the increasing adoption of digital transformation strategies across various industries. European countries, notably Germany, the United Kingdom, and France, are focusing on enhancing their digital infrastructure to support cloud computing, artificial intelligence, and machine learning applications. The European data center market is also influenced by stringent data protection regulations, which have led to a rise in local data storage solutions.

By Geography

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Explore Extensive Ongoing Coverage on Technology Research Reports Domain:

- Cable management systems market is anticipated to be USD 61.1 billion by 2033. It is estimated to record a steady CAGR of 9.7%.

- Digital Music Content Market is anticipated to be USD 54.5 billion by 2033. It is estimated to record a steady CAGR of 9.5%.

- E-Commerce Personalization Software Market is expected to garner a 24.8% CAGR and reach a size of USD 2,412 Million by 2033.

- Generative AI in Content Creation Market is anticipated to be USD 175.3 billion by 2033. It is estimated to record a steady CAGR of 31.2%

- Power Electronics Market will exceed USD 94.21 billion by 2032 with a projected compound annual growth rate (CAGR) of 8.3%.

- Air Charter Broker Market: Growing at a CAGR of 12.0%. Learn more about the key trends, driving and restraining factors of the market.

- User authentication solution market size is expected to grow from USD 14.7 bn in 2022 to USD 54.5 bn by 2032, at a CAGR of 14.4%.

- K-12 Education Technology Market is anticipated to be USD 8,759.5 Mn by 2032. It is estimated to record a steady CAGR of 21.3%

- Generative AI in Clinical Trials Market is expected to reach a substantial worth of around USD 1,122 Mn by 2032, significant CAGR of 23.8%.

- Podcasting Microphone Market growth fueled by podcast popularity, increased mobile device usage, Growing desire for premium audio quality.

- Supply Chain Digital Twin Market projected to be valued at USD 8.7 billion in 2033, growing at a CAGR of 12.0% during the forecast period.

- Remote Sensing Technology Market size is expected to be worth around USD 61.7 Billion by 2032, record a steady CAGR of 19.0%.

- Smart Card Market is anticipated to be USD 29.6 billion by 2033. It is estimated to record a steady CAGR of 5.9% in the forecast period.

- Assistive Technology Market is anticipated to be USD 36.6 bn by 2033. It is estimated to record a steady CAGR of 4.8% in forecast period.

- Supercapacitors Market is likely to jump from USD 5.0 Bn in 2024 to USD 21.7 Bn by 2033, expand at a rate of 17.7% CAGR.

About Us

Market.US (Powered by Prudour Pvt Ltd) specializes in in-depth market research and analysis and has been proving its mettle as a consulting and customized market research company, apart from being a much sought-after syndicated market research report-providing firm. Market.US provides customization to suit any specific or unique requirement and tailor-makes reports as per request. We go beyond boundaries to take analytics, analysis, study, and outlook to newer heights and broader horizons.

Follow Us On LinkedIn Facebook Twitter

Our Blog: