Dublin, Nov. 14, 2025 (GLOBE NEWSWIRE) -- The "India Immunoglobin Market Outlook 2025-2033" has been added to ResearchAndMarkets.com's offering.

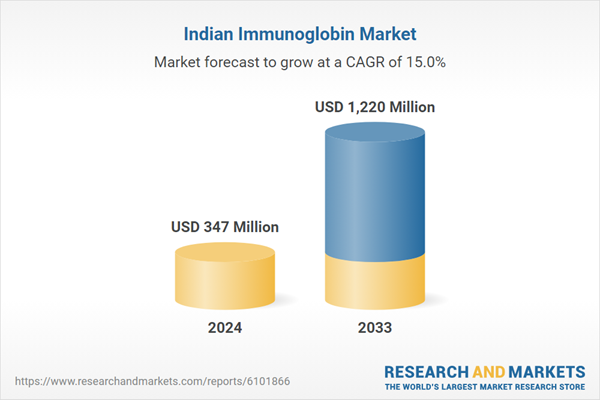

India's Immunoglobulin Market is expected to reach US$ 1.22 billion by 2033 from US$ 347 million in 2024, with a CAGR of 15% from 2025 to 2033. The rising prevalence of immunodeficiency disorders, plasma-derived therapies, government favors, growing health awareness, and rising domestic production are the main drivers of the immunoglobulin market in India. All these factors come together to increase demand and extend immunoglobulin therapy more widely across the country.

Growth Drivers for the India Immunoglobulin Market

Rising Prevalence of Immunodeficiency Disorders

One of the key drivers driving the growth of the Indian immunoglobulin market is the mounting cases of primary immunodeficiency diseases (PIDs). PIDs, a group of over 450 rare genetic conditions, weaken the immune system and expose individuals to increased susceptibility to infections, autoimmune disease, and cancer. In comparison to the worldwide incidence of 1 in 25,000 to 1 in 50,000 live births, India's estimated incidence of PIDs is 1 in 10,000 live births. Despite this higher prevalence, awareness and diagnosis remain poor, with as many as 70% of patients remaining undiagnosed, which increases morbidity and mortality rates. The sudden growth in unclassified cases highlights the need for awareness and early detection so critically. The demand for immunoglobulin therapy is driven by this growing patient base, which fuels market growth.

Advancements in Plasma-Derived Therapies

Plasma-derived treatments are a key driver of India's immunoglobulin market. The developments in plasma collection and processing technology have enhanced product quality and efficiency in production while reducing costs and making them more accessible. Immunoglobulin therapies are increasingly available due to these advances, along with increased domestic production and supportive government policies. This growth supports robust market growth and improved patient outcomes across the country by assisting in the alleviation of the increased demand generated by the increased incidence of autoimmune disorders and immunodeficiency in India.

Increasing Healthcare Awareness and Diagnosis Rates

India's immunoglobulin market is growing largely because there is increased healthcare awareness as well as improved diagnostic rates. As more individuals learn about autoimmune diseases and immunodeficiency disorders, increasingly more individuals are going to the doctor, thereby increasing the diagnoses. Immunoglobulin therapy is capable of being administered immediately due to this surge in early detection, which significantly improves patient outcomes. Adding to market demand even further is that advances in diagnostic technology have enhanced the accuracy and speed of detecting diseases treatable with immunoglobulins. More proactive approaches to health care and treatment access have been promoted by government schemes and medical campaigns, which have been essential to educate the public and medical professionals. Therefore, all these factors function jointly to facilitate the robust growth of the immunoglobulin market in India.

Challenges in the India Immunoglobulin Market

High Cost of Immunoglobulin Therapies

One major obstacle to the expansion of the immunoglobulin industry in India is the high expense of immunoglobulin treatments. These treatments produce pricey goods by requiring strict quality control and intricate manufacturing procedures. The high cost restricts accessibility and affordability for a large number of patients, particularly those from low-income and rural backgrounds. Furthermore, the reliance on imported plasma-derived goods drives up costs even more because of supply chain costs and import charges. This financial obstacle frequently results in incomplete or postponed therapy, which affects patient outcomes. Enhancing accessibility and propelling market expansion in India requires lowering therapeutic costs through better domestic production and encouraging government initiatives.

Regulatory and Quality Control Issues

Issues with quality control and regulations pose serious obstacles to the immunoglobulin business in India. Immunoglobulin products must adhere to strict regulatory criteria in order to be safe and effective, yet negotiating these convoluted clearance procedures can raise prices and delay market introduction. Furthermore, the diversity of plasma sources and production techniques makes it difficult to maintain uniform quality standards throughout manufacturing locations. Poor quality control can result in safety issues that undermine patient confidence and restrict market expansion. To overcome these obstacles and promote the sustainable growth of the Indian market, it is imperative to strengthen regulatory frameworks, improve inspection capacities, and encourage adherence to international quality standards.

Key Attributes

| Report Attribute | Details |

| No. of Pages | 200 |

| Forecast Period | 2024-2033 |

| Estimated Market Value (USD) in 2024 | $347 Million |

| Forecasted Market Value (USD) by 2033 | $1.22 Billion |

| Compound Annual Growth Rate | 15% |

| Regions Covered | India |

Key Topics Covered

1. Introduction

2. Research & Methodology

3. Executive Summary

4. Market Dynamics

4.1 Growth Drivers

4.2 Challenges

5. India Immunoglobulin Market

5.1 Historical Market Trends

5.2 Market Forecast

6. Market Share

6.1 By Product Type

6.2 By Mode of Delivery

6.3 By Application

6.4 By Region

7. Product Type

7.1 IgG

7.2 IgA

7.3 IgM

7.4 IgE

7.5 IgD

8. India Immunoglobulin Manufacturing Capacity

8.1 Biological E Limited

8.2 Intas Pharmaceuticals

8.3 Kedrion Biopharma

8.4 Bharat Serums and Vaccines

8.5 Reliance Life Sciences

9. Companies Investment Plans for Immunoglobulin Manufacturing in India

9.1 Plasma Collection Infrastructure/ Centres

9.2 Capital Requirements

10. Government Frameworks for Immunoglobulin Companies

10.1 Regulatory Framework

10.2 Pricing Control

11. Pricing Trends for IVIG Injections

11.1 Plasma Collection

11.2 Extraction and Purification

11.3 Formulation

11.4 Filling and Packaging

11.5 Regulations and Quality Control

12. Manufacturing Process for IVIG Injections

13. End-Users (Patient Numbers) of IVIG in India

13.1 Primary Immunodeficiency Diseases

13.2 Neurological Disorders

13.3 Hematological Disorders

13.4 Transplant Medicine

13.5 Autoimmune Diseases

14. Mode of Delivery

14.1 Intravenous Mode of Delivery

14.1.1 Historical Market Trends

14.1.2 Market Forecast

14.2 Subcutaneous Mode of Delivery

14.2.1 Historical Market Trends

14.2.2 Market Forecast

15. Application

15.1 Immunodeficiency Diseases

15.2 CIDP

15.3 Hypogammaglobulinemia

15.4 Congenital AIDS

15.5 Chronic Lymphocytic Leukemia

15.6 Myasthenia Gravis

15.7 Multifocal Motor Neuropathy

15.8 ITP

15.9 Kawasaki Disease

15.10 Others

16. Region

16.1 East

16.2 West

16.3 North

16.4 South

17. Porter's Five Analysis

17.1 Bargaining Power of Buyers

17.2 Bargaining Power of Suppliers

17.3 Degree of Rivalry

17.4 Threat of New Entrants

17.5 Threat of Substitutes

18. SWOT Analysis

18.1 Strength

18.2 Weakness

18.3 Opportunity

18.4 Threat

19. Company Analysis

19.1 Baxter international Inc.

19.2 Grifols SA

19.3 Bayer Healthcare

19.4 Takeda Pharmaceutical Company Limited

19.5 PlasmaGen BioSciences Pvt. Ltd.

19.6 Reliance Life Sciences

19.7 Biocon Limited

19.8 Virchow Biotech

19.9 Bharat Serums and Vaccines

19.10 Biological E Limited

19.11 Intas Pharmaceuticals

19.12 Kedrion Biopharma

For more information about this report visit https://www.researchandmarkets.com/r/860l9q

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world's leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Attachment