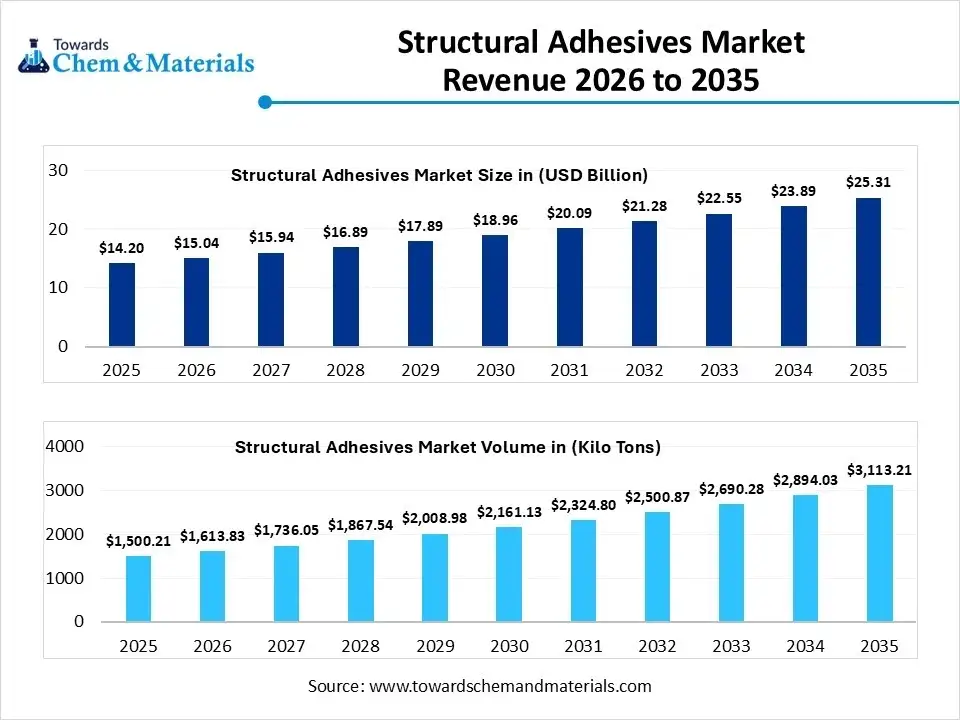

Ottawa, Feb. 25, 2026 (GLOBE NEWSWIRE) -- The global structural adhesives market size was estimated at USD 14.20 billion in 2025 and is expected to increase from USD 15.04 billion in 2026 to USD 25.31 billion by 2035, growing at a CAGR of 5.95% from 2026 to 2035. In terms of volume, the market is projected to grow from 1500.21 kilo tons in 2025 to 3113.21 kilo tons by 2035. growing at a CAGR of 7.57% from 2026 to 2035. Asia Pacific dominated the structural adhesives market with the largest volume share of 44% in 2025. The greater shift towards stronger bonding solutions in the major sectors, such as automotive, aerospace, and construction, is accelerating the industry growth in the current period.

The structural adhesives refer to the strong glues that are primarily used to join materials that carry heavy loads or stress. Moreover, the sectors such as the buildings and construction, automotive, and aerospace have seen a heavy demand for these structural adhesives. Also, the developers in this sector are using adhesives instead of metal joining methods nowadays.

Download a Sample Report Here@ https://www.towardschemandmaterials.com/download-sample/6184

Structural Adhesives Market Report Highlights

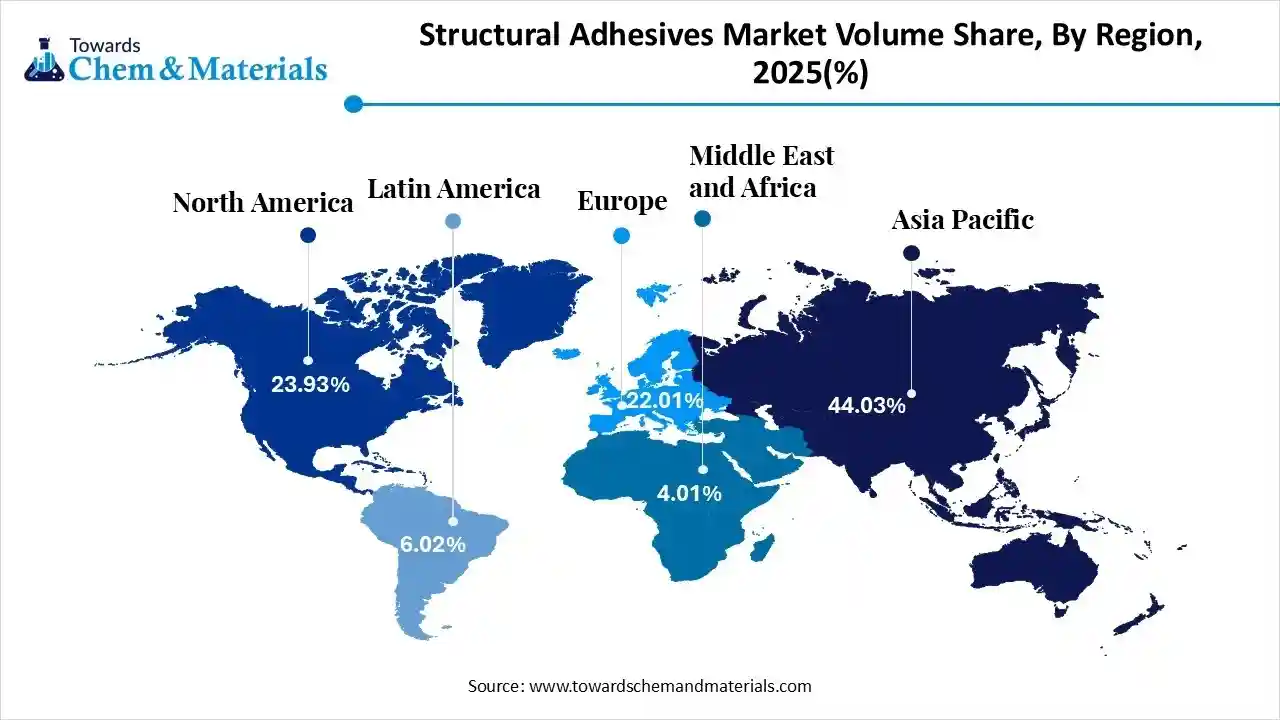

- The Asia Pacific dominated the structural adhesives market with the largest volume share of 44% in 2025.

- The structural adhesives market in North America is expected to grow at a substantial CAGR of 6.78% from 2026 to 2035.

- The Europe structural adhesives market segment accounted for the major volume share of 22.01% in 2025.

- By resin type, the epoxy segment dominated the market and accounted for the largest volume share of 42% in 2025.

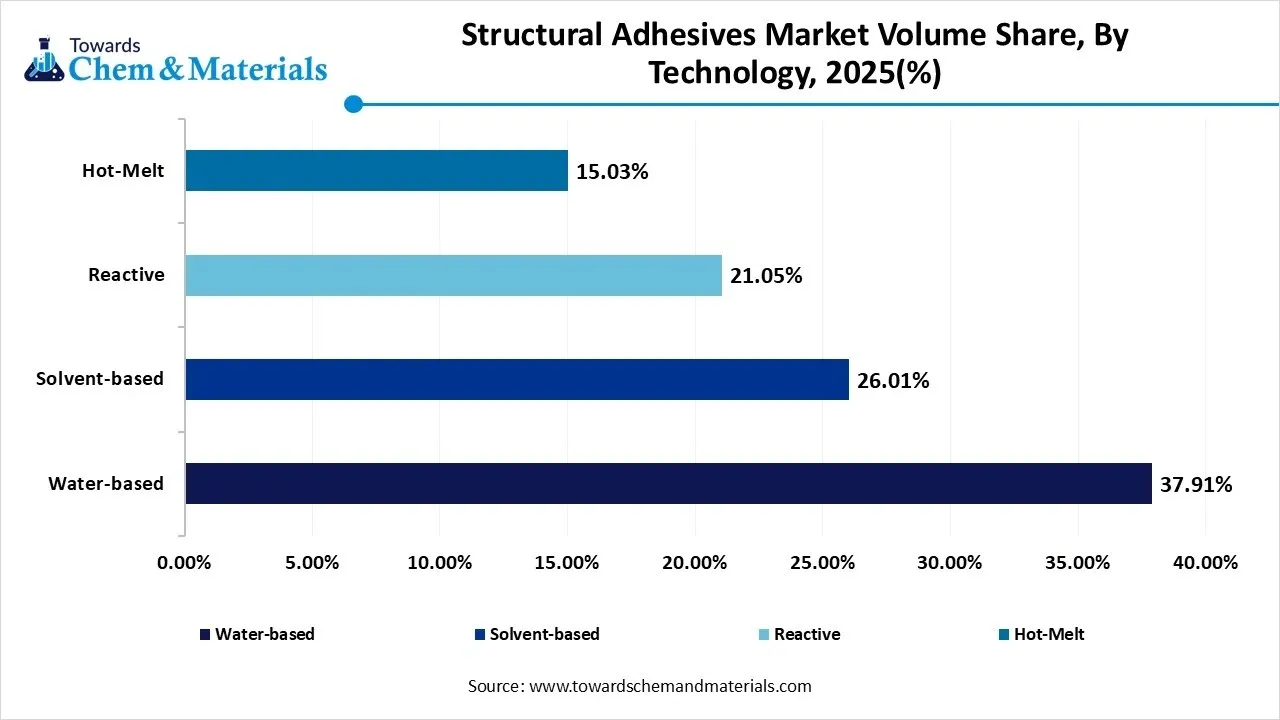

- By technology, the water-based segment led the market with the largest revenue volume share of 38% in 2025.

- By technology, the reactive segment is expected to grow at the fastest CAGR of 10.70% from 2026 to 2035 in terms of volume.

- By substrate type, the metals segment dominated the market and accounted for the largest volume share of 36% in 2025.

- By application, the automotive segment led the market with the largest revenue volume share of 32% in 2025.

Immediate Delivery Available | Buy This Premium Research Report (Global Deep Dive

USD 3200) @ https://www.towardschemandmaterials.com/checkout/6184

Structural Adhesives for Metal and Plastic Bonding

High-strength, lightweight structural adhesive metal bonding formulas make all the difference in applications where metal substrates and components must be assembled. Epoxy structural adhesives are very often used with applications where metal bonding is required, although anaerobic and acrylic adhesives may also be used. Improving process efficiency in both new and established designs remains a challenge for manufacturers, and Henkel’s range of structural adhesive metal bonding products promote efficiency and cost-savings without compromising on strength, impact resistance, or aesthetics.

Acrylic and polyurethane adhesives are also commonly used for plastic and multi-substrate bonding. This makes them particularly well-suited for a wide variety of different plastic substrate bonding where high-strength hold is required in addition to resistance from humidity and environmental factors.

Private Industry Investments for Structural Adhesives:

- Henkel’s Acquisition of Stahl: In February 2026, Henkel completed a major acquisition of Stahl for €2.1 billion to consolidate its leadership in high-performance surface and structural bonding.

- Arkema’s UV-Curing Expansion: In 2025, Arkema invested in specialized production lines for UV-curable structural adhesives designed to speed up assembly in the aerospace and marine sectors.

- Sika’s Southeast Asia Facility: In late 2025, Sika opened a new large-scale manufacturing plant in the region to supply structural bonding materials for burgeoning infrastructure and automotive projects.

- 3M’s EV Epoxy Development: In early 2026, 3M expanded its investment in thermal-management structural adhesives specifically designed to bond and protect electric vehicle battery components.

- Bostik’s Bio-Based Initiative: In February 2025, Bostik launched a joint venture focused on R&D for high-strength structural adhesives derived from renewable tropical biomass to reduce the industry's carbon footprint.

What are the Major Trends in the Structural Adhesives Market?

- Lightweight Products: The heavy usage of structural adhesives in lightweight products has strengthened the bottom line for the production firms in recent years. Also, it is being used to join plastic and composites.

- Shift Towards Factory Automation: The greater shift towards factory automation has resulted in high-yield outcomes for the industrial players. Moreover, the companies are shifting towards the robot installations to improve the work precision and waste reduction in recent years.

- Need for Stronger Bonds: The increasing need for stronger bonds is likely to increase return on investment for manufacturers in the coming years. Also, the industries are seen in using the advanced materials such as composites and carbon fiber, where structural adhesives are observed in providing better bonding qualities.

For more information, visit the Towards Chemical and Materials website or email the team at sales@towardschemandmaterials.com| +1 804 441 9344

Structural Adhesive Market Report Scope

| Report Attribute | Details |

| Market size value in 2026 | USD 15.04 Billion / 1,613.38 kilo tons |

| Revenue forecast in 2035 | USD 25.31 Billion / 3,113.21 kilo tons |

| Growth Rate | CAGR of 5.95% from 2026 to 2035 |

| Base year for estimation | 2025 |

| Historical data | 2018 - 2025 |

| Forecast period | 2026 - 2035 |

| Quantitative units | Volume in kilotons, revenue in USD million, CAGR from 2026 to 2035 |

| Report coverage | Revenue forecast, company ranking, competitive landscape, growth factors, trends |

| Segments covered | By Resin Type, By Technology, By Substrate Type, By Application, By Region |

| Regional scope | North America; Europe; Asia Pacific; Central & South America; Middle East & Africa |

| Country scope | U.S.; Canada; Mexico; Germany; U.K.; France; Italy; China; India; Japan; South Korea; Indonesia; Brazil; Argentina; Saudi Arabia; South Africa |

| Key companies profiled | Henkel AG & Co. KGaA; Dow; 3M; HB Fuller Company; Franklin International, Inc.; Avery Dennison Corporation; Ashland Global Specialty Chemicals Inc.; Lord Corporation; Arkema S.A.; Scott Bader Co. |

Immediate Delivery Available | Buy This Premium Research Report@ https://www.towardschemandmaterials.com/checkout/6184

Structural Adhesives Market Dynamics

Driver

Strong Bonds, Lighter Future Ahead

The need for strong and lightweight bonding solutions is actively driving the industry growth in the current period. As the industries want products that are durable but also lighter in weight. Structural adhesives help reduce the use of heavy fasteners like bolts and welding. This improves efficiency and reduces material cost. In the automotive and aerospace industries, fighter products save fuel and energy.

Restraint

Cost Barriers in Structural Bonding

The high cost of structural adhesives compared to traditional joining methods is expected to hamper the industry growth during the forecast period. Also, the small manufacturers may find it expensive to switch from welding or mechanical fastening. Also, proper surface preparation is needed for strong bonding, which increases time and cost. Some adhesives also need specific curing conditions, like heat or pressure.

Market Opportunity

What is the Most Significant Opportunity for the Structural Adhesives Industry?

The electric vehicles and renewable energy are anticipated to create significant opportunities in the coming years. Moreover, these industries need strong, lightweight, and durable materials. Structural adhesives help with battery assembly, solar panels, and wind turbines. They improve safety and performance. As clean energy projects grow, demand for these adhesives will increase. Another growing area is modular construction, where buildings are made in parts and assembled quickly.

Smart Adhesives Shaping Future Industries

The industry is shifting towards advanced and smart adhesive technologies. Also, the new structural adhesives cure faster and provide stronger bonding. Some adhesives can cure at room temperature, saving energy. Hybrid adhesives are also becoming popular because they combine flexibility and strength. Automation is improving application accuracy. Digital tools are being used to monitor bonding quality.

Structural Adhesives Market Segmentation Insights

Resin Type Insights

Why did the Epoxy Segment Dominate the Structural Adhesives Market?

The epoxy segment dominates the market, owing to they provide very strong bonding and durability. They can handle heavy loads, heat, and chemicals, making them ideal for construction, automotive, and aerospace. They also bond well with metals and composites. Epoxy adhesives last a long time, reducing maintenance costs.

The acrylic segment is experiencing the fastest growth in the market during the projected period, due to they offer fast curing and high flexibility. They bond quickly, which increases production speed in industries like automotive and electronics. They also work well on different materials without much surface preparation. The manufacturers prefer acrylic because it reduces manufacturing time, which directly increases profits.

Structural Adhesives Market Volume and Share, By Technology, 2025-2034

| By Technology | Market Volume Share (%), 2025 | Market Volume (Kilo Tons)2025 | Market Volume (Kilo Tons)2035 | CAGR(%) 2026-2035 | Market Volume Share (%), 2035 | |||

| Water-based | 37.91 | % | 568.73 | 1128.85 | 7.91 | % | 36.26 | % |

| Solvent-based | 26.01 | % | 390.20 | 878.24 | 9.43 | % | 28.21 | % |

| Reactive | 21.05 | % | 315.79 | 788.26 | 10.70 | % | 25.32 | % |

| Hot-Melt | 15.03 | % | 225.48 | 317.86 | 3.89 | % | 10.21 | % |

Technology Insights

How Did the Water-Based Segment Dominate the Structural Adhesives Market?

The water-based segment dominates the market because it is safe, eco-friendly, and low-cost. They release fewer harmful chemicals, making them suitable for indoor use and meeting environmental regulations. These adhesives are widely used in packaging, construction, and furniture. Also, companies prefer water-based adhesives because they reduce health risks for workers, which improves workplace safety.

The reactive segment is expected to grow fastest during the projected period, because they provide very strong and long-lasting bonds. They cure through chemical reactions, creating high-performance joints. These adhesives are used in demanding applications like aerospace, automotive, and wind energy. Also, the reactive adhesives enable lightweight design, replacing heavy mechanical fasteners. This is important for electric vehicles and renewable energy systems.

Substrate Type Insights

Which Substrate Type Segment Dominates the Structural Adhesives Market?

The metals segment dominates the market, owing to the fact that they are widely used in construction, automotive, and industrial equipment. Moreover, the structural adhesives bond metals strongly, reducing the need for welding and screws. This helps improve appearance and reduce weight. Metals require strong bonding solutions, which increases adhesive demand. Also, adhesives help prevent corrosion by creating a protective layer between metal surfaces.

The composites segment is experiencing the fastest growth in the market during the projected period, due to industries are moving toward lightweight and high-strength materials. These materials are widely used in electric vehicles, aircraft, and wind turbines. Adhesives are the best way to join composites because traditional methods can damage them. Also, the composites allow energy efficiency and fuel savings, which is a major global goal.

Application Insights

How Did the Automotive Segment Dominate the Structural Adhesives Market?

The automotive segment dominates due to vehicles' use of adhesives for body assembly, interiors, and safety components. Adhesives help reduce weight, improve strength, and enhance design flexibility. They also reduce noise and vibration. Also, the adhesives help manufacturers create sleek vehicle designs without visible joints, improving appearance. With millions of vehicles produced every year, demand is very high.

The wind energy segment is expected to grow fastest during the projected period, owing to increasing focus on renewable energy and sustainability. Structural adhesives are used to bond large wind turbine blades, which require high strength and durability. These adhesives can handle extreme weather conditions. Moreover, adhesives allow longer and lighter blades, which generate more energy. Governments are investing heavily in renewable energy projects, increasing demand.

Regional Insights

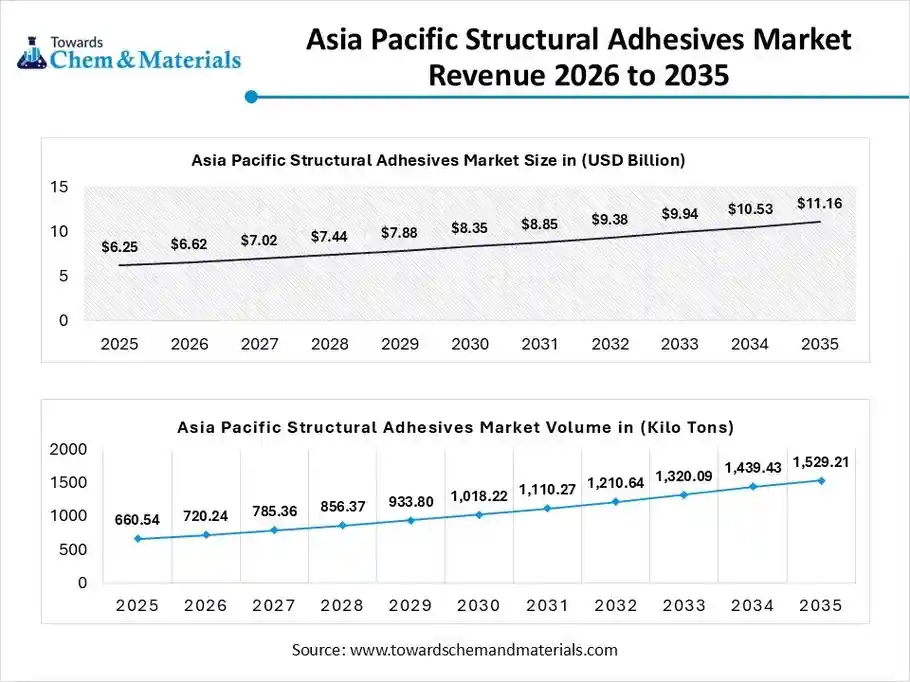

The Asia Pacific structural adhesives market size was valued at USD 6.25 billion in 2025 and is expected to be worth around USD 11.16 billion by 2035, at a CAGR of 5.97% during the forecast period. By volume, the market is projected to grow from 660.54 kilo tons in 2025 to 1,529.21 kilo tons in 2035. growing at a CAGR of 8.75% from 2026 to 2035.

How did Asia Pacific hold the Largest Share of the Structural Adhesives Market?

The Asia Pacific region is the leading region due to the fast construction, manufacturing, and industrial growth. Countries like China, India, and Japan produce huge volumes of cars, buildings, and electronics, all using structural adhesives. Labor costs are lower, so production is high. Governments are investing in infrastructure and smart cities, which increases demand.

China Structural Adhesives Market Trends

China’s market is experiencing steady growth, driven by rapid expansion in the automotive, construction, wind energy, and electronics sectors across China. Increasing adoption of lightweight materials in electric vehicles, supported by manufacturers such as BYD, is accelerating demand for high-performance bonding solutions that enhance durability and reduce weight.

Structural Adhesives Market Volume and Share, By Region, 2025-2035

| By Region | Market Volume Share (%), 2025 | Market Volume (Kilo Tons)2025 | Market Volume (Kilo Tons)2035 | CAGR(%) 2026-2035 | Market Volume Share (%), 2035 | |||

| North America | 23.93 | % | 359.00 | 647.86 | 6.78 | % | 20.81 | % |

| Europe | 22.01 | % | 330.20 | 626.38 | 7.37 | % | 20.12 | % |

| Asia Pacific | 44.03 | % | 660.54 | 1529.21 | 9.78 | % | 49.12 | % |

| South America | 6.02 | % | 90.31 | 182.12 | 8.11 | % | 5.85 | % |

| Middle East & Africa | 4.01 | % | 60.16 | 127.64 | 8.72 | % | 4.10 | % |

Why is the Structural Adhesives Industry Growing Rapidly in North America?

The North America region is the fastest-growing due to its focus on advanced technology and sustainability. The region demands high-performance adhesives for aerospace, automotive, and renewable energy industries. Strict environmental regulations push companies toward low-emission and strong adhesives. Moreover, the rise of automation and robotics has led to the use of adhesives replace mechanical joining for precision and speed in the region nowadays.

U.S. Structural Adhesives Market Trends

The U.S. market is experiencing steady growth, supported by rising demand across automotive, aerospace, construction, and industrial manufacturing sectors in the U.S. Increasing focus on lightweight vehicle production and electric mobility is driving greater adoption of high-performance bonding solutions that replace traditional mechanical fasteners.

Top Companies in the Structural Adhesives Market & Their Offerings

- H.B. Fuller Company: Supplies high-performance epoxies and MMAs for battery assembly and aerospace applications.

- Arkema S.A. (Bostik): Features the Bostik MMA range for high-strength bonding of metals and composites in demanding environments.

- DuPont de Nemours, Inc.: Focuses on BETAMATE™ and BETAFORCE™ brands to improve vehicle crash performance and safety.

- Huntsman Corporation: Provides the Araldite® line of epoxies and polyurethanes for aerospace and energy sector bonding.

- Illinois Tool Works Inc. (ITW): Markets Plexus® and Devcon® adhesives to simplify assembly in marine and transportation markets.

- Dow Inc.: Specializes in rapid-cure resins designed for lightweighting and composite bonding in mass production.

- Lord Corporation (Parker Hannifin): Offers structural acrylics that replace mechanical fasteners in industrial and sign assembly.

- Ashland Global Holdings Inc.: Produces Pliogrip® adhesives for bonding composite body panels in heavy-duty vehicles.

- Master Bond Inc.: Formulates custom epoxy systems engineered for extreme temperatures in electronics and medical devices.

- Permabond Engineering Adhesives: Supplies diverse acrylic and epoxy technologies for high-strength engineering and industrial bonding.

- Scott Bader Company Ltd.: Manufacturers Crestabond® primerless adhesives for the marine and wind energy industries.

- Hubei Huitian New Materials Co., Ltd.: Delivers a wide range of structural adhesives for the automotive and renewable energy sectors.

More Insights in Towards Chemical and Materials:

- Structural Steel Market Size to Reach USD 188.63 Billion by 2034

- Structural Adhesives Market Manufacturers & Suppliers Company Analysis 2026-2035

- Pressure Sensitive Adhesives Market Manufacturers & Suppliers Company Analysis 2026-2035

- Structural Adhesives Market Size to Surpass USD 25.31 Billion by 2035

- Industrial Adhesives Market Size | Companies Analysis 2026- 2035

- Europe Adhesives And Sealants Market Size | Companies Analysis 2026- 2035

- Europe Construction Adhesives and Sealants Market Size | Companies Analysis 2026- 2035

- Asia Pacific Adhesives and Sealants Market Size | Companies Analysis 2026- 2035

- North America Adhesives And Sealants Market Size | Companies Analysis 2026- 2035

- Aerospace Adhesives And Sealants Market Size | Companies Analysis 2026- 2035

- Bonding Adhesives Market Size | Companies Analysis 2025- 2035

- Tile Adhesives Market Size to Hit USD 7.61 Billion by 2034

- U.S. Adhesives and Sealants Market Size to Surge USD 17.08 Billion by 2034

- Polyester Hot Melt Adhesives (PHMAs) Market Size to Hit USD 1,491.92 Million by 2034

- Biobased Adhesives Market Size to Reach USD 14.66 Billion by 2034

- Adhesives Market Size to Hit USD 124.77 Billion by 2034

- Rubber-repair Adhesives Market Size to Reach USD 2.08 Bn by 2034

- Liquid Adhesives Market Size to Hit USD 70.52 Billion by 2035

- Plastic Adhesives Market Manufacturers & Suppliers Company Analysis 2026-2035

- Electronic Adhesives Market Size to Hit USD 15.29 Billion by 2035

- Floor Adhesives Market Size to Reach USD 17.1 billion by 2034

Structural Adhesives Market Top Key Companies:

- Henkel AG & Co. KGaA

- Dow

- 3M

- HB Fuller Company

- Franklin International, Inc.

- Avery Dennison Corporation

- Ashland Global Specialty Chemicals Inc.

- Lord Corporation

- Arkema S.A.

- Scott Bader Co.

Recent Development

- In January 2026, BioBond Adhesives, Inc., unveiled the latest production of adhesive, BioAdhere SUP250. This newly introduced adhesive is biobased and is specifically designed for the defence and mobility industry, as per the published report.

- In December 2025, Big Dog Adhesives introduced a reload adhesive system with reusable cartridges. This system replaces conventional single-use cartridges with a precision and reusable engineered housing compatible with pneumatic and standard manual dispensers.

Structural Adhesives Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2019 to 2035. For this study, Towards Chemical and Materials has segmented the global Powder Coatings Market

By Resin Type

- Epoxy

- Polyurethane (PU)

- Acrylic (including MMA)

- Cyanoacrylate

- Others (Silicone/Phenolic)

By Technology

- Water-based

- Solvent-based

- Reactive

- Hot Melt

By Substrate Type

- Metals

- Composites

- Plastics

- Wood & Others

By Application

- Automotive

- Building & Construction

- Aerospace

- Wind Energy

- Electrical & Electronics

- Marine & Others

By Regional

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Immediate Delivery Available | Buy This Premium Research Report@ https://www.towardschemandmaterials.com/checkout/6184

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Towards chem and Material | Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Automotive | | Nova One Advisor | Nutraceuticals Func Foods | Onco Quant | Sustainability Quant | Specialty Chemicals Analytics | TCM Blog

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Email: sales@towardschemandmaterials.com

Web: https://www.towardschemandmaterials.com/