Dublin, Jan. 05, 2026 (GLOBE NEWSWIRE) -- The "Spinal Cord Stimulation Devices Global Market Report by Product, Application, End User, Countries and Company Analysis, 2025-2033" has been added to ResearchAndMarkets.com's offering.

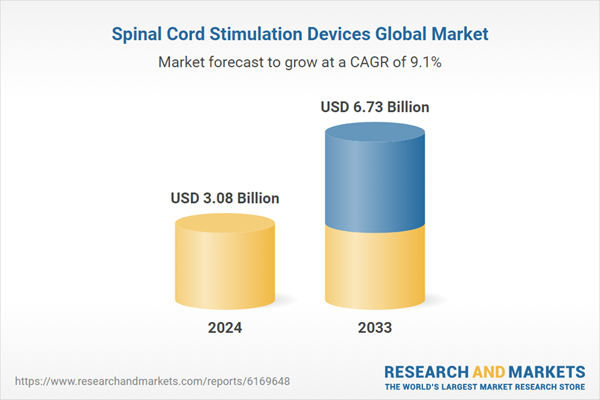

The Spinal Cord Stimulation Devices Market is expected to reach US$ 6.73 billion by 2033 from US$ 3.08 billion in 2024, with a CAGR of 9.07% from 2025 to 2033. The market for spinal cord stimulation devices is being pushed by factors such as an aging population, a rise in chronic pain cases, a growing preference for minimally invasive treatments, technological improvements, and greater awareness of neurostimulation therapies as pain management alternatives to opioids.

Key Factors Driving Spinal Cord Stimulation Devices Market Growth

An Increase in the Prevalence of Chronic Pain Conditions

The market for spinal cord stimulation devices is mostly driven by the rise in chronic pain problems worldwide, including neuropathic pain, sciatica, and lower back pain. Millions of people experience pain that is unresponsive to traditional treatments, which prompts patients and doctors to look for long-term, non-pharmacological solutions. This tendency is further exacerbated by aging populations, sedentary lifestyles, and rising prevalence of degenerative diseases and spinal injuries. SCS devices block pain impulses before they reach the brain, providing tailored, minimally invasive relief. Spinal cord stimulators are becoming a more popular option for patients who have not responded to traditional pain management techniques as medical professionals move away from opioid-based treatments because of the potential for addiction.

Developments in Device Design Technology

Technology advancements in spinal cord stimulation are greatly accelerating market expansion. Features including high-frequency stimulation, closed-loop feedback systems, and longer battery life are now available in modern devices, which increase patient comfort and pain alleviation. Wireless control systems, MRI compatibility, and rechargeable implants have improved usability and safety. Furthermore, more accurate, real-time adjustments catered to the demands of each patient are made possible by smartphone integration and customizable stimulation regimens. These technical developments increase overall cost-effectiveness by lowering the need for device replacement operations while simultaneously improving treatment outcomes. Spinal cord stimulators are becoming more popular among doctors and patients as long as manufacturers keep spending money on research and development.

Increasing Preference for Non-Opioid and Minimally Invasive Treatments

Patients and doctors are increasingly using minimally invasive, drug-free alternatives for pain management as worries about opioid abuse and long-term negative effects grow. With a comparatively minimal surgical risk and long-lasting pain alleviation, spinal cord stimulation devices present a possible answer. Compared to more aggressive surgical treatments, the minimally invasive implantation approach has fewer problems and shorter recovery periods. Furthermore, insurers and healthcare systems are gradually realizing that SCS devices are more cost-effective in the long run than long-term pharmaceutical treatment. Worldwide, the use of spinal cord stimulators is increasing due to the trend toward safer, more sustainable pain treatments, especially when incorporated into all-encompassing pain management plans in public and private healthcare facilities.

Challenges in the Spinal Cord Stimulation Devices Market

Saturation Expensive and with Little Reimbursement Coverage

The high expense of operations and devices is one of the main obstacles facing the spinal cord stimulation sector. SCS systems can be costly, frequently costing tens of thousands of dollars, combined with surgical insertion and aftercare. Various patients in various areas, particularly in poor nations, are unable to obtain these medications due to uneven reimbursement systems and restricted insurance coverage. Patients may be deterred from seeking this treatment by certain insurers' stringent qualifying requirements or partial coverage, even in mature markets. Affordability and reimbursement reform are essential for increasing access and promoting long-term market growth since the high upfront cost and economic inequities prevent widespread adoption.

Risks of Surgery and Varying Patient Results

Infection, lead migration, nerve injury, and device malfunction are among the dangers associated with spinal cord stimulation, despite the fact that it is less invasive than other surgical procedures. Furthermore, not every patient receives sufficient or durable pain relief; some may need revision surgery or device removal. Physicians may be hesitant to offer SCS because of the heterogeneity in patient outcomes, which is frequently caused by variations in pain kinds, anatomy, or psychological variables. Although they are not always definitive, pre-implantation experiments aid in predicting efficacy. Unfavorable results may cause patients to become dissatisfied and lose faith in the technology. The wider acceptance and deployment of SCS devices in various healthcare settings is still hampered by these medical issues as well as post-operative problems.

Key Attributes

| Report Attribute | Details |

| No. of Pages | 200 |

| Forecast Period | 2024-2033 |

| Estimated Market Value (USD) in 2024 | $3.08 Billion |

| Forecasted Market Value (USD) by 2033 | $6.73 Billion |

| Compound Annual Growth Rate | 9% |

| Regions Covered | Global |

Key Topics Covered

1. Introduction

2. Research & Methodology

3. Executive Summary

4. Market Dynamics

4.1 Growth Drivers

4.2 Challenges

5. Spinal Cord Stimulation Devices Market

5.1 Historical Market Trends

5.2 Market Forecast

6. Market Share Analysis

6.1 By Product

6.2 By Application

6.3 By End User

6.4 By Countries

7. Products

7.1 Rechargeable

7.2 Non-Rechargeable

8. Applications

8.1 Failed Back Surgery Syndrome

8.2 Complex Regional Pain Syndrome

8.3 Arachnoiditis

8.4 Sciatica

8.5 Degenerative Disc Disease

8.6 Others

9. End Users

9.1 Hospitals

9.2 Ambulatory Surgical Centers

9.3 Others

10. Countries

10.1 North America

10.2 Europe

10.3 Asia Pacific

10.4 Latin America

10.5 Middle East & Africa

11. Value Chain Analysis

12. Porter's Five Forces Analysis

12.1 Bargaining Power of Buyers

12.2 Bargaining Power of Suppliers

12.3 Degree of Competition

12.4 Threat of New Entrants

12.5 Threat of Substitutes

13. SWOT Analysis

13.1 Strength

13.2 Weakness

13.3 Opportunity

13.4 Threats

14. Pricing Benchmark Analysis

15. Key Players Analysis

15.1 Abbott Laboratories

15.2 Medtronic plc

15.3 Boston Scientific Corp.

15.4 Nevro Corp.

15.5 Saluda Medical Pty. Ltd.

15.6 Beijing PINS Medical Co. Ltd.

15.7 Nalu Medical

15.8 Stimwave Technologies

15.9 Synapse Biomedical Inc.

15.10 Gimer Medical

For more information about this report visit https://www.researchandmarkets.com/r/b7nho8

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world's leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Attachment